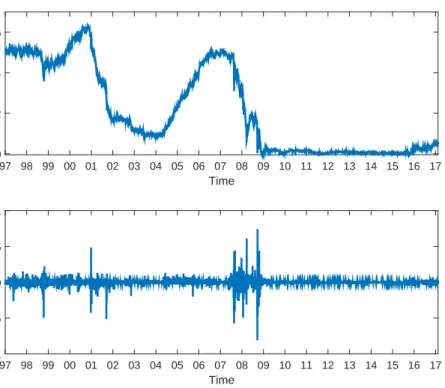

The risk-neutral stochastic volatility in interest rate models with jump–diffusion processes

Texto completo

Figure

Documento similar

word embeddings [32]. BERT-BASED MODELS TO CLASSIFY EEGS 458 To compare the results, we develop two experiments based 459 on BERT models with the same architecture. First, a model

Betas of the market premium factor, the market capitalization factor and the one-year momentum factor are statistically different from cero in the Fama French and Fama French

The EAT also outperforms another two emotion- adaptation approaches in a significant way: (1) the CMLLR- based approach where the speaker models are trained with the neutral

That the line profiles of neutral atoms and ions during the outburst phase are different, with the neutral atoms being more sensitive to the velocity variations in the accretion

We also assessed the role of CTCF as an insulator in several genomic contexts where binding sites for this factor are located between genes with divergent expression patterns,

The observed event yields in these regions are compared with the background expectation from standard model (SM) processes and the predicted contribu- tions from

Unlike these works, we employ factor models with principal components, which allows us not only to identify countries sharing common cycles (as is shown in de Lucas

Results from the SPR model that includes market participation as a tactical response (INCCP model) are compared with results from other two models: the first one is a certainty