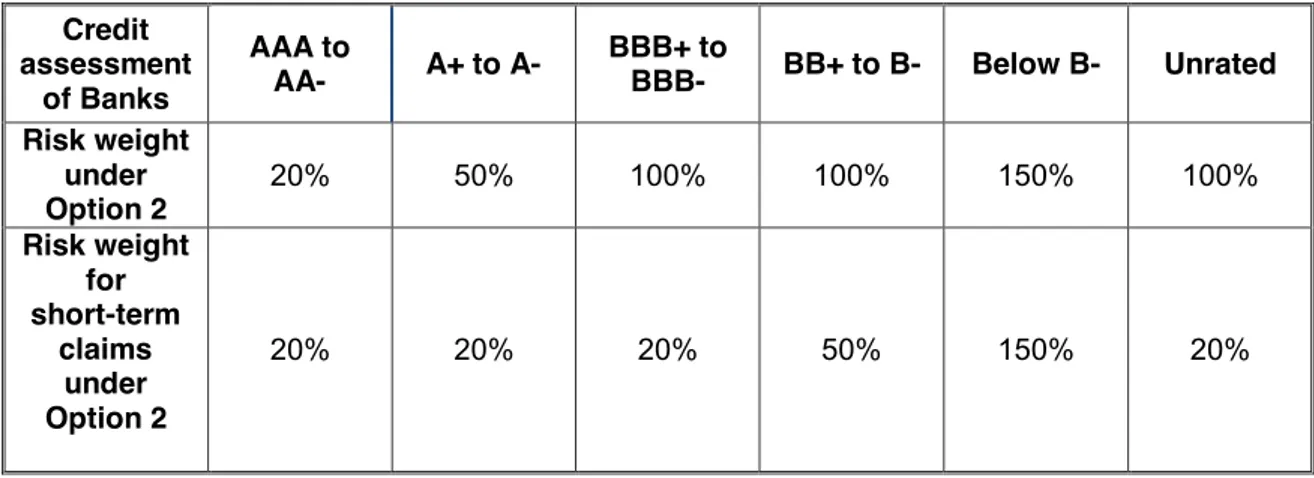

Credit risk on basel rules: Claims on corporates

Texto completo

Figure

Documento similar

We exploit the 2011 stress test supervised by the European Banking Authority (EBA) and the Spanish Central Credit Register to explore: 1) the occurrence and magnitude of these

“The impact of the 2007 liquidity shock on bank jumbo mortgage lending”, Journal of Money, Credit and Banking, 45(s1), pp. “Mortgage Securitization and Information Frictions

Finally, the paper uses an aggregate measure of uncertainty from the data submitted by forecasters that replied to two consecutive rounds and finds significant increases in

7 Weight assigned to best forecaster (cont.). e) Using density forecasts of unemployment one year ahead.. 8 Weighted averages of individual measures of uncertainty using the

Figure 7 shows how the VSTOXX declines abruptly in 2012, just after the start of the ECB’s Long-Term Refinancing Operations (LTROs). That was also the year when Mario

While larger firms are affected by the standard in the literature variables of bank credit growth and initial size, micro firms appear to be particularly vulnerable to

If the banks have proposed a net settlement system, the central bank in country i then updates its beliefs to that the risk of the foreign bank, <£,-, is uniformly

Jointly estimate this entry game with several outcome equations (fees/rates, credit limits) for bank accounts, credit cards and lines of credit. Use simulation methods to