The reasons behind the low level of financial development for Mexican households in Mexico are found in both the demand and supply of financial services. For other authors, financial inclusion is considered an ideal condition in which access to the various products offered by the financial system is universal (Roa, 2015), and not just the extended margin in the development of the financial sector. This later dimension is achieved when households' financial needs are covered without generating systemic risk in the financial industry (Roa, 2015).

Currently, Mexico is performing under the development of its financial system compared to other Latin American countries. In the case of demand drivers, culture and trust (or lack thereof) are considered two important elements for banks that limit financial inclusion (Beck and De la Torre, 2007; López-Rodríguez and Lima-Velázquez, 2015).

The experiment

This episode in the RCT shows that mistrust of banks is not only a cultural aspect, but is also based on banks' commercial practices. In terms of the RCT, it was decided that no separation of the two groups could be made because the individuals chose not to receive the bank accounts. Therefore, the results of the RCT can better be interpreted as the result of the training in entrepreneurial skills, financial literacy and the provision of the smartphone, as it was provided to all 180 households.

All families received smartphones and training on their use in the city of Tlaxcala, which had good access to a data signal. At the time of the experiment, antennas providing access to the wifi signal were being installed in all the capitals of the municipalities. While our families were used to using wifi signals from the moment RCT was installed in some of their communities, this solution did not work for all families as some communities do not have such antennas.

This last aspect also relates to competition in the telecommunications industry, which at the time of the RCT described in the paper saw very significant changes in behaviour, prices and services being offered in response to the changes produced by the 2014 telecommunications reform. .In terms of RCTs, this constraint is controlled for using fixed effects whenever possible. The experiment was designed to be representative of the state of Tlaxcala, following a strategy in which households were selected after a stratification of the state into 10 cells, which were obtained by dividing the municipalities of the state into two levels of poverty (high and low). , three levels of population (high, medium, low) and two levels of intensity of receiving remittances (high, low).

The size of the sample is obtained based on the distribution of a discrete random variable, which in this case was the proportion of households receiving remittances in the state of Tlaxcala, which according to ENIGH was around 6% during the 2000-2010 periods.

Implementation of the RCT 1 Empirical models

Data

In the case of account balances, treated households show an average balance of 111 pesos in 2011 (about 8 dollars) and an average balance of 309 pesos in 2014 (about 17 dollars). In the case of the school year of the head of the household, the table shows that the average household is more educated than the average head of the household from the treated households. It is shown that while the receipt of remittances is more common in the treated households, the difference with respect to the untreated households in this variable is not statistically significant.

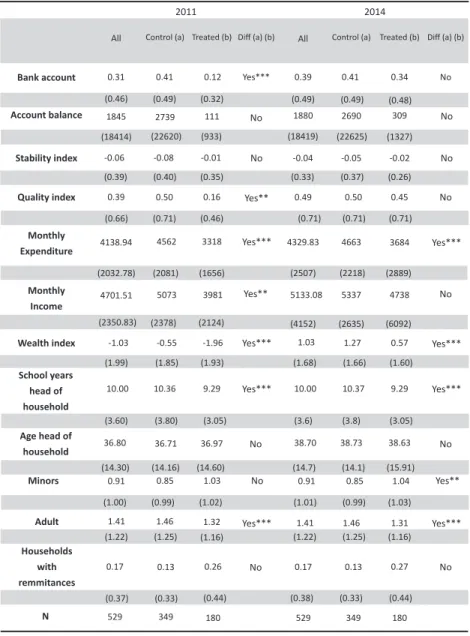

It is important to mention that the average receipt of remittances shown in the sample is 17%, which is above the average number of households receiving remittances in Tlaxcala. This was deliberately induced in the sample as the study represents households receiving remittances. In the case of the information at the municipality level, it is obtained from different sources: All information in the study will be presented in constant pesos by 2014.

The number of branches per ten thousand people within 2 kilometers of the municipality of Cabecera is 3.8 in the entire sample. The percentage of families living in municipalities with high acceptance of remittances is 13% in the entire sample, while 16% of families that participated in the KRT live in municipalities with high acceptance of remittances. 69% of the sample lives in municipalities with more than 30 thousand inhabitants, while 48% of the families that participated in the RCT live in similar municipalities.

The percentage of families living in municipalities with high poverty is 65% in the entire sample and there are no differences with treated families.

Results

- Financial Inclusion: Linear models

- Financial Inclusion: Non-Linear specifications

- Results for other household outcomes

- Robustness checks: the role of remittance reception

- Relation to literature

- Limitations of the study

The third column of Table 5 shows that the treatment reduced the stability index by 0.08 points, an effect that is significant at the 10% level. The fourth column of Table 5 shows that the treatment increased the quality index by .29 points and that the change is significant at the 1% level. One additional year of education of the head of the household increases the probability of having a bank account by 3.8%.

The above results imply that the effect found for the treatment is relatively large compared to the effect of other exogenous variables. One more year of education increases the account balance by 1% and this is statistically significant at the 10% level. These results also show that the treatment generates a relatively large effect on It is important to clarify that the weighted estimate for the account balance generated a non-significant effect, which is different from what is found with the linear model.

These results may indicate that the number of observations is insufficient to obtain an accurate estimate when it is. Consequently, we conclude that the evidence suggests no treatment effect on stability and quality indices. In the case of the probability of a bank account, the table shows that for households receiving remittances, the treatment is not statistically significant, while for households receiving remittances, the treatment increases the probability of owning a bank account by 10%.

This result is interesting and shows that treatment influences the composition of household expenditure. The RCT presented in this paper found positive effects on bank account ownership and account balances, as well as wealth and micro-enterprise activity. The different results are likely due to structural differences in the countries studied, which relate to differences in labor markets (i.e. the US labor market is more productive and therefore pays higher wages), as well as in financial market institutions (i.e. in the US competition and consumer protection promotes savings and consumer rights). The combination of these two structural differences probably leads to the fact that in Mexico, when a household generates savings, it immediately looks for investment opportunities that arise in the form of micro-enterprises or indicators related to housing construction.

Conclusions

In terms of policy recommendations, these two problems faced and resolved during the RCT reveal the need for major investments in infrastructure as well as changes needed in consumer protection regulation to achieve universal coverage of mobile and banking . services. The RCT also faced two very important structural reforms that changed incentives for all households, including the control group. The first one allowed the entry of more competitors in financial services and the second one lowered prices and increased services provided by telecommunications companies.

As for the RCT presented in this article, the panel data methodology allows for common changes occurring at the same time of treatment, whenever fixed effects were feasible. The results imply that costs of accessing financial services are important, as when those costs are reduced, bank accounts increase. However, the results also show that services provided by the financial sector do not fully meet the needs of the studied households, as account balances have grown less than proportionally to the increase in account holding, and there is evidence that households are adjusting the composition of their expenses that invests in micro-business and in real assets, rather than in savings or the use of bank credit.

The paper also presents evidence that the effects of processing have a negative association with receipt of remittances. Households receiving remittances have lower effects than those found among households not receiving remittances. This result is consistent with the idea that households receiving remittances are able to reduce credit constraints (Mackenzie and Rapoport, 2007) and consequently respond less to this type of intervention.

However, the study found that the main effect of the treatment on these types of households was a 12% increase in wealth, demonstrating that the TFE and TES help them change the composition of their spending, increasing their investment in real assets .

Comisión Nacional Bancaria y de Valores (CNBV, 2016), Disposiciones de Carácter General Aplicables a las Instituciones de Crédito (Circular Bancaria Uniforme). Recuperado de: http://www.cnbv.gob.mx/Prensa/Presentaciones%20Seminario%20Corresponsales/i.%20Circular%20Única%20de%20Bancos.pdf. Comisión Nacional Bancaria y de Valores (2010), Banca de Corresponsales: Una Oportunidad para Llevar Servicios Financieros a Todos.

Recuperado de: http://www.cnbv.gob.mx/Prensa/Presentaciones%20Seminario%20 Correspondsales/i.%20Folleto%20Corresponsales%20Bancarios.pdf Comisión Nacional Bancaria y de Valores (2011), Informe de Inclusión Financiera-. Comisión Nacional para la Protección y Defensa de los Usuarios de Se-pdf Financiero (CONDUSEF, 2015), Anuario 2014. 2014), “Migración, remesas e innovaciones financieras: un análisis comparativo entre el Estado de Tlaxcala y el resto del país”, en S. Las Nuevas Dimensiones del Desarrollo Regional en México en el Siglo XXI: Lecturas en Honor a los Dres. Tlaxcala: El Colegio de Tlaxcala, A.C. 2017), remesas, tecnología móvil y desarrollo sostenible.

Levine (2005), "Finance, Financial Sector Policies and Long-Term Growth", The World Bank Policy Research Working Paper 4469. Centro de Investigación y Educación Económicas (CIDE). 2004), "Financial Sector Policy and the Poor: Selected Findings and Issues", The World Bank Working Paper 43, Washington, D.C. Lima-Velazquez (2015), El efecto de la desconfianza en el uso de los servicios financieros formales en Yunez, A., Rivera, F., Chávez, M., Mora, J.

Rapoport (2007), “Network Effects and the Dynamics of Migration and Inequality: Theory and Evidence from Mexico”, Journal of Development Economics.