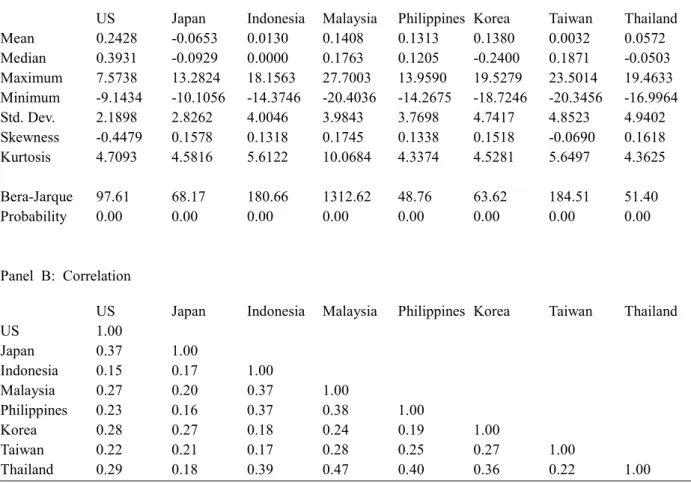

In contrast, however, there are several empirical studies showing that the financial markets of East Asian countries became increasingly integrated with those of developed countries in the 1980s (Glick and Hutchison, 1990, Cheng and Mak, 1992, Bekaert and Harvey, 1995 and Kuen and Song, 1996). Contrary to this result, the Japanese innovation plays little role in determining the East Asian market index returns. The last variable in the sequence is simultaneously correlated with the rest of the variables.

On average, the foreign influence contributes only 7.9 percent to the forecast error variance of East Asian market returns by the fourth week in the first period.

Financial Liberalization and Penetration of Foreign Financial Institutions of East Asian Financial Markets

In the Philippines, the share rose to 35.5 percent in 2001 after a sustained decline in the first half of the 1990s, and in Thailand there has been a gradual increase in the share of foreign banks. A large part of the increase in the market share of foreign banks in the Southeast Asian countries has come from the large increase in their lending in local currency as shown in Figure 4. Except for Malaysia, in all the East Asian countries, the absolute amounts are for international claims. of the foreign banks has fallen, which has raised the ratio between local currency and international receivables. In the early 1990s, the six East Asian countries secured more than 70 percent of their total international financing from financial institutions.

However, it is American and European institutions that dominate in the roles of brokers and dealers of derivative transactions.

Causes of Foreign Dominance in Capital Market Services in East Asia

The nature of shareholder population in East Asian countries has also contributed to underdevelopment of the financial services industry. That is, East Asian savers and investors were brokered by Western financial institutions at New York and London markets. In investing their surpluses, East Asian countries sought the services of Western financial institutions.

There is no doubt that the share of Western financial institutions in East Asia has increased since the early 1990s.

Prospects for Regional Financial Integration in East Asia

There are plenty of emerging market funds operating out of New York to invest in East Asian securities. As a result, borrowers and lenders from East Asia will have more incentives to move to the New York and London markets than before, accelerating the integration of East Asian financial markets into global financial centers. Trade liberalization has unleashed market forces that have drawn East Asian economies to regional integration; financial liberalization to global financial integration.

While the East Asian countries have not been able to coordinate their institutional reforms at the regional level, they have been pressured to adopt codes and standards for. In terms of finance, most of the East Asian countries can benefit more from joining the US. Thus, when deciding whether to join a CCA, East Asian countries may need to carefully examine whether monetary integration will help develop efficient regional financial markets that can survive competition with other global financial markets .

This cost consideration has led to the proposals to establish an East Asian Regional Stock Exchange and an East Asian Regional Bond Market. While these markets may enable some East Asian countries to borrow in their own currencies, there is no guarantee that a regional bond market in East Asia will be large and efficient enough to survive competition with global bond markets. Bond issues in the proposed East Asian market would be denominated in key regional currencies.

There is also the question of whether the East Asian bond market may be more efficient at diversifying corporate funding sources and opening up new investment opportunities than global bond markets. Finally, efficiency considerations may ultimately require the integration of the East Asian regional bond market with global bond markets.

Concluding Remarks

There is also no reason to believe that the East Asian bond market will be better positioned to protect countries in the region from a repeat of the financial crisis in the future, unless it can be shown that this market will not be less susceptible to speculation. cattle and other market failures as much as international financial markets have been. One concern is that financial liberalization may not necessarily help improve the efficiency and competitiveness of the financial services industry in East Asia through the process of learning and acquiring new and more sophisticated financial technologies, certainly not in the foreseeable future. Because the gap in financial technology and expertise between East Asian emerging market economies and advanced developed countries is so large and building legal, regulatory and other financial infrastructures is so costly and time-consuming that Asian countries Easterners may never be able to catch it. with their Western competitors, and may in fact fall into the trap of low-tech banking, while the provision of other more sophisticated financial services is dominated by foreign financial institutions.

This specialization will not cause serious problems for East Asian countries if the efficiency and stability of the global financial system can be improved to reduce the incidence of financial crises and help emerging market economies to better withstand both internal and external shocks through an effective system of liquidity provision and prudential regulation of financial institutions and markets at the global level. Despite the long and protracted debate over the reform of the international financial system, in the eyes of many East Asian policymakers not much has been achieved to represent the interests of emerging market economies.13 There is no reliable global or regional lender of last resort , which could provide liquidity support to emerging market economies in the event that they experience short-term balance of payments problems. From the perspective of East Asian emerging market economies, developed countries with developed financial markets have not made much effort to expand and strengthen cross-border financial supervision and cross-border financial regulation.

The lack of effective cross-border prudential supervision of foreign financial institutions operating out of East Asian financial markets has caused a number of problems. Most important of all, it is difficult for East Asian policymakers to predict how branches or subsidiaries of foreign financial institutions and their parent institutions would behave in times of financial distress and crises in emerging market economies. Most East Asian countries have been unable to borrow in their own currencies on international capital markets, although they have lifted many restrictions on capital movements, and that is not likely in the short term.

Montiel (2001), “Post-crisis Exchange Rate Policy in Five Asian Countries: Filling in the “Hollow Middle”?, een paper opgesteld voor een seminar over Exchange Rate Regimes: Hard Peg on Free Floating”, het IMF Institute, maart, 2001. McKinnon, Ronald (2002), "The East Asian Exchange Rate Dilemma and the World Dollar Standard", Asian Development Bank, februari.

Before the 1997 Crisis

1 Korea

A central point of the reform was the adoption of a negative list system in regulating capital flows. 1999, p.73), “in Indonesia, the capital account had been liberalized well before the crisis and the free currency system had been a pillar of economic policy for the past 30 years.”. Most restrictions on the inflow of foreign direct investment into import substitution industries had been lifted by the 1970s.

This included simplifying the investment process and raising the limit on the percentage of ownership of joint ventures that non-residents can own. During the early 1990s most of the remaining restrictions on foreign ownership were removed so that by 1994 100 percent ownership was possible in most industries. Before the crisis, Malaysia took a major liberalization of the capital account on two occasions in 1986-87 and 1994-96.

Foreign investors were allowed to acquire up to 49 percent ownership of publicly traded shares. According to Table 2, net capital inflows in Indonesia and Thailand average 4.1% and 9.1% of GNP in the period 1992-1996, while the corresponding figures are 1.9% and 7.2% in Korea and Malaysia. In the first half of the 1990s, the three countries recognized the need to slow down and in some cases reverse capital account liberalization.

The first round of the liberalization process in May 1990 focused on the deregulation of current account transactions. The second (April 1991) and third (February 1994) rounds saw most controls on capital outflows removed.

Capital Account Liberalization : After the 1997 Crisis

These include a prohibition on the sale of short-term money market instruments to non-residents, and a prohibition on commercial bank swaps and outright bidding-side forward transactions with foreign customers, unless trade-related. Some of the deregulation measures include:. i) Removal of all formal and informal barriers to FDI in palm oil plantations; ii) Removal of restrictions on FDI in retail and wholesale; And. iii) Reducing the number of activities closed to foreign investors until July 1998. Due to the expectation of a depreciation of the currency, interest rates in the offshore ringgit market increased relative to domestic interest rates.

Capital controls were aimed at eliminating the offshore ringgit market and limiting the supply of ringgit to speculators, and some of the specific measures introduced on 1 September 1998 included:. The disruption of capital inflows combined with rapid growth brought in a large amount of foreign capital that exceeded the absorptive capacity of the Thai economy. Then, growing concerns about the rapid deterioration of the current account, an overvalued exchange rate, and the insolvency of the financial system led to a sharp reversal of capital inflows and eventually touched off a major crisis.

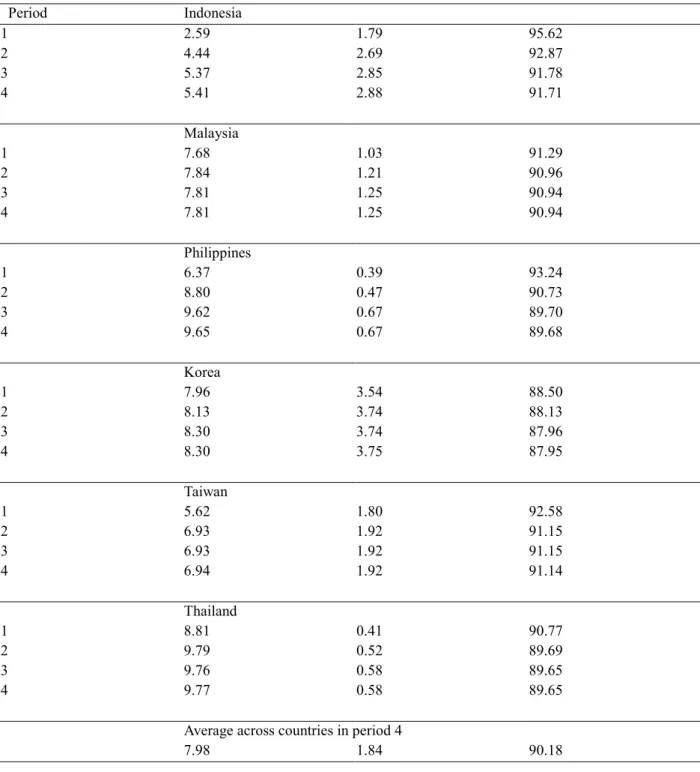

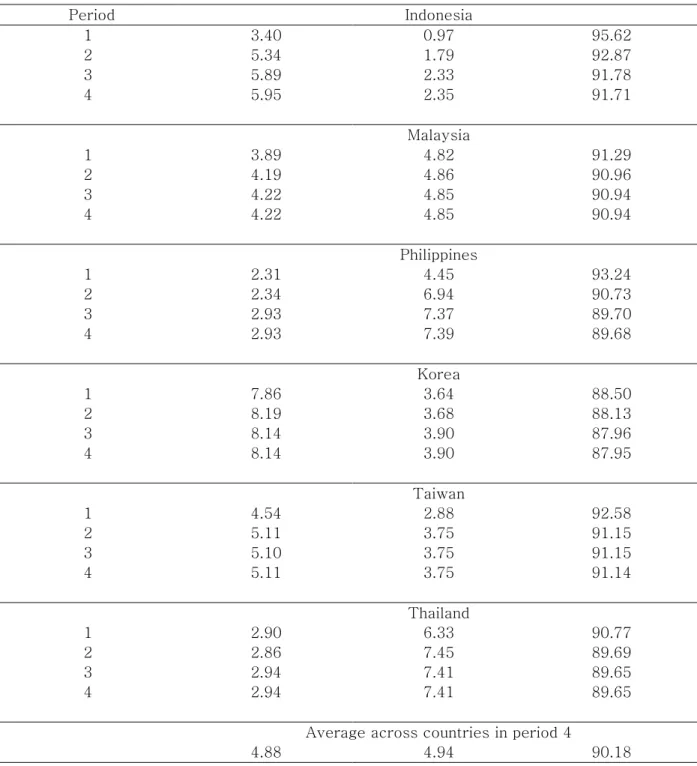

In recent periods, there are indications that the Thai authorities have intervened in the foreign exchange market to limit the short-term volatility of the nominal exchange rate. For this intervention goal, they have tightened foreign exchange reporting requirements, raising concerns that the tightening is a prelude to the reintroduction of some of the capital controls they previously abolished. The table shows the results of variance decomposition of Asian market returns using the estimates of trivariate VAR for the US, Japan and each of the six Asian markets.

The table shows the results of variance decomposition of Asian market returns using trivariate VAR estimates for Japan, the US and each of the six Asian markets. The table presents the results of variance decomposition using the estimates of the trivariate VAR for the US, Japan, and each of the six Asian markets estimated for each of the two sub-periods (before the Asian currency period and after the Asian currency crisis period, respectively. In the equation of motion for the conditional variances, ι is a 3-vector of ones, α, β are 3-vectors of parameters (where ∗ is the Hadamard matrix product, element by element), and H0 is an unobserved initial covariance matrix that we set equal to the sample covariance matrix of the returns.

The table lists the top 20 managers before and after the Asian currency crisis.