Red-letter improvements to inland waterway and road transport networks appeared in the last decades of the 18th century. Per capita growth rates rose from something close to zero in the first half of the 18th century to no more than 2-3% per year in the mid-1800s. There seems little doubt that de-industrialization in the South was the result of a massive influx of European manufactured imports.

Of course, the basic equality of per capita levels combined with Europe's small population meant that Third World 'industry' dominated world production in the 18th century (Bairoch 1982 Table 10). The lack of data makes it more difficult to document changes in global income distribution during the first wave of globalization. Due to the high transport costs, the industry is also somewhat spread out in the north and in the south.

Higher incomes lead to a larger local market in the North and this in turn attracts relatively more investment to the North. That is, northern industry and innovators benefit proportionally more than the south from increased industrialization in the north.

Capital and Financial Market Integration

Correlation of Investment and Savings

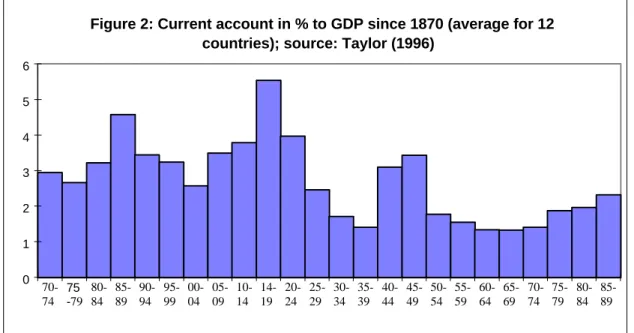

Before World War I, the average size of capital flows was quite high for certain countries, especially during the decades around 1880. Depression. In fact, they suggest that the current international financial system still has some way to go before reaching the levels of capital mobility achieved during the first wave of globalization.

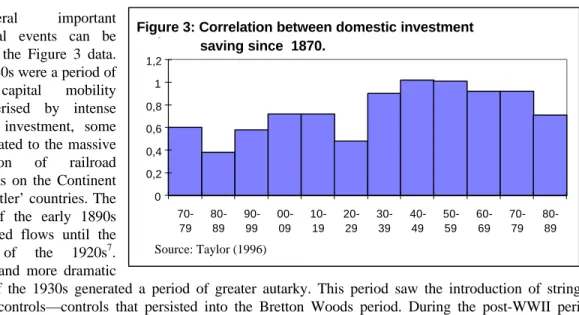

The 1880s was a period of high capital mobility marked by intense foreign investment, some of it related to the massive expansion of railway networks in the continent and 'settler countries'. In the post-World War II period, these controls were gradually relaxed and eliminated in many nations. The fall in the investment savings correlation in the 1980s is significant, but on that background capital mobility is still lower than during the previous booms in the 1880s and 1920s.

Interest rates and Financial Market Integration

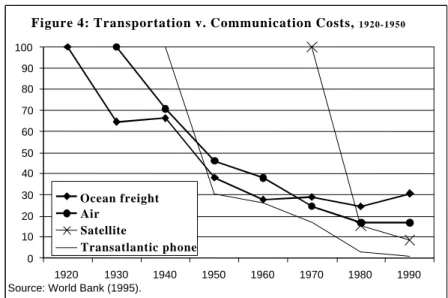

The telecommunications revolution of the late 20th century favored the rapid, almost frenetic movement of highly liquid assets.

Financial Crises

4 Trade, Investment, Migration and Factor Prices

- Trade

- Trade Barriers

- Trade Flows

- Trade with Emerging Economies

- Multinationals and Foreign Direct Investment

- Migration

- Factor Prices and Globalisation

- Factor Prices and Post-WWII Globalisation

- Factor Prices in the First Globalisation Wave

This, in turn, promoted the mass migration of people and capital in the late 19th century (more on this below). The last column of the table also contains figures on the exponential growth of the most recent form of communication, the Internet. Since the signing of the GATT in the late 1940s, all developed countries have gradually liberalized tariffs and other border measures on industrial goods.

However, as Lindbeck (1973) noted, the denominators in the 19th century consisted primarily of private economic activity. During the second phase, however, trade liberalization and rapid industrialization changed the nature of Third World participation in the world trading system. In fact, FDI was in many ways more important in the first wave than in the second.

Globalization has caused falling real wages in the US and high unemployment in Europe according to populists such as Buchanan (1998) and Goldsmith (1994) as well as some scholars such as Leamer and Wood (1994). In sharp contrast, the past two decades have been nothing short of a disaster for unskilled workers in the world's rich nations. As Krugman (1997) says, rising wage inequality in the US is the flip side of Europe's rising unemployment.

In the United States, migration accounts for another 30–40% of the decline in the lowest-skilled American workers (Borjas, Freeman, and Katz 1997). In turn-of-the-century Europe, land was scarce and labor was plentiful; in the new world, land was plentiful and labor was scarce. Not surprisingly, labor (and capital) flowed from the Old World to the so-called settler economies of the New World.

This was particularly evident in the most open economies such as the United Kingdom and the Nordic countries. These changes resulted in about a 40% drop in the ratio in the New World and about a 50% increase in the ratio in the Old World. It also fueled anti-trade sentiment in Europe in the form of the continent's retreat from liberalism after the 1880s.

5 Economic Beliefs, Institutions and the Policymaking Environment

Macroeconomics and Finance

- Why the Adjustable Peg Died

- The Gold Standard’s Success

In short, the increased sanctity of the monetary holy trinity and self-fulfilling attacks are increasingly forcing nations to choose between managed floats and membership in a grand monetary union. The gold standard was an adjustable-pin regime that worked well despite a high degree of capital mobility. The gold standard worked because governments solved the tri-lemma; they were satisfied with only two elements of the holy trinity – fixed exchange rates and perfect capital mobility.

Eichengreen (1996) argues that the gold standard was “a socially constructed institution whose viability depended on the context in which it operated”. Specifically, a critical element was the protection that governments and central banks had against political pressure—especially pressures to sacrifice exchange rate stability for domestic economic stabilization. In short, the central bankers of the 19th century did not face the dilemma between internal and external balance. In particular, the impact of monetary policy on employment, output and prices has not been fully captured (see Box 1).

Ignorance of the actual effects of monetary policy therefore certainly had a positive effect on the credibility of the system. After observing the impact of gold finds on output and the inflationary consequences of debasing a currency, central bankers and economists had a clear idea of the connections between the money supply, prices, unemployment and aggregate output. Before the First World War, macroeconomics was not a distinct field and much of the debate focused on seemingly tangential issues such as whether bank credit in forms other than notes could affect prices.

15 Traces of Eichengreen's point can also be found in Triffin's statement that: "The most important development of the [post World War I] period was the growing importance of domestic factors as the main determinant of monetary policy." Flandreau et al (1998) attribute this point to Polanyi (1944). 16 See Flandreau, Le Cacheux and Zumer (1998) for a critique of this view and a detailed study of central bank independence during the gold standard. In addition to the political isolation surrounding central bankers, the UK's dominance of the international trade and financial system was a critical factor underpinning the gold standard's success.

World War I, the rise of democracy, the end of Pax Britannica, and Keynesianism all served to destroy the social and intellectual context that supported the gold standard.

Trade Policy

- Evolution of the Intellectual Climate

- Evolution of the Policymaking Climate

However, the supremacy of the free trade doctrine among leading economists did not hinder the development of modern protectionism, especially the baby industry argument. Alexander Hamilton was one of the earliest and most influential proponents of this doctrine. The writings of John Stuart Mill and Robert Torrens (who developed something akin to the optimal tariff argument) deflowered the purity of the free trade doctrine.

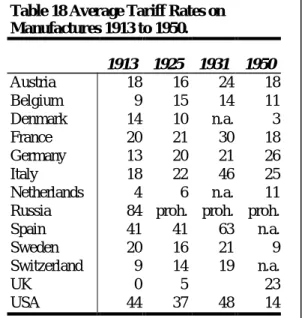

The first sustained drive against free trade began in Britain just after the end of the Napoleonic Wars in 1815. It also signaled the end of the Pax Britannica and Britain's hegemonic support for the international trading system. The last straw that finally broke the back of the world trade system was the US tariff increase in 1930.

By the end of the decade, the world had broken into different world trading systems, according to Kindleberger (1989). Japan created its own trading system in the form of the Greater East Asia Co-Prosperity Sphere. It encouraged the acceptance of the autarkic commercial philosophies of the fascists in Germany, Italy and Japan.

By the late 1930s, the US and Great Britain had learned their lessons and were trying to liberalize trade even as World War II broke out. The war interrupted these efforts, but the restoration of the world trade system emerged as one of the main objectives of the Bretton Woods institutions. That is, the world trade order is seen as a central pillar of American prosperity, so that its protection constitutes a central element of the US's self-defined national interests.

At the end of the first wave of globalization, the world trade system had almost no institutional support and was not really a system in the formal sense of the word.

6 Summary and the Lessons of History

At the same time, WTO/GATT membership grew from 19 countries in the late 1940s to more than 120 countries today, GATT coverage was expanded to include agriculture, services and clothing. Importantly, the expansion of global trade and investment after World War II created a powerful pro-trade lobby in every advanced industrialized country, namely exporters and multinationals. Specifically, because of today's highly balanced pattern of trade (most trade consists of two-way trade in goods between rich countries), powerful export lobbies in Europe, Japan, and the United States have a strong interest in preserving and promoting free trade between countries. three blocks.

This political power therefore acts as a very important barrier to another defense escalation on the scale of the 1930s among the advanced industrial nations. Such agreements help stabilize the system, even as the US slowly relinquishes the mantle of economic leadership. Unfortunately, these 19th century beliefs are still alive in some nations – in particular China and Russia.

So it would appear that a key challenge in global governance is to draw these nations tightly into the global system of trade and investment.

7 References

An Intellectual History of Free Trade. 1997), “On the Evolution of the Global Income Distribution,” Journal of Economic Perspectives, 11, 3, p. Do They Matter and What Are We Doing About Them?”, in R. Whalley The Emerging Global Trade Agenda: High Stakes for Developing Countries, Overseas Development Council, Washington D.C. Has globalization gone too far?