By the end of the last century, the most widespread view was that financial development had a significant positive impact. Although this literature has generally been interested in the broad question of the impact of financial development on growth, there are also studies such as Edison et al. 2002) explicitly analyzed the links between international financial integration and economic growth,1 and concluded that it was not possible to reject the null hypothesis that international financial integration did not accelerate growth.

Other benefits of international financial and banking integra-

Other benefits of international financial and banking integration: indirect channels. especially in the case of international economic integration, the ultimate reason explaining its importance was the implications for growth. For example, one of the claimed benefits of the integration of global financial markets is its supposed positive effect on financial stability, as risks would be spread around the world.

The dangers of international financial and banking integration

Some of the most critical views have even considered it a stylized fact that there is actually no correlation between long-term economic growth and financial globalization (Rodrik and Subramanian 2009). Referring to Lane's article on Financial Globalization and Crisis (2012), Dani Rodrik argued that some of the original arguments for financial globalization were to equalize the marginal returns to capital around the world, to transfer savings from rich to poor countries. , which contributes to increasing growth and convergence.

International financial integration and the crisis

However, even before the onset of the international financial crisis of 2007-2008, some voices pointed to the limited benefits of deeper financial integration for growth. Other gentle views on financial globalization, despite the crisis, are offered by Kose et al.

Measuring international financial and banking integration

The paper cited above by Edison et al. 2002) actually addresses the question of how different measures of financial inclusion can affect growth. In contrast, other measures of financial integration are actually more specific, focusing on particular types of integration, such as banking globalization.

The book’s plan

But in the case of the degree of banking, the effect is the opposite. Nevertheless, the effect in the case of the degree of bank affiliation (Figure 3.7) is the opposite.

How did Financial Integration Impact on the Activity, Pro-

Issuances are classified into two groups: debt issuance and regulatory capital issuance, based on the criteria of whether the corresponding instrument can absorb losses without endangering the bank's viability. The part analyzing the evolution of the asset side of banks is based on aggregated data of assets and credit balance by category, published in the Statistical Bulletin of the Bank of Spain during the period 1998 to 2011.

Financial integration and business model of banks

- domestic and foreign wholesale funding on banks’ balance

- The use of the financial resources on the asset side

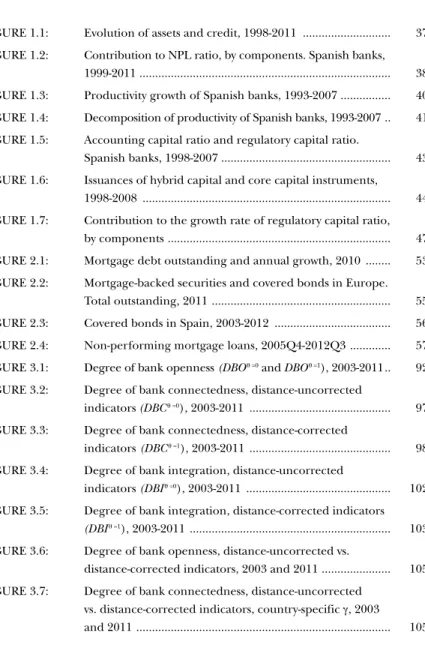

The eruption of the crisis has led to liquidity problems for Spanish banks due to difficulties in refinancing previous debt issuances. The strong increase in assets can largely be explained by the evolution of credit activity.

Productivity growth and performance measures

Martín Oliver, Ruano and Salas (2013) regress the estimates of banks' productivity against a list of potential determinants, and they conclude that a large part of the productivity growth during the euro period can be explained by the change in the way the Spanish banks operated. business model. When all the determinants of productivity differences are taken into account, we see that the technical progress (growth of the time trend) of the banking industry is increasing.

Financial integration and solvency of banks

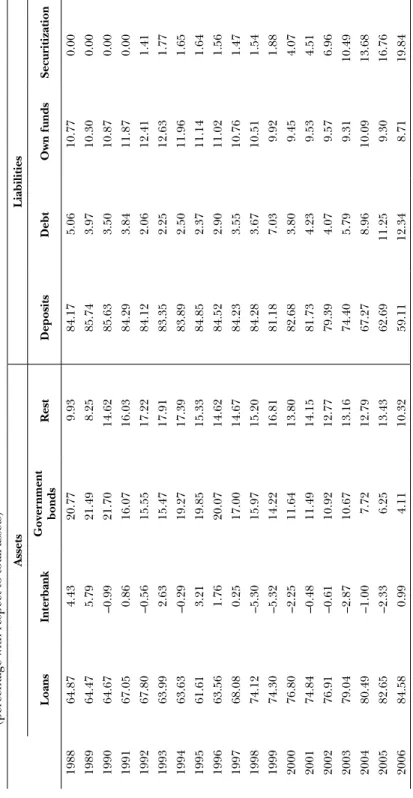

The first ratio, Regulatory Capital/Core Capital, is the inverse of the core capital weight within the statutory capital. This means that the statutory capital quality to absorb losses deteriorates at the same time as the banks' assets become riskier.

Conclusion

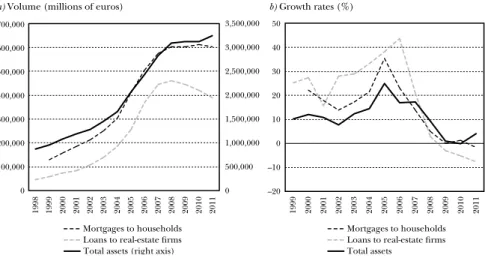

The end of the story about the banking crisis in Spain has not yet been written. Securitization represents one of the main forms of financial activity across the borders of the various EU financial systems.

The mortgage market in Spain

The entity then issues securities representing claims on principal and interest payments made by borrowers on group loans. Importantly, the issuer has an ongoing obligation to maintain sufficient assets in the cover pool to satisfy the claims of covered bondholders at all times.

How are mortgage quality and securitization related?

Indeed, a widely held view prior to the recent global credit crisis emphasized the positive effect of securitization in diversifying credit risk across the financial system, strengthening its overall resilience (Greenspan 2005). At the same time, there were gradually more skeptical attitudes towards the impact of securitization on the stability of the financial system.

Given the problems that arose with CBs, are CBs an alternative

In the aftermath, alternatives to securitization have been sought (see the report of the Banking Supervision Committee [ECB 2011]). While banks with high loan-to-value ratios are more likely to issue MBS, the issuance of MBS does not predict lower loan-to-value ratios in the future.

What about the real effects? did securitization have a say in

As evidence of this, we find that a bank is more likely to issue CB when it has a relatively low return and a high loan-to-deposit ratio. Interestingly, CdR finds that a greater securitization intensity of a firm's lead bank reduces credit constraints to a greater extent.

Conclusions

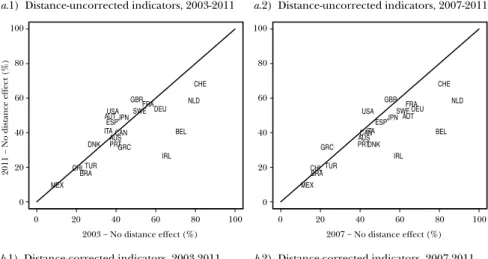

We also observe notable inconsistencies in the evolution of the degree of bank openness across countries. The upper panel represents the evolution of the mean, both unweighted (solid lines) and weighted (dashed lines). 3 The derivation of the following equations, well known in the literature (see, for example, Caldarelli 2007), is also reported in the Appendix.

Beyond the Law of One Price: International Banking

- Controlling for distance

- definitions

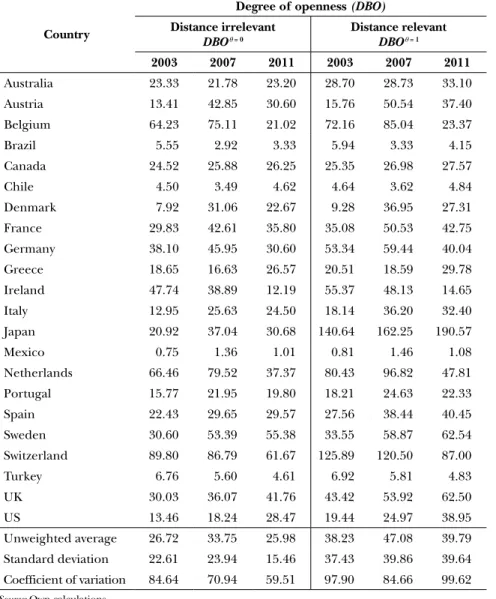

We then define the relative flow (cross-border bank assets or liabilities) or degree of banking openness between countries i and j as DBOijθ = Xij Xˆiθ. The measure of total banking connectedness assesses the importance of both direct and indirect relationships that countries establish with each other. Therefore, for the banking markets in country i ∈ N, we define the degree of banking integration as, .

The last one is verified because DGBI is a weighted average of the countries' degree of banking integration, where the weight of each country directly depends on its size. As of 2011, the share of the US banking system was quite small (13.97%), especially considering the size of the US economy. As also indicated in table 3.1, the total assets of the US banking system in terms of GDP are considerably lower than those of most countries in the sample.

Results

- degree of bank openness

- degree of bank connectedness

- degree of bank integration

- How distance and the crisis affect bank integration

Specifically, in the case of the euro area countries, the degree of openness has decreased markedly since the crisis began. The violins reveal some patterns that hide the evolution of the average degree of banking connectedness. Considering the degree of banking openness (DBO) and the degree of banking connectedness (DBC) together, we construct the indicator of banking integration (DBI).

Conclusions

Note: Number of defaults as a function of the net value percentage g, for probability function (5.7). The figure shows the total number of defaults after the shock propagation ends (for better visibility, we do not report the standard deviations in this graph). In this section we analyze the behavior of the networks when changing the size of the largest bank in the system.

Systemic Risk, Contagion, and Financial Networks

Connectivity, coordination and network formation

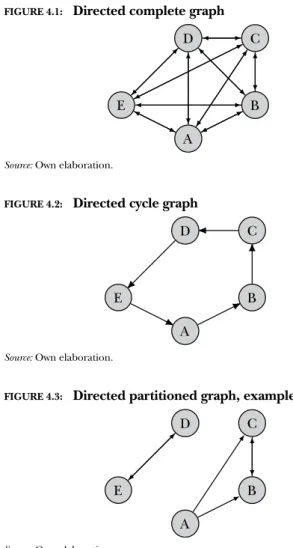

Finally, in the case of the partitioned graph structure, only two of the four regions are affected by the infection. Another interesting extension of Allen and Gale's (2000) basic framework is explored in Babus (2007). To simplify the model, the author also assumes that the network formation game is played only between banks of the same type.

Connectivity and phase transitions

To address this point, Acemoglu, Ozdaglar and Tahbaz-Salehi (2013) use a model where the size of the shock is related to the total excess liquidity in the system. A convex combination of the two becomes less stable and less elastic as g increases (the higher g, the closer to the graph the cycle network configuration). Therefore, regardless of the network structure of the financial system, there will be no default.

Homogeneity versus heterogeneity

The main result is that the most heterogeneity is introduced, the least network resilience. The ratio between the total amount of interbank assets and the total interbank liabilities is kept constant across nodes. When the average connectivity is low, the probability of spillover due to failure of the most connected bank is higher than the probability of failure of the largest node.

Imperfect information, moral hazard and bank runs

In other words: the structure of the network and the degree of diversification do not matter. As mentioned, the returns on investments here, unlike in Brusco and Castiglionesi (2007), depend on the network structure of the interbank market. However, when the chance of success of the gambling tool is high enough, the decentralized solutions are applied. are very close to the solutions of the social planner.

With this choice of parameters, we get tail indices in the degree distribution, which are equal or With this choice of parameters, we get tail indices in the degree distribution, which are equal or Note: The number of defaults as a function of the upper bound of the bank size interval used in the Monte Carlo simulations.

Hubs and Resilience: Towards More Realistic Models of the

Generating mechanism for a scale-free banking system

Since loops are not allowed in our model (they would mean that bank i and j are both borrower and lender of each other), we have to use a criterion to eliminate one of the edges. For a fixed sequence of the sizes {Ai}, several different realizations of the network are thus possible. A possible choice is to randomly eliminate one of the two terms i → j or j → i; however, there are also other options if the purpose is to enforce the disassortative behavior of the networks (see section 5.3).

Topological properties and the probability function

4 In order to strengthen the disassortative behavior, one can use a criterion for eliminating the loops other than the one described in footnote 2. 4 In order to strengthen the disassortative behavior, one can use a criterion for the elimination of the loops other than the one described in footnote 2. 5 To strengthen the disassortative behavior, one can use a criterion for eliminating the loops other than the one described in footnote 2.

Simulation results

- Transmission of shock

- Bank capitalization

- Interbank exposure

- Results with other network generators

- The size of the hubs

The figure shows the total number of defaults (thick black line) along with the standard deviation of the mean (thin vertical lines) and the number of defaults that occur in the first four stages of shock propagation. In the following, we will compare the number of defaults in sizeless, random, and maximum entropy networks for different system capitalization. As the upper limit of b increases further, networks will become very sparse and the number of defaults will decrease due to lower overall system connectivity.

Conclusion

A network analysis of the Italian money market.” Journal of Economics Dynamics and Control 32, no. Systemic Risk: The Dynamics of Model Banking Systems.” Journal of the Royal Society Interface 7, no. Contagion in the interbank market and its determinants.” Series 2: Discussion on Banking and Financial Studies Paper No.

Computation of the degree distribution via the

Estimating financial contagion in the interbank market: Maximum entropy versus observed interbank lending patterns." Temi di discussion (Economic working papers), Working Paper no. Estimating bilateral exposures in the German interbank market: Is there a risk of contagion? European Economic Review 48, no. The Transformation of the parameter in the size distributionρ(Ai), from Aito kin/out, brings us to: A.5.4) The transformation of the parameter in the size distribution.