These cover the outlook for the macroeconomic environment, with a gradual recovery of EU economic growth and a strengthening of the US dollar in the medium term. Second-generation biofuel processing technologies will become economically viable by the end of the design period and will begin to contribute on an industrial scale to biofuel production in the EU. The EU would also increasingly benefit from a growing world demand and relatively high world price levels, supported by the assumed strengthening of the USD in the medium term.

Beef production is expected to decline over the medium term to below the level of 7.6 million t in 2014 in line with the structural reduction of the dairy herd and the impact of decoupling. EU-27 milk production is expected to expand at a modest pace over the short term in line with the increase in production quotas granted to eleven member states of the EU-15. Bulgaria and Romania will grow stronger than the rest of the EU in the medium term at levels above 6 %.

Cereals

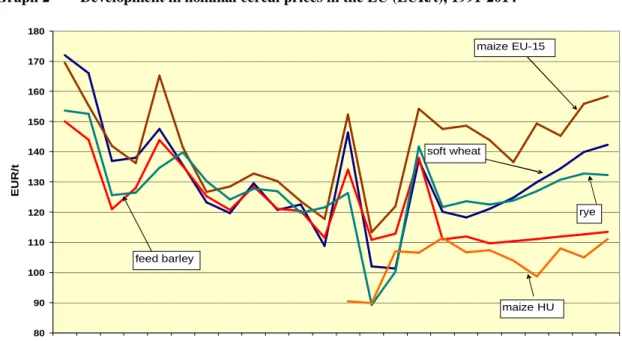

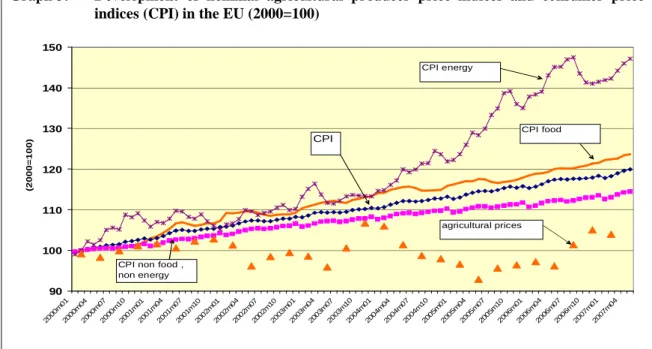

Favorable conditions on the world markets and growing domestic demand should support nominally higher grain prices than in the last decade. Finally, the impact of higher meat prices again has little impact on overall consumer prices due to the low weight of meat in the CPI (at 3.6. The relatively stable cereal area and low yield growth should be important factors contributing to a relatively balanced market situation cereals in the forecast period for most regions in the EU.

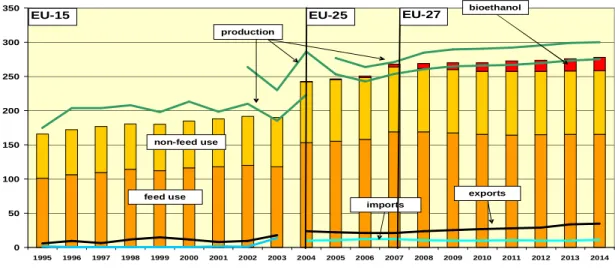

Domestic consumption of cereals would increase by 10 million tonnes over the projection period from 268 million tonnes to 278 million tonnes in 2014 due to the growth of the emerging bioethanol and biomass industries. By the end of the projection period, second-generation biofuel technologies are likely to become commercially viable and lead to a slowdown in demand for cereals and sugar beets for bioethanol production. Second, the overall increase in the production of white meat and eggs in the EU is expected to be significantly lower than in the last decade.

In the medium term, changing price conditions will also result in a significant change in the composition of grain feed use. Barley will maintain regional competitiveness in feed production in the early part of the projection period in the western part of the EU. In particular, the registered maize import of 4 to 5 million t in the last two years should fall again due to the increasing availability of.

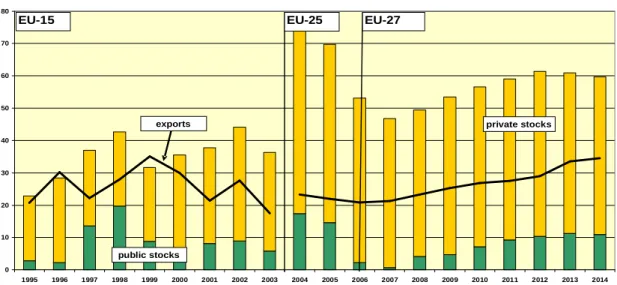

However, the displacement of barley and common wheat in feed use by maize could lead to increasing stocks in the western parts of the EU (barley) and in the landlocked EU-12 Member States (common wheat). The regional distribution of public stocks would be more evenly distributed between in the different parts of the EU due to the phasing out due to the phasing out of the maize intervention.

The EU oilseed markets

Due to the expected low harvest in 2007 and the phasing out of maize intervention, stocks will only gradually grow to 11 million tonnes in 2014. However, the risk of increasing stocks for barley in Germany remains in case of higher than expected harvests if as well as for wheat in the EU-12 due to infrastructure problems and the associated high transport costs. In summary, the medium-term outlook for EU-27 cereal markets should remain moderately positive for most regions in the EU due to the impact of the CAP reform, the phasing out of maize intervention, the subdued outlook for growth of the yield, the emerging bioethanol market and the expected gradual integration of Bulgaria, Hungary, Slovakia and Romania into the internal market together with more favorable world market conditions are expected to balance grain markets worldwide until 2014.

The expected continued trend in the allocation of crushing and biodiesel production capacities in the EU should lead to an increase in oilseed imports. The total area of colapa, sunflower and soybean oilseeds bottomed out in 2002 at 6.6 million ha before increasing to 7.0 million ha in 2004 (of which 0.8 million ha as non-food oilseeds on land set aside). Very favorable medium-term prospects for oilseed markets should lead to a steady increase in harvested area to 10.3 million ha by 2014.

Due to the limits imposed by the Blair House agreement (with a maximum of 1 million t of soybean meal equivalent), the non-food oilseed area is expected to remain stable at 0.8 million ha in 2014. It is estimated that that production will increase to 34.6 million t, supported by the expansion of oil fields and strong growth of the rapeseed crop (1.8% per year). Most of the growth would come from rapeseed production, as sunflower and soybean production should remain relatively stable.

Any further increase in non-food oilseed production on set-aside land remains limited by the Blair House agreement, which effectively limits the total EU oilseed production potential. Domestic demand is projected to expand by another 18 million t between 2007 and 2014 to reach 66.6 million t (mainly for canola, followed by soybeans).

The sugar market

However, beet production costs are only one factor in supply chain competitiveness and can be offset by economies of scale in the sugar processing industry, which in the case of southern regions of the UK versus many in the medium term, the prospects will be defined by the pace of restructuring in the short term because it determines who who will bear the costs of the adaptation and how much structural burdens will be brought forward, i.e. within the transition period until 2009, when the restructuring funds would mitigate the change or after the transition period, when the costs would have to be borne by the industry and beet growers themselves. Nevertheless, in the short to medium term, sugar beet production can be expected to decline in the least competitive regions of the EU.

Beet growers in the most competitive regions of the EU, especially France, Belgium and Germany, would benefit from this trend and find additional markets. The pace of restructuring of the EU sugar sector would determine how much and when it will benefit from these positive medium-term factors. The regional distribution of the reduction takes positive account of those regions that have already used the restructuring fund.

The emerging biofuel production will contribute to stabilize sugar beet production despite the significant price pressure for the beet sugar market due to the slow restructuring and the accumulated high levels of stocks until the end of the transition period in 2009. The high level of stocks that will remain until 2009 be reduced over time and fall to 2.9 million tonnes at the end of the projection period. The high domestic availability of sugar will lead to pressure on market prices for sugar from 2010, taking into account the assumed slow pace of restructuring until 2009.

The limited absorption of restructuring funds carries a large downside risk factor, despite the temporary withdrawal of quotas in 2007. The first major risk is due to the potential amount of imports within the EBA initiative and the consequent costs of adjustment rates for the sector post-2009.3 The second major downside risk factor is the high level of total stocks in the markets, which would weigh heavily on the medium-term outlook post-2009 with the reported projected restructuring burden leading to low prices in 2010 and 2011.

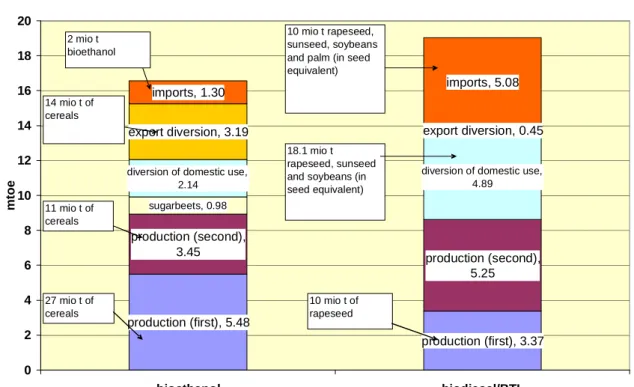

Assuming this development of demand for biofuels in the EU-27, the main factors determining the impact on agricultural markets are: The analysis assumes that biodiesel production will remain in the EU taking into account the current international competition. Bioenergy production represents one of the main major opportunities for agriculture in the medium and long term in the EU.

5 The market prices of beef in the EU-10 member states increased sharply after enlargement, with increases varying between 10 and 30. In the medium term, per capita consumption of pork in the EU-27 is expected to increase from 41.9 kg in 2006 to 43, 2 kg by 2006. 2014, with a marked increase in the EU-12 (supported by sustained economic growth and purchasing power). Due to lower domestic demand and partial EU bans on imports from third countries (introduced as measures to protect against avian influenza), EU-25 poultry meat imports fell to 578 000 t in 2006 (-4%).

With the decline in exports outside the EU, the EU-27 is projected to become a net importer of poultry meat by the end of the projection period. The graph below shows the evolution of meat consumption per capita in the EU during the period 1991-2014. EU-27 milk production is projected to expand at a modest pace in the short term in line with the increase in production quotas granted to the eleven EU-15 member states, but in the medium term, milk production will gradually decline to level of 148.2 million t in 2014, driven by a continued decline in subsistence production in the EU-12.

7 Although compensation through direct payments has mitigated the impact of declining milk prices in the EU-15. Cheese production in the EU-27 is expected to increase further in the medium term between 2006 and 2014 by a total of 10%, mainly due to continued strong increases in the EU-12. After a short-term parity in 2007, the EU price is expected to increase faster than the world market price and to be about 8% higher in the medium term.

Agricultural labor input in the EU-10 countries is assumed to decrease by 3.5% on average annually during the forecast period, in line with the restructuring of the agricultural sector. Agricultural income in EU-2 is expected to show a positive trend, rising steadily to show an increase of 71.8% in 2014. 15 The growth rate in this baseline assumes a stable macroeconomic environment in EU-10 throughout the baseline period.