Alternatively, performance differences between LPs may be due in part to differences in the objectives LPs have when investing in private equity (and not necessarily their ability). To test this hypothesis, we examine investments in young private equity groups (founded after 1990) across all classes of LPs. This article is also related to the literature on setting up private equity funds.

However, the drivers and consequences of individual limited partners' decisions to invest in private equity have so far been unexplored, largely because the data have been unavailable until very recently. Efforts to invest in private companies with private equity groups have often encountered agency problems. Institutional investors are known to vary widely in their sophisticated approach to private equity investing.

The Data

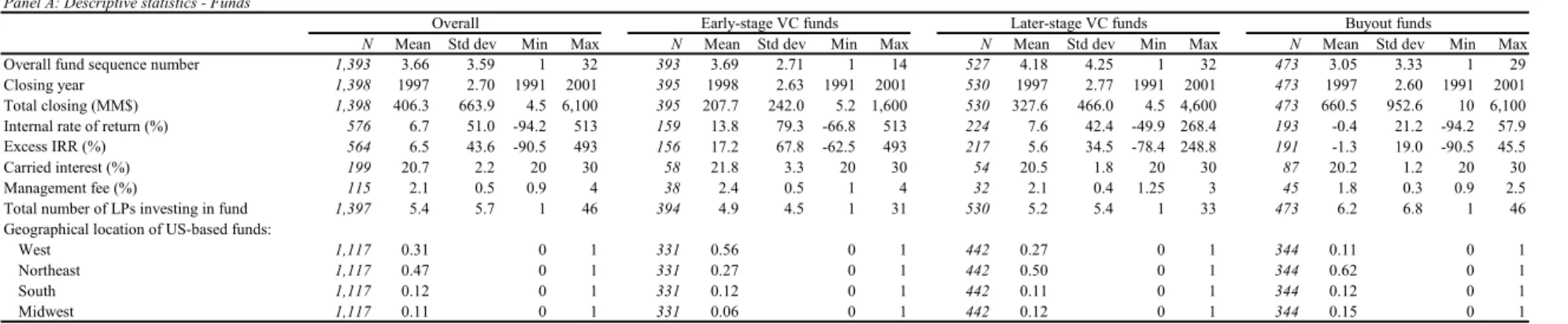

We collected information on fund size, stage, previous funds raised, etc., from the Asset Alternative Fund Database (included as part of their Galante Venture Capital and Private Equity Guide, but again not usually shared with researchers) and the Venture Economics ' online fund database. We distinguished between the overall score of the fund, and the order of this particular family of funds. For example, a mezzanine fund may be the eighth fund raised by a large private equity group, but the first to specialize in mezzanine investments.).

Our primary source of return data was the Private Equity Intelligence 2004 Private Equity Performance Monitor, which presents return data for over 1,700 private equity funds. We compiled information on the overall size of assets managed by the limited partner, each institution's length of experience with private equity investing, and location from Venture Economics' Private Equity Investor Directory and Alternative Asset Investment Resources Directory. We obtained information on senior management investors from the annual Pensions and Investments survey of the 200 largest US pension funds.

Analysis

We note that VCs tend to be somewhat older (the average sequence number of later VCs is 4.2), reflecting the longer history of this segment of the private equity market. Finally, we see that the assets in our sample are concentrated on the East and West coasts, with 47 percent and 31 percent of the US. First, the coverage of the Galante database appears to have become more comprehensive in the later part of the sample period.

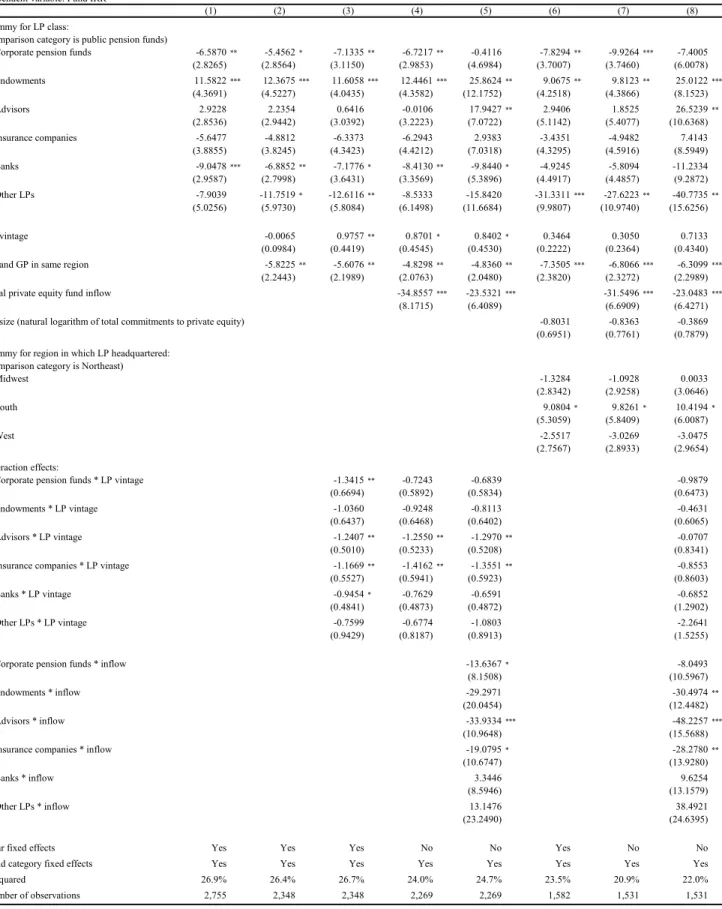

Second, the 1990s represent a period of massive growth in the private equity industry in terms of the number of funds raised and the number of investors participating in the industry. 5The year is expressed relative to that of the median LP in the sample, which began its In column (2), we include a dummy equal to one if the LP and GP are in the same region of the US and a control for the age of the LP's private equity program.

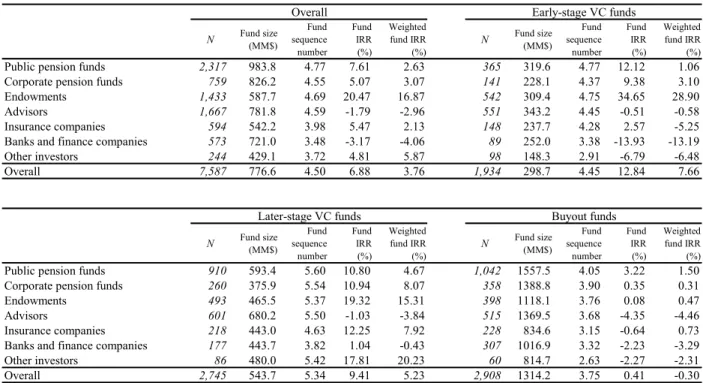

One of the most important decisions for LPs is whether or not to reinvest in the next fund in a partnership. For each fund in our sample, we identify whether the capital fund raised a follow-up fund of the same type. Public pension funds and insurance companies reinvest in around 60 percent of the funds where a next fund was raised.

They are followed by endowments and advisors, who reinvest about 50 percent of the time, while corporate pension funds and banks reinvest only 39 percent of the time. We see that LPs tend to reinvest in the next partnership fund if the current fund has a high IRR (on average these funds have an IRR of 25 percent). In column (1), we find a positive but barely significant relationship between reinvestment and past performance of the previous fund.

The picture changes significantly if we use this cut-off, as now funds and public pension funds tend to outperform the rest of the PPs, while banks and other PPs do worse. When we use excess IRR as the dependent variable, endowments perform significantly positively in two of the three regressions reported. Overall, these results suggest that some of the variation in the performance of LPs (in particular, funds of public pension funds) can be attributed to the preferential access of these LPs that have been in the industry for a long time.

LP-Specific Differences

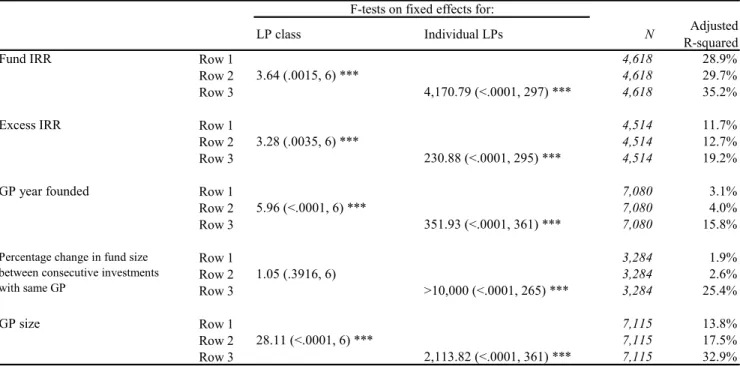

The first row in this table reports the R2 for a regression of the raw fund's IRR on controls for fund type and year fixed effects. We also find that an F-test on the joint significance of the LP fixed effects is significant at the 1% level. In the same way as before, we find that the R2 between the base model and the model with LP-type dummies increases from 11.7% to 12.7%, but when we include the individual LP fixed effects, the R2 goes up to 19.2% .

In each case, the increase in R2 is much larger if the individual LP fixed effects are included. To look at the heterogeneity in LP styles by class of LP, we pool the estimated LP fixed effects and calculate the mean, median, and standard deviations of these fixed effects by LP type. If the distribution of the estimated fixed effects is very tight around the sample mean, this would suggest that MPs do not differ greatly within MP classes, and vice versa if the distribution is very wide.

The standard deviation of fixed effects IRRs for advisors and corporate pension funds are 85 and 67, respectively, versus 60 and lower for other LP classes. We can now relate these different fixed effects to understand how these different investment dimensions relate to each other. Each cell in this table represents the correlation between a set of fixed effects, described in the top row of the table, and another set of fixed effects, described on the left side of the table.

The first cell shows that, not surprisingly, the correlation between raw IRR fixed effects and excess IRR fixed effects is very high (point estimate 0.88) and highly significant. When we look at the correlation of the raw fixed effects of IRR and other dimensions of LP investment style, we find that LPs that have high GP size fixed effects and higher fund size change fixed effects are associated with lower performance fixed effects. And finally, we document a positive (but weak) correlation between the LP IRR fixed effect and the GP founding year average fixed effects.

Looking at the other dimensions of LP investment style, we find that LPs that have higher fixed effects on the change in fund size (that is, those that invest in funds that increase their fund size more from one fund to the next) also have higher GP base year fixed effects, lower reinvestment fixed effects and a lower proportion of GPs in the same area.

Conclusion

Most interestingly, these different investment styles are systematically related to changes in LP performance. LPs that have higher IRR fixed effects also tend to invest in smaller, slower growing funds and have a smaller proportion of GPs in the same geographic area as the LP. Second, we noted in the introduction that varying levels of experience of LPs can exacerbate cycles in the private equity market.

The size of the fund refers to the total dollar value raised from all investors in the fund, the sequential number of the fund refers to the fund portfolio of the private equity firm, the IRR of the fund is the internal rate of return obtained by the fund from the fund's Private Equity Performance Monitor and weighted IRR, the internal rate of return is weighted by commitment to a fund as a fraction of each LP's total commitments to private equity funds. comparison category is public pension funds). FundInflowi is the year-over-year change in the amount of venture capital inflows in the country and in the year of fund i closing, and is a proxy for market conditions. LPageij is the number of years since the private equity program was established at LP j when it made an investment in fund i.

D_sameregionij is a dummy variable and = 1 if both LP j and the private equity firm managing fund i are based in the same US region (Midwest (includes Illinois and Ohio), Northeast (includes Massachusetts, New York, and Pennsylvania), South (includes Texas) and West (includes California)), otherwise = 0. Reinvestment is a dummy variable that takes the value 1 if LP j has reinvested in the next fund in the same family as fund i. FundInflowi is the year-on-year change in the amount of inflow of funds into the total private or venture capital in the country and in the year of closing fund i and is an approximation of market conditions.

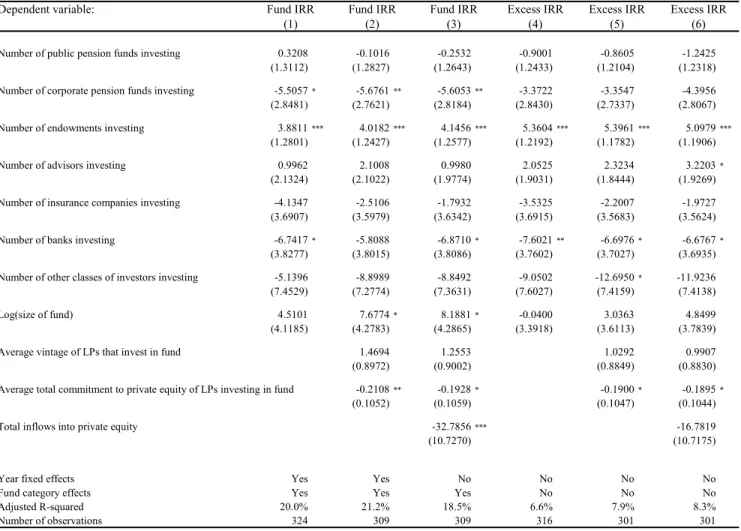

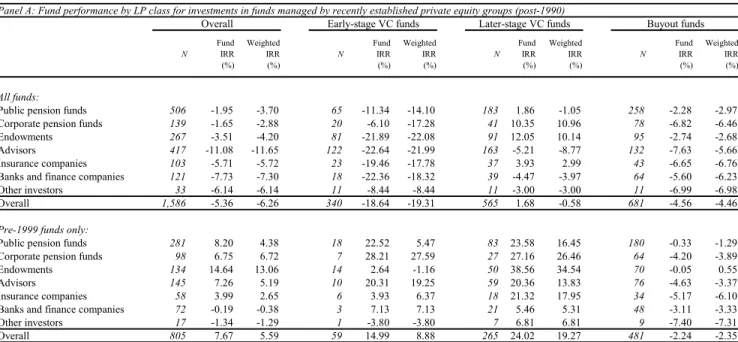

LPAge_reinvj is the age of LP j's private equity investment program at the time of the reinvestment decision. Panel A: Fund performance by LP class for investments in funds managed by recently established private equity groups (after 1990). FundInflowi is the year-over-year change in the amount of funds inflowing into venture capital in the country and in the year of closing of fund i, and is an authority for market conditions.

LPageij is the number of years since the private equity program was established at LP j when it made an investment in fund i. The table shows summary statistics for 417 LPs in the sample, measuring investment relationships for each individual LP and grouping by LP class. The table shows the results of fixed-effect panel regressions, where standard errors are clustered at the fund level.