LTROs (long-term refinancing operations) are part of the ECB's open market operations and have a long maturity. The exceptional role of the ECB during the crisis must be understood in the context of this unique period.

Banking union and the “Five Presidents’ Report”

The banking union represents the biggest transfer of sovereignty in Europe since the creation of the euro. In conclusion, the banking union represents the largest transfer of sovereignty in Europe since the creation of the euro.

Concluding remarks

In mid-2017, the European Commission will publish a white paper with a roadmap for the development of this second phase, so that 2016 will be a busy year and a key year in terms of political debate. Only then will it be possible to guarantee that it has the legitimacy and support necessary for the European project to develop successfully.

European leaders need to take a long-term view when dealing with these topics, making sure they look far enough ahead. Now, more than ever, there is a need to clarify the extent to which the countries in question are willing to transfer sovereignty and how quickly they want to move forward in building the Europe we want for the future.

Ángel Laborda and María Jesús Fernández 1

International context

In the case of Europe, this will be offset by the boost from the lower oil price, although the impact of this in the US.

Recent developments in the Spanish economy

However, this was mainly the result of the recruitment freeze in the public sector, as the slowdown was almost imperceptible in the case of market services. Total employment (in full-time equivalent work terms) rose by 2.4% in the last quarter of 2015, and 3% over the year as a whole, an increase.

Emilio Ontiveros 1

The need for this change is particularly urgent in the political context resulting from the recent general election. The article concludes by considering the limitations resulting from the international environment and the political situation following the December 2015 parliamentary elections.

Remedying the damage

Exceptionally expansionary monetary policy adopted by the ECB, the resulting depreciation of the euro and the cheapening of raw materials and consumer goods, especially hydrocarbons, represented a greater stimulus for the Spanish economy than for the eurozone average. Expansionary monetary policy adopted by the ECB, the resulting depreciation of the euro and the cheapening of raw materials and consumer goods, especially hydrocarbons, represent a greater stimulus for the Spanish economy than for the eurozone average.

Modernising the economy

This is an area that requires a long-term strategy with sufficient political support to ensure that it is not left at the mercy of future budget cuts. As stated by the European Union, it is also worth progressing in the direction of financial diversification.

Support from the international environment

Developments affecting China's economy and financial system have been a strong driver of the financial volatility recorded earlier in the year. Some of the imbalances that make the crisis more acute in the euro area have not yet been corrected.

Concluding remarks: The role of political uncertainty

The ECB's public debt purchases undoubtedly significantly moderate the potential negative impact of the difficulties in building a sufficiently stable coalition government. The same obstacles make it difficult to find solutions to the complex dynamics of the situation in Catalonia or to adopt decisions to agree new deficit and public debt targets with the authorities in Brussels.

Carmen López Herrera 1

The impact of the crisis on investment and loss of competitiveness in the

Despite the fact that the European economies are already starting a recovery, investments remain well below pre-crisis levels. Looking at the outlook for credit growth over a longer period, we see that the volume of new loans granted by banks to SMEs has stagnated since 2010, according to data released by the European Central Bank (ECB). .

EFSI structure: Main characteristics

Generating an investment-friendly environment through the European Investment Advisory Center and the European Investment Project Portal (EIPP). In parallel, work is continuing on the development of a portal – the European Investment Project Portal (EIPP) – which was planned to be operational by the beginning of 2016.

Potential impact for the Spanish economy

To this end, the EC has established, again together with the EIB, the European Investment Advisory Hub, a platform managed by the EIB to provide access to a range of advisory and technical support programs and initiatives. At national level: business, entrepreneur and guarantee credit lines offered by Spain's public credit institution, ICO, (such as FOND-ICO Pyme, ICO Innovación Fondo Tecnológico and Línea JEREMIE) and facilities granted by the Center for Industrial Development Technology (CDTI) for research, development and innovation projects.

Conclusions

At community level: the SME initiative (financing aimed at providing guarantees to financial intermediaries consisting of providing partial coverage of portfolios of loans extended to eligible SMEs), the InnovFin lines (with two parts, depending of project size, which can take the form of loans or guarantees) and financing under the scope of the COSME program for competitiveness of enterprises and SMEs. In this context, the role of the public sector, in collaboration with the financial sector, must be redirected to the indication of priorities from an economic and social perspective with a view to promoting productivity and social cohesion.

Carlos Ocaña 1 and Alice Faibishenko 2

A unique macro environment, stricter regulation and technology-related disruptive change represent the main actual and forthcoming challenges for the

In this context, the banking industry is paying close attention to the pressure on profitability resulting from the unique macroeconomic environment. The remainder of this article will focus on each of the three forces outlined above and how they are likely to affect the banking sector in general, with a particular focus on the situation in Spain in the final pages.

Unique macro conditions are affecting profitability in the short-term

However, more attention should also be paid to the possible consequences of regulatory and technological changes, which are equally important and ongoing. This means that the banking sector, among other things, needs to increase efficiency to improve its prospects, and new technologies should be an important part of this process.

Stricter regulation will likely affect profitability and lending capacity

However, the additional costs are expected to have an impact on the availability and terms of credit for the private sector. These include a review of the types of products and services offered, cost reductions, balance reductions, shifting certain activities to "shadow banking".

Disruptive technological change will present opportunities and threats

The new regulatory requirements are changing banks' business models as they adopt strategies to cope with the impact of the new measures. Other responses include foreclosure (as in the case of HSBC in the UK, ahead of the entry into force of regulatory measures to address this issue in 2019. At the European level, proposals for some form of foreclosure are pending, but not yet approved .) Finally, some banks may shift their geographic mix and try to take advantage of different Basel III implementation calendars in different regions.

Perspectives on the Spanish banking sector

This relatively high profitability may seem surprising, as the sector is one of the sectors most seriously affected by the crisis. The relatively high profitability of the Spanish banking sector as a whole may seem surprising, given that it is one of the more severely affected by the crisis.

Conclusion

In the case of the Spanish banking sector, some of these pressures, such as low interest rates, are particularly intense given the reliance on the traditional retail banking model. The Spanish Financial System in a New Political Era,” Spanish Economic and Financial Perspectives, January.

Santiago Carbó Valverde 1 and Francisco Rodríguez Fernández 2

In the context of a difficult start to 2016, the Spanish banking sectors´ recent performance on profitability and solvency indicators has been positive and

A difficult start to the year: Market and regulatory pressure

This is undoubtedly an important task, but the decentralization and the many layers of bureaucracy involved in the current banking union are such that compliance with the law takes up a vital part of the banking sector's human resources. The first is that the EBA aims to publish the results in the first quarter of the year.

The Spanish banking sector: Results and expectations for credit

As the supervisory authority emphasized, "the decision is based on the fact that all the analyzed information gives consistent and sufficiently uniform signals against the activation of the countercyclical capital buffer at this moment. More specifically, in terms of credit developments – and SEFO's monitoring of this – the latest published data show that year-on-year rates of change in Spanish private sector financing remained negative in January 2016 (Exhibit 2).

Fresh doubts about European banks?

The latest data shows that the ratio of non-performing loans to total private sector credit has fallen to 10.2% from a peak of 13.77% in 2013. As total credit rises and the balance of non-performing loans continues to decline, the ratio's decline will accelerate.

Transformation under way

The inevitable correction in the real estate sector has led many European banks to rethink their business and focus more on SMEs. This is a complex strategy, as it requires a change in the competencies of banks' human capital - to take a more proactive approach and offer more customized services - because this type of financing is especially penalized by solvency regulations.

Victor Echevarria Icaza and Francisco J. Valero López 1

This article analyzes the various regulatory proposals currently on the table for sovereign bond holdings and their potential effects. The following section anticipates the potential effects of the new regulations on banking activities and the functioning of the monetary union.

Regulatory framework

In the EU, however, this situation is replaced by the principle of equal treatment of the different. Leaving aside other potential formulations,5 there are currently two possibilities within the scope of the Basel III framework.

Effects of penalising sovereign bond holdings

This instrument would at least mitigate the negative impact of the introduction of haircuts on holdings of government bonds. If the source of stress is a specific institution that is not considered 'systemic', the units are.

Joaquín Maudos 1

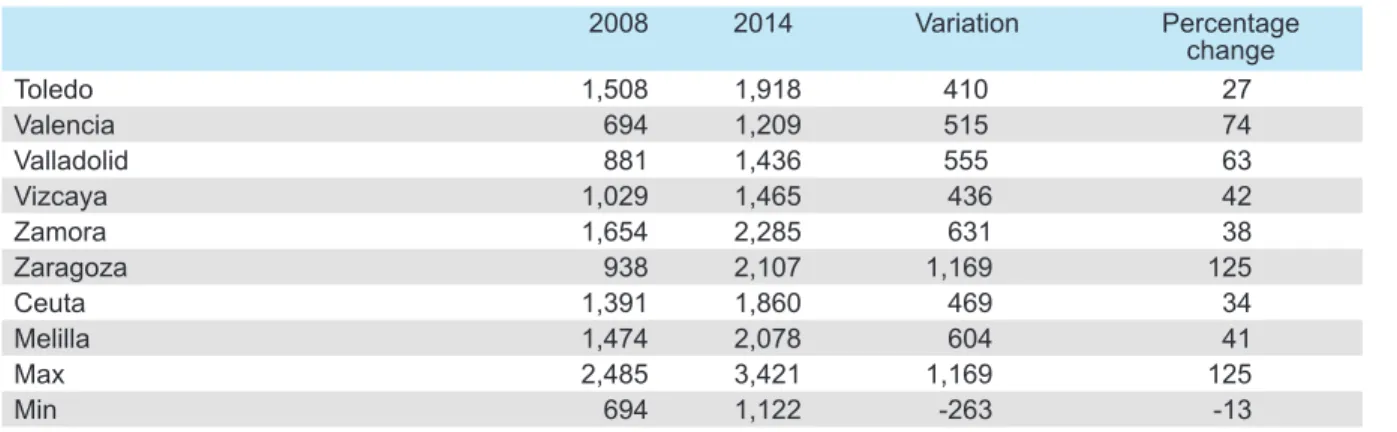

The profound restructuring of Spain´s banking sector has resulted in a significant increase of concentration across almost all provinces. Despite the much needed

The second focuses on a provincial level analysis of bank concentration in Spain, after analyzing the differences in intensity of the adaptation that took place in the branch network. The next section analyzes the possible impact of the current levels of concentration in terms of competition, based on the concentration indices compiled, taking the thresholds used in the United States as a benchmark.

Trends in bank concentration in Spain in comparison with the European

The concentration of the Spanish banking market was below the European average in 2008, although by the end of 2014 it had risen above it. The reduction in the number of competitors has led to an increase in the concentration of the European banking market.

Concentration of provincial banking markets

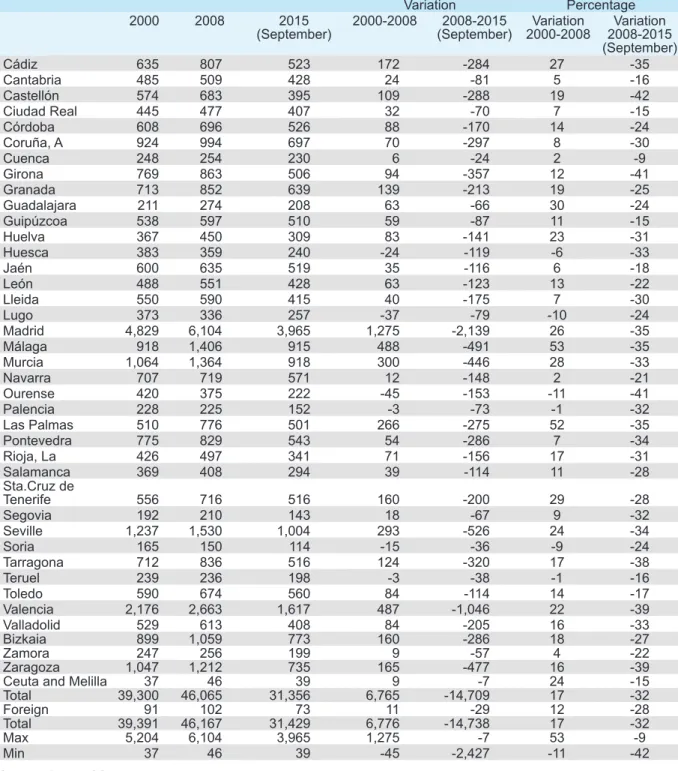

Although this increase is more than double the EU15 average in terms of sharp cuts in the branch network, Spain remains second in the EU ranking in terms of branch network density. Since the beginning of the crisis, the network has shrunk in all the provinces of Spain, without exception.

Is the increase in the level of bank concentration in some provinces a

Cutting off branch networks was a particularly important part of this strategy, as the number of existing offices at the time of the outbreak of the crisis was not compatible with efforts to deleverage the Spanish economy. The differences are even greater when it comes to the increased concentration that has taken place during the crisis.

José García Montalvo 1

The recovery of the Spanish economy in 2015 allowed the financial sector to significantly reduce its volume of troubled assets. However, progress was

Recent trends in the property sector and lending

Indeed, judging by the development of the prices of the Ministry of Public Works and Transport in Exhibit 1, the overvaluation of the past has given way to the undervaluation of today. The data from the beginning of the year show a sharp drop in confidence, driven more by expectations than by the current situation.

The banks’ property exposure

Part of this decline in the share of credit for productive activities in the real estate sector was offset by the increase in lending to households for home purchase and renovation. The fall in lending to the property sector was similar (13%), although the pace of reduction was considerably slower than the previous year (20%).

Trends in the NPL rate

Nevertheless, considerable differences remain in the rate of non-performing loans broken down by loan purpose (Exhibit 6). The recent decline in the NPL rate was more pronounced among large companies (22%) than SMEs (14.3%).

Trends in foreclosures and refinancing

The NPL rate among businesses in the construction industry and property sector is above average, and there is also a significant difference between large companies (24.8%) and SMEs (35.1%). As in the case of non-financial corporations as a whole, the decline in the NPL rate is greater among large companies than SMEs.

Property risk in SAREB

The improvement of the Spanish economy in 2015 allowed the financial sector to significantly reduce the volume of non-performing assets. On the contrary, it is predictable – based on the 2015 results presented by the main banks – that the confiscated real estate has remained stable at the same level as in the previous half-year.

Prepared by the Regulation and Research Department of the Spanish Confederation of Savings Banks (CECA)

Bank of Spain Circular on supervision and solvency, completing the

- Scope

- Exposures to public sector entities

- Capital buffers

- Internal organisation

- Internal capital adequacy assessment and treatment of risks

- Financial conglomerates

- Disclosure requirements to the market and the Bank of Spain

- Transitional and repealing provisions

Prepared by the Regulatory and Research Department of the Spanish Confederation of Savings Banks (CECA). Credit institutions will have three months from the entry into force of the circular to publish information on their corporate governance and remuneration policy on their website.

Bank of Spain Circular amending the Circular on information regarding

In the case of securitizations formalized between July 7, 2014, and the entry into force of the circular, originating entities that wish to apply the treatment determined in CRR when calculating their capital requirements for these securitizations must provide the Bank of Spain with information on these securitizations provide. using the standard format included in the Circular. The Circular repeals the existing Solvency Circular, although it leaves certain aspects of it in force.

Draft Bank of Spain Circular on amending Accounting Circular

When calculating value adjustments and provisions for credit risks due to insolvency, the estimates must be consistent with the downgrading of the risk category and must take into account the existence of effective guarantees. In addition, the value of the insurance will be calculated using the deductible in the insurance assessment.

Funcas Economic Trends and Statistics Department

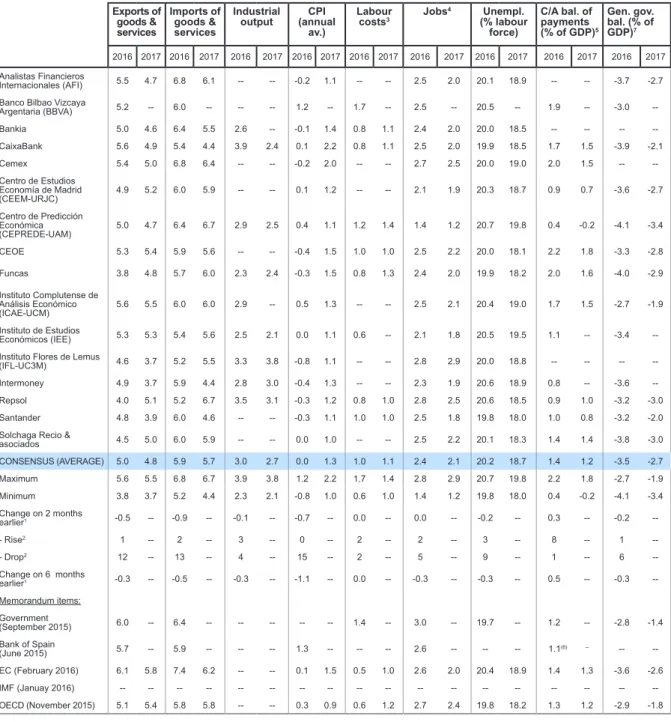

The forecast for 2016 remains unchanged at 2.7%

The forecast for 2017 is 2.3%

Strong growth in the manufacturing industry

Falling oil prices mean inflation is lower than expected

Positive trend in employment

The current account surplus will shrink in 2016

The government deficit will overshoot the target by a few tenths of a percent

The perception of the global economy remains negative

Long-term interest rates are too low

The euro continues to depreciate

Fiscal policy is neutral

1 Change in percentage points between the average of the current month and that of the previous two months (or six months ago).

KEY FACTS

Annual percentage change Graph 2.4.- VAT, sectoral structure Share of added value in basic prices. Annual percentage change Graph 4.4.- Functional distribution of income Percentage of GDP, 4-quarter moving averages Graph 4.2.- National income, consumption.

KEY FACTS: 50 FINANCIAL SYSTEM INDICATORS – FUNCAS

Highlights

Commentary on "Financial savings and debt:" During the third quarter of 2015, there was an increase in financial savings to GDP in the overall economy that reached 2.1% of GDP. There has been a fall of €1.96 billion in the use of the Eurosystem by Spanish banks since January.

Spanish banks: Improved performance in the face of financial turbulence