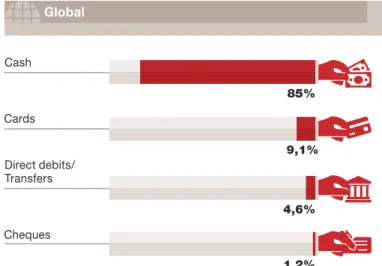

Another trend worth mentioning in the microcosm of payment means is virtual currencies. In any case, one of the fundamental characteristics of means of payment in the world is geographical diversity.

History of means of payment (and the economy)

The next leap in technology and concept in the history of means of payment was the advent of the credit card. The advent of the Internet in the 90s was also a radical breakthrough in payment habits, as it made it possible for the first time to carry out all kinds of transactions from the comfort of your own living room.

Is a world without cash

The disappearance of cash would bring counterfeit money to a sudden death, limit tax evasion and make it possible. The benefits are clear, but removing cash also involves many difficulties and contraindications, no.

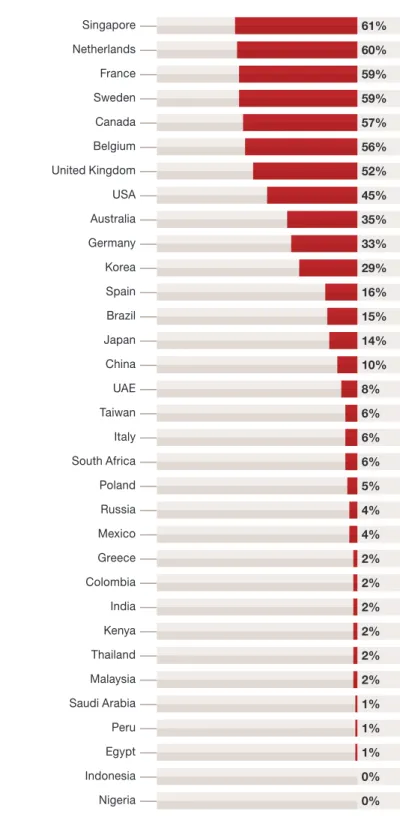

Therefore, the trends and future of the means of payment are determined by the preferences of the customers (their needs, inclinations and wishes). Source: Study: The future of means of payment in Spain, by PwC and IE Business School. Source: The future of means of payment in Spain, by PwC and IE Business School.

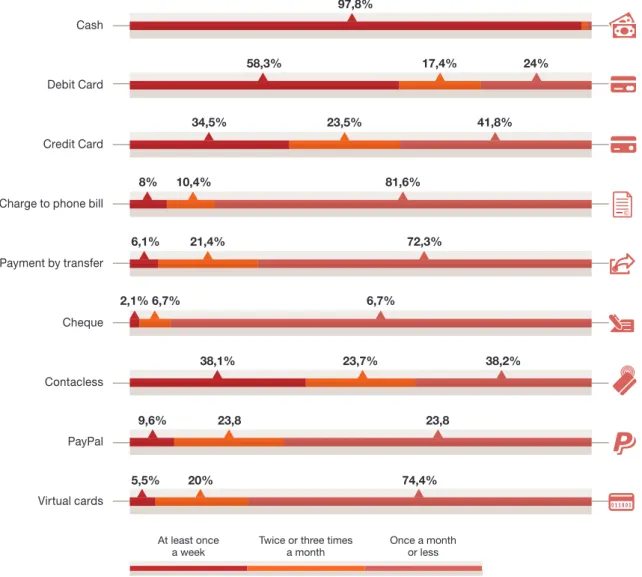

About how often you used the following payment methods in the last six months. PayPal excels across the board (scoring between 7 and 8 out of 10) and is the highest rated payment method among respondents. There are no major differences between the various payment methods assessed (cash, credit card, debit card, check, transfer, mobile bill, PayPal, contactless card and virtual card).

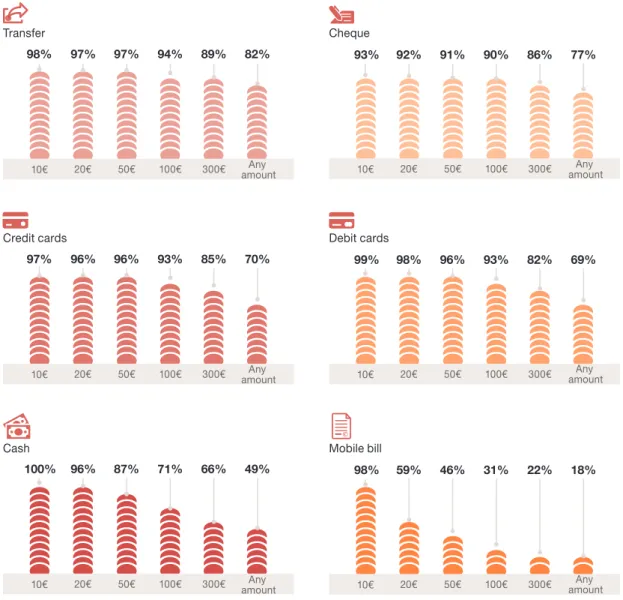

How much are you willing to pay to use the following means of payment? Now let's look in detail at the key players of the payment system and how they behave in the light of the.

Bitcoin, somewhere between success and mistrust

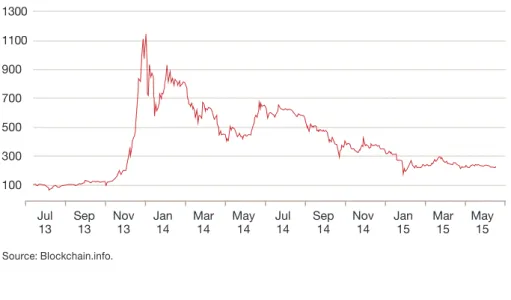

The so-called virtual currencies have gained popularity as a means of payment as the needs for the exchange of virtual goods and services have increased. Those who pay each operation also have the option to tip the miners in the form of a fee. According to figures from the beginning of March 2015, just over 200 physical stores accept Bitcoin in Spain (85 in Madrid), while there are around 6,300 in the world.

But to become a mass means of payment, it would need to address price volatility, which fuels speculation and leaves users unsure of how much they are paying for what they buy. With this background, what is the future of bitcoin and other cryptocurrencies as a means of payment. Experts believe that it could become a commonly used electronic payment method given its good fit with the Internet ecosystem.

The wallet war

In the world of means of payment, the market has seen the arrival of bracelets with NFC functionality, that is, another method is the payment gateway, which is a service for the exchange of encrypted sensitive information between the buyer, the seller and the banks involved is at the . This is particularly useful for professionals who work in the client's home or in mobility conditions, such as taxi drivers.

Trends in the means of payment are driven by the emergence of new technologies, which are normally not visible to the customer, but whose development and implementation are crucial to the success or failure of any industry initiative. What if my battery is empty?" The answer must come from the industry, which has made astonishing strides in mobile phone capabilities in just a few short years; It should ensure the security of the transaction and the resources and devices involved in the payment process.

The ideal means of payment

But we know that there is a certain degree of consensus among experts about the features that a new means of payment needs if it wants to conquer the market. It must be able to pay in physical stores and via the Internet. Some believe that in the not-so-distant future, people will be going home without a wallet.

This question was asked in an investigation conducted by PwC in the United States and included in the report entitled Opening the Mobile Wallet. On the one hand, the citizens who participated are willing to use mobile wallets to replace certain documents or devices. Furthermore, survey participants were asked about the likelihood of using mobile wallets to make payments or move money.

Mobile wallets, why?

Sectoral regulations. These are generally promoted by official

In short, the objective is to square the circle, which must combine reasonable market control with the deregulation necessary to promote its efficiency and ensure its development. In Europe, the general regulation of the sector is entrusted to the Payment Services Directive (PSD), which was implemented in 2009 and whose second version (PSD2) is under negotiation in Europe. The directive is the framework that enables the development of the Single European Payments Area (better known as SEPA), an initiative of the banking sector that supports it.

In the United States, the role of the European PSD is played by the veteran Electronic Funds Transfer Act, which was passed in 1978. In developing countries, where the banking infrastructure is often weak, financial inclusion is one of the priority objectives of the regulation. The data security standard par excellence for payment cards is the so-called Payment Card Industry Data Security Standard (PCI DSS). Born in 2004 from the merger of the data protection programs managed by Visa, MasterCard, American Express, Discover and JCB, this standard is mandatory for all participants in the payment process that accept, store or transmit card data, i.e.

Channel or product

The standard was developed by a. administrative body: the PCI Security Standard Council, which actually acts as a supervisor of the payment cards subsector. Communication standard for financial institutions (ISO 20022) Mobile payments (SecurePay) Authentication in means of payment. SecurePay-Third Party Providers) Real-time payment. On the one hand, there are completely non-legal markets, beyond the control of the authorities and the industry itself.

This is the case with the so-called cryptocurrencies (bitcoin being the main example, but not the only one), which by their very nature are out of control. General rules for regulating means of payment in the European Union are included in the Payment Services Directive (PSD). However, in 2013, the European authorities realized that technological progress required more complete market regulation and launched a double proposal: to initiate a second version of the PSD (so-called PSD2) and to develop a regulation for exchange fees on card transactions.

Europe

In Spain, the Ministry of Finance decided in April 2015 to consider Bitcoin as a means of payment. The new policy is expected to be adopted in the course of 2015 and, after the transposition process, can be fully implemented in the Member States in 2017.

The regulation could be given the green light in 2015 and, as it is subject to direct application, could enter into force in 2016. The draft regulation on exchange rates in card transactions (the commissions that the retailer's bank pays the bank of the buyer), on the other hand, sets a number of thresholds: 0.3% of the purchase value in credit card transactions and 0.2% in debit card transactions. In the latter case, Member States may lower the threshold and apply commission limits in absolute terms.

The second aspect of non-regulation has to do with the cracks or gaps in regulated markets. It was introduced in 2009 and aims to provide the legal basis for the creation of an internal market for payments. It regulates third-party providers (payment initiation services) and forces banks to give them access to their infrastructure.

The draft of the new Payment Services Directive (see enclosed information) looks at the inclusion of third party providers in European regulations. The purpose of capping exchange costs is that said restriction forces a reduction in the commission that banks charge the retailer (the so-called discount rate, which is not regulated), which could also benefit the end consumer. The European Commission hopes that lower rates will save the European payment system 6 billion euros a year.

Regulation of the much-feared third party providers

Security, a strategic problem Historically, security has been key in the development of means of payment. This is not true now, but it was in the past: in the early versions of the technology, there was a possibility that this kind of data could be stolen. Samsung, which will launch its own payment method in the summer of 2015, has also announced that it will use the fingerprint as a means of authentication.

This collaborative effort to improve transaction security has resulted in the creation of various bureaus and. Some regulators of the financial system as a whole have also taken major roles in the security debate. Hacker attacks have affected many of the links in the payment chain (commercial companies, processors, banks, governments, mobile operators..) and they have mainly focused on the United States.

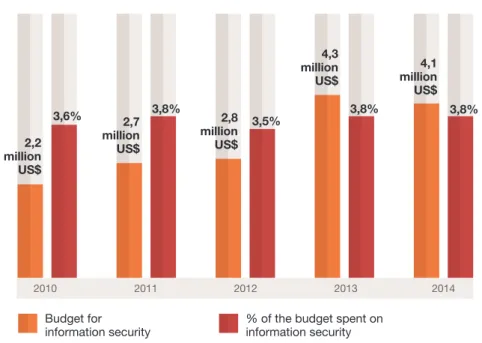

They still say security is expensive

After the incident was discovered, there has been an unusual increase in prepaid card fraud in some parts of the US. The payment method of the future will be universal, ubiquitous, easy, practical, cheap, secure and will include a rich user experience. But with the available information, it is possible to make a number of recommendations for all actors who are looking to play an important role in the process and want to take a share of the business.

Since the advent of the Internet, he has had a major influence on the financial services and other consumer sectors. In developing countries, the use of non-cash means of payment is limited, but growing rapidly in the heat of technological advancement and the rise of the middle class. As in other areas of the financial services industry, regulations are becoming increasingly strict and players must participate in the process as much as possible.