E-Banking vis-a-vis Traditional banking in Nigeria

Electronic banking services

Electronic banking in an outgrowth of ICT, and it offers the classic and current way of banking services. It should be noted that almost all the 25 banks that survived the 2005 consolidation exercise in Nigeria have adopted electronic banking services in one form or another, although the level of adoption has mostly been at low or basic interactivity and functionality level. There is abundant evidence that electronic banking systems are expected to serve the purpose of reducing bank hall, reducing waiting time, making customers more liquid and above all ensuring a cashless society.

The emergence of electronic banking in Nigeria has also brought some products for easy and efficient banking transaction, these products include efficient express service (EQS), electronic payment among others. However, to ensure effective customer satisfaction; Nigerian banks must be ready to embrace the latest technologies brought about by the advancement of ICT. Given the current low rate of adoption of e-banking, it is doubtful whether Nigeria will achieve its stated goal of becoming a key player in ICT and e-banking by 2020.

Be that as it may, customer satisfaction with banking services is influenced by the perceived quality of products/services and other related delivery processes.

Important of ICT in E-banking Operations

ICT directly affects how managers decide, how they plan and what products and services are offered in the banking industry. It is a concept that has a remarkable effect on almost all aspects of human endeavour. Ovia (2005) outlined some banking services transformed by the use of ICT such as account opening, customer account mandate and transaction processing and recording.

Information and communication technology has provided self-service facilities (automated customer service machines) from which potential customers can complete their account opening documents directly online. ICT products in use in the banking industry include Automated Teller Machine, Smart Cards, Telephone Banking, Electronic. According to Ovia (2001), banking in Nigeria is increasingly dependent on the spread of information technology and that the IT budget for banking is far greater than any other industry in Nigeria.

He claimed that the online system has facilitated internet banking in Nigeria as evidenced by some of those who launched websites. Woherem (2013) revealed that since the 1980s, Nigerian banks have performed better in their investment profile and use of ICT. systems than the rest of the industrial sector of the economy. ADCG) on IT diffusion in Nigeria shows that banks have invested more in IT, have more IT staff, more installed base of PCs, LANs and WANs and better connectivity to the Internet than other sectors of the Nigerian economy.

However, the study pointed out that while most banks in the West and other parts of the world have at least one PC per staff, Nigerian banks are seriously lagging behind with only a PC to capital ratio of 0.18. Ovia (2005) opined that the ICT revolution has caused the banking sector to change from the traditional way of doing business to supposedly better ways through technological innovation that improves efficiency. ICT can increase efficiency through its use, and banks have recently been encouraged by the rapidly falling prices of ICT devices.

This requires proper analysis to determine the type, nature and extent of ICT products required for efficiency and effectiveness. Given the role that technology plays in modernizing the banking sector, there is no doubt that the future of the Nigerian banking industry rests heavily on its swift and rapid adoption of ICT. Experiences from other countries have paid greater attention to the application of ICT to the activities of.

Theoretical Review

The diffusion of innovation theory states that diffusion of innovation occurs when potential adopters become aware of the innovation, assess its relative value and make a decision based on their judgment, implement or reject the innovation, and seek confirmation from the adopter or rejection decision. The theory consists of three components: 'the innovation decision process, characteristics of an innovation and characteristics of the adopter (Bates, Manuel & Oppenheim, 2007). The innovation decision process categorizes the steps an individual takes from realizing an innovation, through formulating an attitude toward the innovation, to deciding whether or not to implement it.

The characteristics of an innovation have an impact on the likelihood of acceptance and adoption, and also on the rate at which this process develops. The Technology Acceptance Model (TAM) is similar to diffusion of innovation theory, but it places more emphasis on psychological predispositions and social influences such as belief, attitudes and intentions. The range of influential factors in the use of innovations includes: the associated 'cost' (personal and institutional), the availability of necessary 'resources' (money, equipment, training, time, previous experience and relevant skills) and the 'value' of the innovation (Bates, Manuel & Oppenheim, 2007).

The adoption of electronic banking is a transformation of practice—a practice of moving from analog or manual operations to those of machine-enabled or electronic processes.

Empirical Review

Moreover, none of the empirical works focused strictly on service delivery; not even the studies in Nigeria. The questionnaire was supplemented by oral interviews with few respondents to validate some of the answers in the questionnaire. The population of the study consists of the entire staff of the Six (06) Zenith Bank branches in Enugu metropolis, Enugu State.

Due to the nature of the study population which does not require any strict randomization, the researcher adopted this. The questionnaire was distributed to some respondents in the population to assess their level of understanding of the questions in the questionnaire. The data collected from the bank's customers on the same topic is presented in Table 4 below.

Table 4 shows that 73 or 97.3 percent of the customers surveyed agreed that there are sufficient technological capabilities at Zenith Bank to leverage the benefits of ICT. However, 2 to 2.7 percent of customers surveyed believed that the bank does not have sufficient technological capabilities to leverage the benefits of ICT. To collect data on this topic, question 6 is intended for the customers and question 12 for the bank's employees.

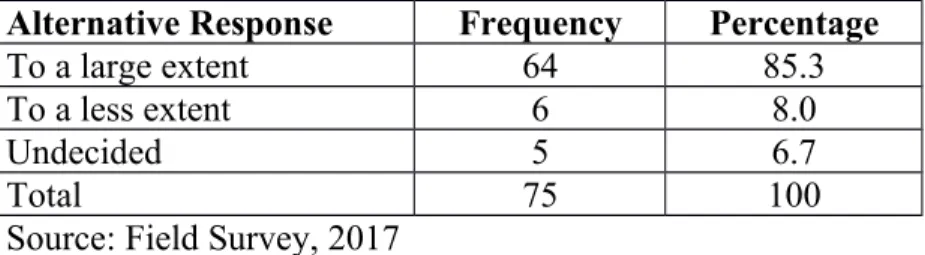

The results from Table 6 show that 80 or 96.4 percent of the employees were of the opinion that the bank had introduced ICT to a large extent, while 3 or 3.6 percent of them were of the opinion that the bank had only introduced ICT to a lesser extent. With the question, we wanted to find out whether the bank's services have improved since the introduction of ICT in the bank's operations. The results from Table 8 show that 68 or 90.6 percent of the surveyed customers agreed that there are structural problems preventing banks in Nigeria from adopting and implementing e-banking in their operations.

4 and 5.3 percent of clients, however, did not agree that there are structural problems that prevent banks from accepting and introducing electronic banking in their operations, while 3 or 4 percent were unspecified. The result of the employees' assessment of whether there are structural problems preventing banks from adopting and implementing electronic banking is presented in Table 9 below. The result from Table 10 shows that a total of 43 respondents or 33.5 percent of the respondents comprising customers and bank employees were of the opinion that the high cost of electronic banking equipment inhibits the adoption and deployment of ICT by banks in Nigeria.

26 respondents or 16.4 percent felt that the lack of skilled and technical manpower is a hindrance to the adoption and deployment of e-banking in the banking sector in Nigeria, while 22 or 1.3 percent of the respondents felt that the high maintenance cost of e-banking equipment inhibits banks in Nigeria. take over and introduce electronic banking into their operations. In addition, 30 or 18.9 percent of respondents cited frequent power outages that increase operating costs and inhibit banks from accepting and.