Our analysis suggests that devaluation is a major trend in Europe as total assets of the banking sector in the eurozone fell by 8% in 2013. Ultimately, the costs of the lack of restructuring are borne by the employees in those countries, while the structure.

Upcoming stress tests reveal EU supervisor´s perceptions

As shown in Table 1, the negative scenario appears to be "softer" for Spain compared to the average of the euro area or the European Union for most of the indicators considered with the sole exception of unemployment. This means that, at least when it comes to economic growth, the future for Spanish banks does not impose further macroeconomic pressures compared to other EU banking sectors, where, on the other hand, bank restructuring is still in progress. waiting

Does it pay to restructure a banking sector?

Our estimates show that some economies of scale have emerged in recent years, being much larger in countries where restructuring has been more intense, as in the case of Spain. Overall, our analysis suggests that the intensive restructuring process that Spanish banks have undergone in recent years has imposed many sacrifices, but may also bring many competitive advantages in the near future.

The high level of Spain´s private debt, particularly of non-financial corporations, is often cited by international institutions as the main obstacle to a sustained

Introduction

Spain's high level of private debt, particularly of non-financial corporations, is often cited by international institutions as the main obstacle to sustainable development. The results are highly sensitive to parameters such as the percentage of debt converted to capital or the loan coverage level.

Current situation

At the same time, between 2008 and 2013, the Spanish banking system reduced the outstanding loan balances of Spanish companies by approximately 240 billion euros by servicing debts, enforcing guarantees (generally real estate) and, above all, transferring real estate. credit for. The obligation to make provisions for the credits of this sector at rates that are much higher than for other production sectors (in accordance with Royal Decree-Law (RDL) 2/2012 and RDL 18/2012), as well as the transfer of a large share of these funds to SAREB, resulted in gross loans on banks' balance sheets amounting to slightly more than EUR 110 billion (EUR 75 billion net).

Opportunities arising from RDL 4/2014

2 For the part of the loan that does not exceed the value of the collateral. Standard risk when there are objective factors that lead to the conclusion that the remaining amounts owed are likely to be collected after the refinancing agreement is used.

Channels of impact on profit and loss and solvency of banks

Based on these assumptions, all three cases produce a positive result after the application of the refinancing agreement, which generates capital for the bank. Sensitivity analysis: Impact on equity of the conversion of debt into equity according to percentage of conversion and level of coverage of the initial loan.

Conclusions

In short, in most cases the impact of the new treatment of restructured transactions will be positive for the banking sector for two reasons: i) it facilitates the debt restructuring of viable companies, i.e. the management of risk, and (ii) an adequate analysis of operations and of their most sensitive aspects can improve banks. For the banking sector, the impact of the new treatment of restructured transactions will in most cases be positive as it facilitates the debt restructuring of viable companies, and encourages an analysis of operations and of their most sensitive aspects, which can improve banks' capital positions. .

Sara Baliña and Ángel Berges 1

Spain´s private sector continues its deleveraging process in contrast to increasing leverage in the public sector. Given heavy reliance of the private sector on bank

Closing the external financing gap

Debt dynamics: Private versus public

However, in terms of the aggregate sector, it is much more accurate to use gross debt for several reasons. A second reason to use gross debt at the aggregate sector level concerns financial stability concerns.

Debt instruments: Bank based/

From those figures we can conclude that the Spanish economy entered the crisis with an overall debt level of 325% of GDP, most of which (about 290% of GDP) is private debt and only 36% of GDP in public debt. Six years of crisis caused an overall increase in the debt of the Spanish economy to almost 350% of GDP, with an intense rebalancing between private and public debt.

Bank debt is largely unchanged as a percentage of GDP as a result of the very different dynamics in the private and public sectors. Non-financial corporations and households have reduced their bank debt by around 10% of GDP since the start of the crisis, while the public sector has increased its bank debt by almost the same order of magnitude over the same period.

Spanish debt dynamics by instrument and institutional sector (% GDP)

Since the beginning of the crisis, almost 50% of GDP has been generated by the public sector through the issuance of securities. Both in households and in the public sector, this form of financing was not.

Spanish debt: Where is it heading?

Despite having performed much better than bank finance in the last six years, their role as debt providers is only relevant to the public sector, as they represent almost 80% of total outstanding debt. Private devaluation, however, will continue at a slower pace than has been the case in recent years.

Joaquín Maudos 1

As a result, specific measures should be implemented for SMEs to improve their access to finance. For SMEs in the manufacturing structure of the Spanish economy, improving their access to finance is essential to support the recovery.

Firms’ financial structure: SMEs vs

Although there are arguments justifying the restrictions on SMEs' access to external finance, the data presented in this article suggest that the cost increase they pay is excessive. In this context, this article examines the differences that exist between SMEs and large Spanish businesses in terms of access conditions, and compares the situation in the different countries of the euro area.

In terms of the composition of external financing, the main difference between large companies and SMEs is in the relative share of bank financing. In contrast, trade credit represents a share of external financing that is somewhat higher among SMEs than large companies (16.1% vs. 15.3%).

Size and cost of bank finance

This is 11.5 percentage points (pp.) more than among large companies (Exhibit 1) and is the first indication of the difficulties SMEs have in obtaining external financing. Non-bank lending (including intra-company loans) is more important among large companies (41.3% compared to 37.6%), as is the case of debt financing, although it is slightly less important in the case of large Spanish companies (1.5% external finance).

Business size and availability of finance

In general, the problem of access to finance is worst among SMEs, with the difference between large companies and SMEs also significant (12 pp.) in France. Only in Germany is there no difference between large companies and SMEs (6% identify access to finance as their main problem).

Fear of rejection: An indicator of credit constraints

In the case of Spanish firms, 18% of SMEs identified access to finance as their main problem, compared to 16% of large companies. Of the countries represented, the country in which the majority of SMEs report this problem is Italy (19%, 1 pp. more than in Spain).

Availability of bank credit and borrowing conditions according to company size

Increase/decrease in non-interest costs

Increase/decrease in collateral

The data for Spanish SMEs contrasts sharply with those for SMEs in Germany and France, where most companies believe banks have cut their interest rates. Spanish SMEs have also seen the most increase in collateral requirements when applying for bank loans, with the net number of respondents to whether they have increased or decreased by 37 percentage points.

Firms’ opinions over banks’

In the case of non-interest costs, SMEs, especially those in Spain, have seen the biggest increases. In the eurozone, as in all countries examined, SMEs have seen their costs increase to a greater extent, with net percentages of positive responses to this question being higher in all cases among SMEs than large firms.

Firms’ expectations about the recovery in credit

Bank credit to new financing operations: Large firms vs. SMEs

In the case of smaller loans, credit has been recovering since May 2013, with the value of new credit rising. For larger loans, the situation is diametrically opposite, as apart from a one-off positive year-on-year rate in December 2013, the rate has been negative in all other months since May 2013, falling to -16.7%.

Main messages and conclusions

Finally, the recovery in SME lending revealed by the latest data on the progress of new loans is in line with the improvement detected in the ECB's latest survey on access to finance. In addition, the perception of Spanish companies (and those in the euro area) about future expectations regarding the availability of bank financing has also improved, although much more so among large companies than SMEs.

Santiago Lago Peñas 1

The Spanish government´s fiscal consolidation strategy through 2017 looks promising, but falls short of guaranteeing debt sustainability

The 2013 budget and the government´s outlook for the period 2014-2017

As a result, the ratio relative to GDP is expected to decline and thus the degree of achievement of the 2013 targets is expected to increase. Indeed, as interest payments are expected to rise by half a point, the spending adjustment will come in at five percentage points of GDP (4.8%).

Is Spain´s fiscal consolidation process credible?

Therefore, most of the fiscal adjustment depends on the reduction in the ratio of expenditure to GDP. Note: (1) The expenditure figures for Spain do not include the one-off costs of the financial reform.

Is the adjustment enough? Public debt sustainability

In real terms, however, autonomous regions' spending is currently more than 20% lower than at its peak in 2009 and it is difficult to see where further cuts can be made without jeopardizing the basic pillars of the welfare state. This calls for stronger action by the European Central Bank (IMF, 2014) and fiscal expansion in those countries with sufficient room for maneuver.

Concluding remarks

The economy of the Eurozone in general and the Spanish economy in particular must keep the fear of deflation at bay. In this connection, Annex 2 points to the need for a more balanced use of measures on the expenditure and revenue side to reduce the public deficit than proposed in the government's budget consolidation scenarios.

SEFO - Situación Económica y Financiera de España vol. 2013), “La nueva estabilidad fiscal en España: un enfoque centralizador”, Informe sobre el federalismo fiscal en España 2012, IEB, Barcelona. Ministerio de Hacienda y Administraciones Públicas (2013), Informe sobre la Actuación Eficaz Adoptada por el Conjunto de España por las Administraciones Públicas, 1 de octubre de 2013. 2014b), Actualización del Programa de Estabilidad.

Daniel Fernández Kranz 1

Eliminating composition bias reveals there has been some flexibility of wages in Spain in response to the economic crisis. However, the distribution of the

This article provides evidence of the wage adjustment process in Spain after removing composition bias. The salary information comes from people who worked full-time for the same company continuously during the first five years of the economic crisis.

Main findings

A general pattern in the data is that wages have fallen more in jobs that previously paid higher wages at the beginning of the economic crisis. This last piece of evidence contradicts recent claims that the economic crisis has increased income inequality in Spain.

Wage adjustment across types of jobs

Figure 2 shows the change in salaries of jobs according to the type of contract (permanent or Exhibit 2. Exhibit 3 shows the evolution of salaries of jobs grouped by firm size.

Wage adjustment across jobs defined by worker characteristics

Since then, the wages of fixed-term jobs have fallen more than the wages of permanent jobs. Instead, wages of jobs with less-skilled workers lost an average of 4.2% during the same time.

Wage adjustment by sector and region of employment

Finally, Figure 6 shows that jobs with older workers lost 5.4% compared to jobs with workers under 30, which lost 3.5% in real terms.

Wage trends in the public and the private sectors

All things considered, the wage adjustment process has been more intense in the public sector than in the private sector since 2008. Exhibit 9 shows how differently wages in the public sector have behaved compared to wages in the private sector.

Regression analysis

This contrasts with wages in the private sector, which have fallen a more modest 3.4% since their peak in 2010. Overall, the wage adjustment process has been more intense in the public sector than in the private sector since 2008 , with public sector jobs losing 2.4% compared to 0.8% in the private sector.

Prepared by the Regulation and Research Department of the Spanish Confederation of Savings Banks (CECA)

National Securities Market Commission (CNMV) Circular on requirements

Royal Decree-Law adopting urgent measures on the refinancing and

Amendments to the Bankruptcy Law

A revision of the system of judicial confirmation of refinancing contracts was carried out, with the scope of application being extended to all types of financial obligations, except creditors for commercial transactions and creditors for public obligations. In order for the value of the guarantee not to decrease in the event of the debtor's default, special rules have been established that allocate the remainder to the creditor.

Other provisions

Similarly, creditors who have signed a refinancing agreement for obligations assumed by the debtor in connection with the feasibility plan are not considered beneficial directors. In addition, a measure was put in place to prevent overburdening of certain minority interests in syndicated financing.

Draft Bill of a law to promote corporate finance

The draft law adjusts the legal framework applicable to financial companies due to the loss of credit institution status in accordance with CRR and CRD IV. Promoting the operation of the Alternative Exchange (MAB) by facilitating the transition of listed companies to this alternative trading platform.

FUNCAS Economic Trends and Statistics Department

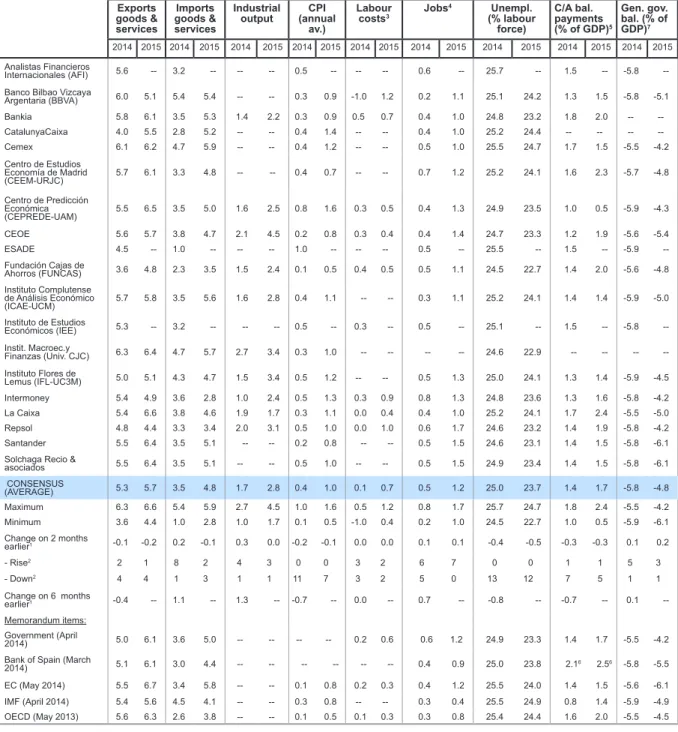

The growth estimate for 2014 has been raised a tenth of a percent to

The forecast for 2015 has risen to 1.9%

Further improvement in the industrial activity forecast

Inflation was lower than expected

The employment forecast has improved

The external context is expected to improve

The panellists' view of the current environmental situation in the EU is neutral, and the trend is expected to be one of improvement in the coming months. In the case of the situation outside the EU, as in previous panels, the view is also that it is neutral and that the trend will be towards improvement in the coming months.

Interest rates on government debt are not expected to rise further

Although the upward trend started several months ago, it received a boost in recent weeks when the president of the European Central Bank said there was unanimity in the ECB's Governing Council on the need to take unconventional monetary policy measures if inflation continues to rise. level would remain. very low levels over a prolonged period of time.

The euro is overvalued

Fiscal policy should be restrictive

1 Difference in percentage points between the current month's average and that of two months earlier (or six months earlier). 1 Difference in percentage points between the current month's average and that of two months earlier (or six months earlier).

KEY FACTS

Annual percentage change Figure 2.4.- Gross value, structure divided by sectors Percentage of value added in base prices. Annual percentage change Figure 4.4.- Functional income distribution Share of GDP, 4-quarter moving average Figure 4.2.- National income, consumption.

KEY FACTS: 50 FINANCIAL SYSTEM INDICATORS

Highlights

Lending to the private sector percentage change for the sum of banks, savings banks and credit unions 29. Percentage change of debt securities on the asset side for the sum of banks, savings banks and credit unions 31.

Spain´s debt dynamics and impact on the banking sector