The market is also one of the most innovative, especially in fast-growing applications such as mobile payments. One of the clearest indicators of the rise of mobile in Africa is the changing investment pattern in communications infrastructure and services. For example, in November 2011, the Nigerian Communications Commission (NCC) – which regulates Africa's largest communications market – shrugged off the introduction of unified industry regulation in the West African region.

This alone makes Africa one of the fastest growing communications markets in the world, as well as one of the most exciting. PwC acknowledges that some of the information used in the following country profiles is obtained with permission from Business Monitor International (BMI).

Southern Africa

In response, Telkom launched its own mobile W-CDMA network, 8ta, with coverage initially in the country's metropolitan areas. Many of the outstanding liberalization targets incorporated in the Court of Auditors are under consideration. Based on the results of the updated model from 2010, BTA defines and manages the new price development on the telecommunications market.

Africa Central

These operators have contributed to the transformation of the Nigerian telecommunications market in various segments including fiber and satellite backbone provision, voice, data and internet services. Nigeria's second national carrier, Globacom, has been the first to capitalize on the opportunity created by the payment system by partnering with Afri-pay Limited, a subsidiary of United Bank for Africa (UBA). The Kenyan mobile market is served by four operators – Safaricom, Airtel (formerly Zain), Orange (Telkom Kenya) and Yu, a subsidiary of the Indian-based group Essar.

The legislation was preceded in 1997 by the development of a telecoms policy framework in the form of the Postal and Telecommunications Sector Policy Statement (amended in 2006). In terms of the law, the regulator is an independent body with funding derived from licensing and spectrum fees. Uganda's information and communication technology market is considered one of the most liberalized and open in Africa.

The main objective of the guideline is to promote a fair, efficient and competitive market in the telecommunications sector. Ghana Telecom was incorporated in 1974, with the government retaining 100% ownership of the incumbent network operator. Mobile phone operator Celtel International, part of the Zain Group, acquired 75% of the operator from the Government of Ghana in late 2007, and the company was renamed Zain in August 2008.

The legislation was the result of policy directions contained in the 1995 Telecommunications Development Policy.

Francophone Africa

The Government of Ghana remains a shareholder in the company with a 25% stake through Ghana National Petroleum. Ghana's telecommunications regulator has indicated that it will not issue new licenses in the near future. In the future, it may be necessary to merge the ATCI and the CTCI into one regulatory entity to avoid the conflict of jurisdiction that regularly occurs between these two regulatory bodies and to make the function of regulating the telecommunications sector smoother.

The ATCI is reviewing its licensing framework to introduce more competition, particularly in the services tier of the market, and to review spectrum allocation. Camtel recently obtained a mobile license, albeit controversially, and is in the process of rolling out a mobile service based on the CDMA platform. Third generation mobile services have still not been introduced in the country apart from Camtel EV-DO fixed wireless service.

The regulator has shown that it can effectively intervene in the country by lowering interconnection rates between mobile and fixed operators, resulting in an overall rate reduction of around 20%. At a critical time, operators in emerging markets, especially Africa, are facing network performance issues. Voice remains the killer application in these markets, but as 3G networks become widely deployed in emerging markets, the next wave of growth will come from data usage across a range of devices such as smartphones and tablets.

Rolling out another technology (3G or even 4G) after the long 2G phase would have disastrous results – often manifested as inefficiently implemented capex, network quality issues and general delays in the rollout of the new network.

Programme in action

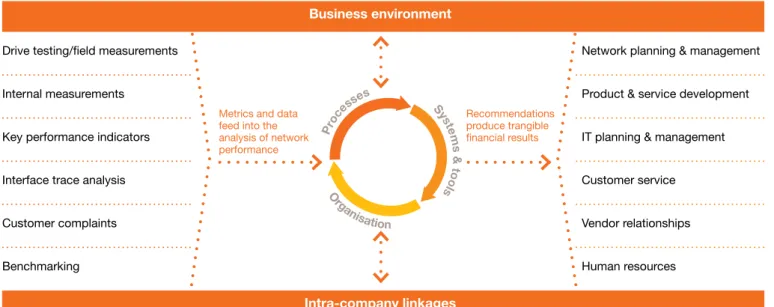

Often (and highly recommended), this assessment extends far beyond the scope of the technology organization. The organizational portion of the assessment lists challenges in the command and control structure, as well as information flow and decision-making through that structure. This part of the assessment identifies overages and gaps in the tool portfolio, as well as the consistency of the tools for effective network operations.

The purpose of this step is to build a profit-and-loss picture of the technology organization. In most cases, critical parts of the technology organization can grow to the next level by encouraging investment. What operational, organizational and cost improvements could still be made, and what the potential opportunities are for each.

Mobile operators and banks in Africa are focusing on a huge and fast-growing opportunity – the large population of unbanked people in areas where physical banking infrastructures often do not exist, but who need access to financial services. The two terms are often mixed up, but mobile banking is the broader of the two terms. In contrast, mobile payments – the focus of this article – thrive where users are 'new to banking' (not 'new to mobile banking').

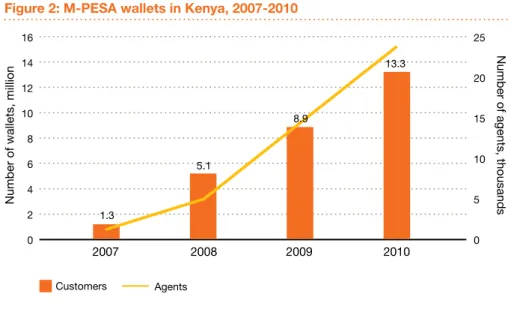

We will also identify some of the problems that operators and banks face when trying to take advantage of the mobile payment opportunity. The service now has more than 13 million users – more than 30% of the total population (see Figure 2). So it's no surprise that 36% of CMOs are planning fundamental strategic changes in the next 12 months, compared to 13% of the rest of the survey population (see Figure 3).

Michael Tsamaz

Chairman and Chief Executive Officer OTE Group

In addition to changing their approach to investment and risk, communications executives say they will likely continue to cut costs. Of course, outsourcing may be motivated by the need to reduce costs, but it is also a component of the major organizational changes that two-fifths of communications CEOs expect to make in 2012. These strategic priorities are reflected in the 'wish list' of activities. which communications CEOs most want to spend more time on.

While CEOs in many sectors prioritize leadership development and the talent pool, communications CEOs are more interested in meeting customers. Communications CEOs are more positive about the changing dynamics of the global economy than their peers in other sectors, as befits the global nature of their industry. And while most CEOs with overseas expansion plans are focusing on China, CMOs prefer Brazil: 26% see it as a key growth market in the next 12 months (vs. 15%).

That said, communications CEOs expect to receive more information about their employees than CEOs in other sectors—and they're often more satisfied with the quality of information they receive. Communications executives also place much greater weight on measures such as staff productivity (62% vs. 50%) and labor costs (57% vs. 41%). Almost three times as many communications CEOs have significantly reduced their company's headcount—that is, by more than 8%—in the past 12 months.

Communications executives want to make sure they're armed with all the facts when faced with tough decisions about who to keep and who to let go.

Wim Vanhelleputte MTN Côte d’Ivoire

Today, if you are in Côte d'Ivoire and you get an internet connection, it can be even better than the internet connection you might have in France or Switzerland or other parts of the world. Taiwan, Singapore and South Korea are all good examples of the benefits of investing in this infrastructure. What are your views on the future development of the communications market in Côte d'Ivoire.

Many of the applications that are already being used in other parts of the world will follow here because, after all, we are only in one big village right now. Communications Review: As CEO for MTN Côte d'Ivoire, how are you making the most of MTN's network of companies on the continent? Iran and South Africa are more advanced, more developed markets than most of the other 19 countries, so products and services, new promotions and the like are all shared with us; we don't have to reinvent anything because we are part of a group.

The individual operator does not have an overview of what is really happening in the rest of the world or in similar markets or more advanced markets, and this is where MTN with 21 countries makes the difference. The differences are in the details, but we all do similar things in many of the same markets. For example, if we tell the guys from MTN Benin that we're going to run their shift from Côte d'Ivoire, I don't think they'll have a party – but they'll understand and maybe say, okay, maybe I can get the position in Abidjan to work there and do part of the job.

Photos will also be a problem because the faces of people from Ghana are so different from those in the Ivory Coast that anyone looking at the photos will immediately recognize the Ghanaians, not the Ivorians.

Karel Pienaar MTN South Africa

He is a registered professional engineer and a member of the Institute of Electrical and Electronic Engineers. The participation of telcos in the financial services industry could lead to a zero transaction fee environment due to differences in the telco's respective business and cost models compared to the banks. None of the mobile banking services offered currently effectively meet the real needs of segmented customers, such as simplicity, cost and accessibility.

This is about to change, as meeting these needs is directly related to a telco's distribution footprint and mobile penetration rates. Pienaar: Before responding to the role of the equipment manufacturer per se, let's first consider the ICT ecosystem. I believe that given the scale of the current telecommunications operators in South Africa and the scale required to establish a successful telecommunications business, other ICT players should not focus on becoming telecommunications operators themselves.

This means that the telecommunications company of the future will consist of a single network with flexible centralized services. Pienaar: The sharing of networks and service platforms is very important in the business model of the future. With the introduction of the latest optical technologies, we are moving into an era of unlimited capabilities.

To obtain PDF files or hard copies of the publications, please visit the websites below.