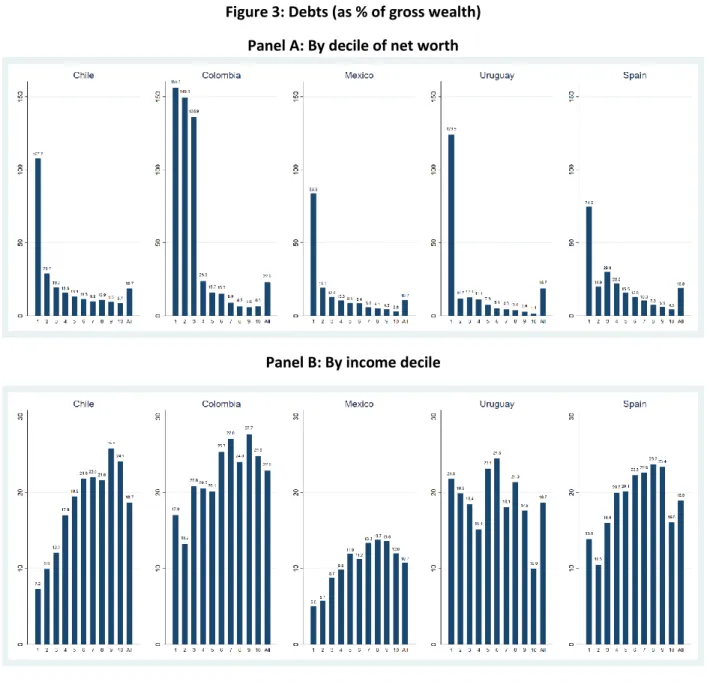

In contrast, the ratio of net worth to income is significantly lower in the Latin American countries, ranging from 5.1 in Mexico, to 4.4 in Uruguay and Colombia, and 3.5 in Chile. Universidad ORT Uruguay | 8 Surprisingly, the debt ratio for the rest of the wealth distribution is remarkably stable (with Latin America at lower values than Spain). This is likely a reflection of limitations in the development of the country's financial system and capital markets.

Households in the lowest deciles hold most of their wealth in financial assets, while the proportion of financial assets decreases until the 6th to 7th deciles, and then increases at the top right of the distribution. As seen in the following charts, financial assets differ for the poor (who hold mostly liquid and safer assets, such as cash) and the rich (who hold riskier and more long-term assets). As already discussed, most financial assets in Chile are held in the form of pension rights.

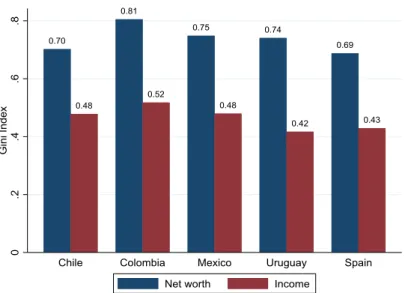

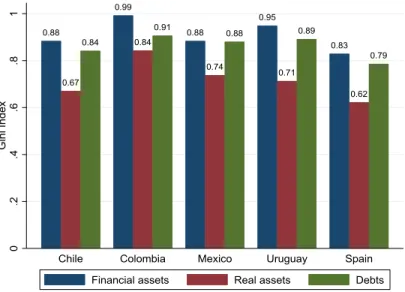

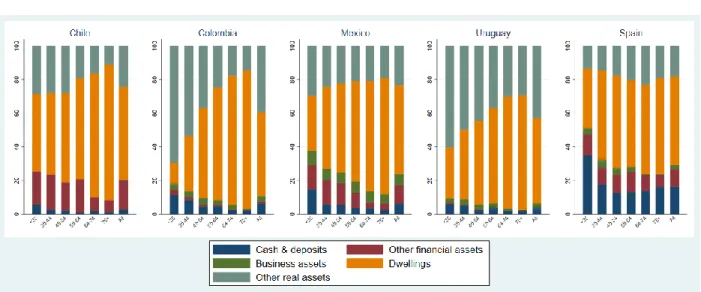

The ratio of Gini's wealth to Gini's income is between 1.56 and 1.60 for Colombia, Mexico and Spain. Financial assets are the component of wealth that is least equally distributed in the five countries, but especially in Uruguay and Colombia. The share of residential assets increases with age for the four Latin American countries.

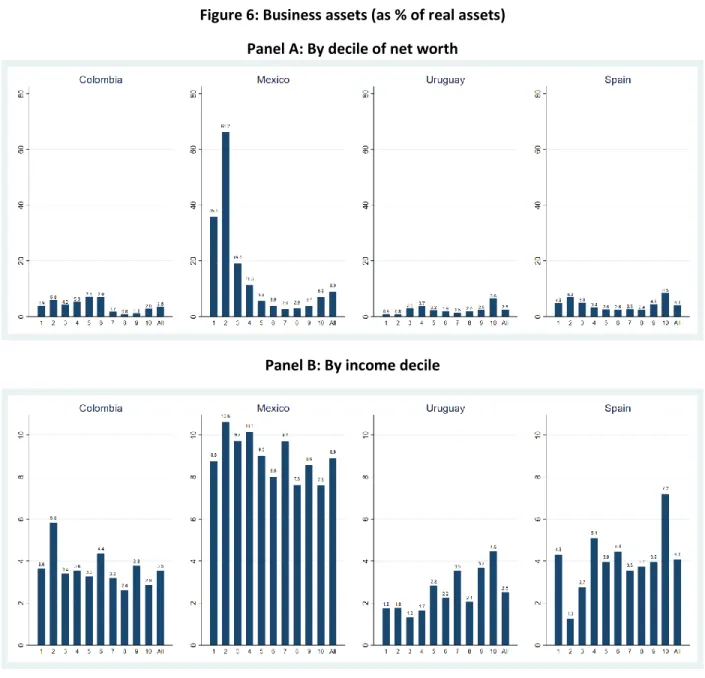

The ratio of gross wealth in business assets is highest for those in the lowest education group in Mexico. This represents between 25% and 39% of the average value of the net worth-to-income ratio. Universidad ORT Uruguay | 24 Similarly, Table 2 reports the regression of the debt-to-income ratio on observable household characteristics.

Intergenerational effects

High level of education is a dummy that takes the value of one if the household head has completed at least some tertiary education. Universidad ORT Uruguay | 27 Inheritances are not only related to debts, but also to net worth. While net worth represents 7 years of annual income among families who inherited their main property in Chile, Mexico and Uruguay, it represents only 3.4 years in Chile, 4 years in Uruguay and 4.8 years in Mexico among families who did not inherit their main property .

That is, for most of the relevant empirical range, the probability of receiving an inheritance increases with age. Given the probabilities of being inherited (Chile 4%, Mexico 11%, Uruguay 12% and Spain 10%), this implies an elasticity in the probability of inheritance with respect to income in the range of approximately one for Chile, Mexico and Spain and a much lower 0.2 for Uruguay. Universidad ORT Uruguay | 28 argued that these coefficients are the result of reverse causality: individuals who inherited their homes do not need to generate the same amount of labor income to cover their family budgets.

Note: Income refers to the logarithm of household income; all other variables are defined for household heads. Secondary education level is a dummy that takes the value of one if the head of the household has completed a secondary or technical education. One of the most commonly used strategies to study intergenerational mobility is to measure the impact of parent education on children (Behrman et al. 1999).

A ratio equal to 1 means that the head of the household has achieved the same level of education as her parents. Someone with the same level of education as their parents has not benefited from the overall social improvement in education. There are no substantial differences in the ratio with respect to the mother or the father, or even the maximum between the two.

From now on, we analyze intergenerational mobility using the maximum, but our results are robust to alternative measures. We consider three groups of households: those in which education has not improved relative to the average (ratio below 1.15, which corresponds to the first quartile), those in which the number of years of schooling has increased compared to parents, but consistent with other households. population (ratio between 1.15 and 2, which corresponds to the second and third quartiles) and those with an above-average increase in the number of years of schooling (ratio above 2). Without making claims about causality, the results show that intergenerational advancement in education is associated with greater wealth, a greater ratio of net worth to income, a greater likelihood of inheritance, a greater share of financial assets, and a lower share of real assets and debt.

Final observations

Universidad ORT Uruguay | 31 We also examine the relationship between assets and debt with respect to household characteristics. We find an increasing correlation between the wealth-to-income ratio with age and education in all countries. For example, the increase in net worth relative to income between the lower level of education and the intermediate level is between 0.9 and 3.

The difference between those with higher education and those with less is even greater. In Latin American countries, we find an inverse U-shaped relationship between the debt-to-income ratio and age. Older age is associated with a higher debt-to-income ratio up to a point where the ratio begins to decline.

The highest value is reached in Chile at the age of 37, in Colombia at the age of 58, and in Mexico and Uruguay at the age of 50. We find that more educated households tend to have higher debt-to-income ratios, likely reflecting difficulties in accessing credit markets among the less educated. The proportion of households that inherited their main property is 12% in Uruguay, 11% in Mexico and only 4% in Chile, compared to 10% in Spain.

As expected, the share of gross assets in housing in the four countries for which inheritance data is available increases with inheritance, while the share of assets in cash and deposits falls, as does household indebtedness. We also find, as in the case of Spain, that net worth relative to income is significantly higher among households that have received an inheritance in the three Latin American countries for which data are available. Only in Uruguay are we able to study the relationship between intergenerational mobility, measured by education, and wealth.

Without claims of causality, we show that intergenerational educational progress in that nation is associated with greater wealth, greater net worth-to-income ratios, greater probabilities of inheritance, greater shares of financial assets, and lower shares of real assets and debt. The raw data used in the paper are publicly available from national institutes mentioned in the Data section of the paper. Upon request, the authors can provide the codes that produce the figures and tables reported here.

DEPARTAMENTO ADMINISTRATIVO NACIONAL DE ESTADÍSTICA DE COLOMBIA– DANE (2019)