With regard to the cost-benefit ratio, the majority of companies indicate that the costs outweigh the benefits. In addition to the tour of the building, personal contact with the detainees was also on the programme.

RELEvANCE

Referring to the study of kPMG in 2010, they already assessed white-collar crime as a serious danger and predicted a further increasing trend (cf. kPMG, 2010, p. 6). The current study from 2012 shows that the number of accounting information and annual account falsifications has been reduced to three per cent. (cf. kPMG, 2012, p. 11).

This also includes the question of the form of control and the type of sanctions, as both are important for the effectiveness of legislative measures. In addition, an investigation is underway into how companies listed on DAx, MDAx, Tec-DAx and SDAx rate the effectiveness of the government's catalog of measures against its targets.

ThE STUDY’S STRUCTURE

To concretely grasp the offense of balance manipulation, the following chapters will discuss it in the context of white-collar crime and its terminology.

ACCoUNTING IRREGULARITIES IN ThE CoNTExT oF

The Penal Code for Trade 1954, the German Foreign Trade and Payments Act, the Goods Exchange Laws, as well as the Financial Monopoly, Tax and Customs Laws, including with regard to the penal provisions that may be applied under other laws. The Broadcasting Act (AÜG) and the third book of the Social Code as well as the Act to combat clandestine labour.

FACTUAL FINDINGS oF ACCoUNTING FRAUD

According to the German accounting principles of the German Commercial Code (hGB), Commerzbank suffered a loss of 3.6 billion euros. The result of the loss under the accounting principles of the German Commercial Code (hGB) meant that it did not have to pay interest on the state's €1.9 billion share.

ExPLANAToRY MoDELS FoR ThE ACT oF

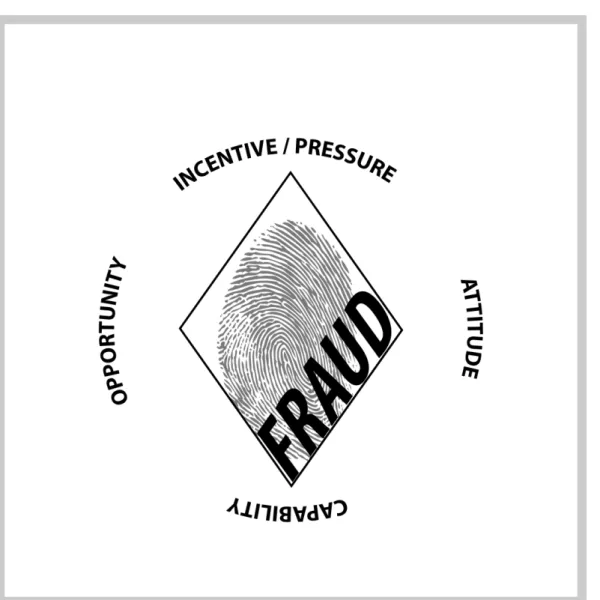

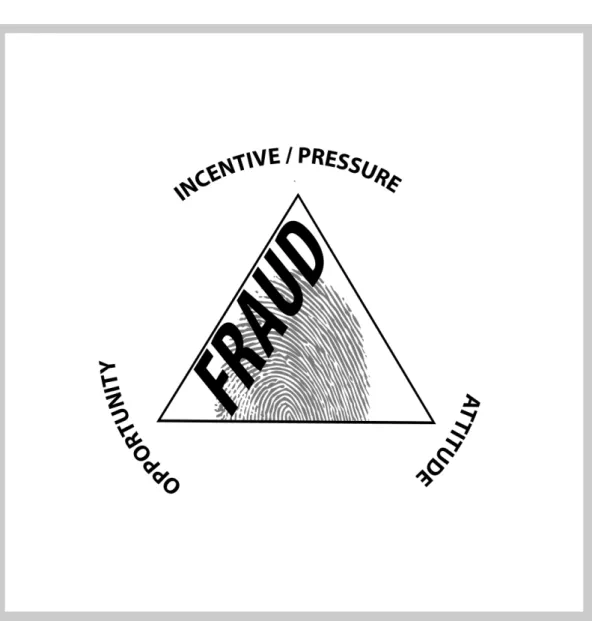

FRAUD TRIANGLE / FRAUD DIAMoND

The IDW also notes that the inner justification is dependent on the attitude, the character or the moral concept of the person acting (cf. The aspect of inner justification has a subjective component but the social context of the company plays a decisive role in relation to the personal justification for the undertaking of a fraudulent act.

APPRoAChES To FURThER DEvELoPMENTS

- ThE LEIPzIGER PRoGRESSIoN MoDEL oF WhITE-CoLLAR CRIME

- ThE oFFENDERS MoTIvES FoR CoMMITTING

- PRoFILES oF WhITE-CoLLAR CRIMINALS

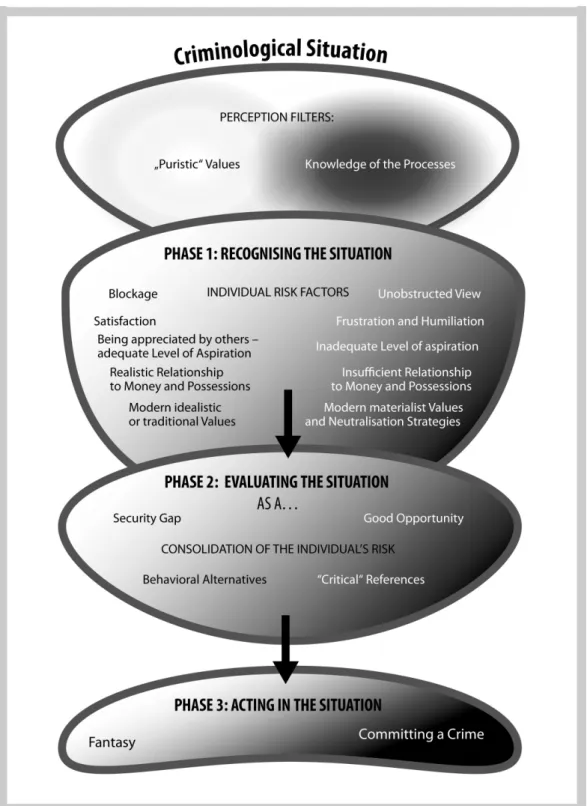

As such, the Leipziger Progression Model analyzes the procedural nature of white-collar crime and the driving factors that arise throughout the process (cf. There is insufficient scientifically based practical knowledge about the person the white-collar criminal is.

LookING AT ThE ACCoUNTING FRAUDSTER

Motives for a better presentation of the company's financial statements can be, for example, personal enrichment plans on behalf of management. In subsequent years, the company's results will implicitly appear better than they actually are.

ThE PRINCIPLE oF ShAREhoLDER vALUE

11 This includes three of the four largest energy suppliers in Germany (the fourth company is vattenfall which is headquartered in Sweden). These four companies own the majority of the electricity market in Germany and own the majority of electricity networks.

RESULTS oF ACCoUNTING IRREGULARITIES

IMPLICATIoNS FoR CoMPANIES

The authors of the study also point to the significant administrative costs caused by white-collar crime. Fighting white-collar crime and prosecuting cases cost a lot of time and money.

IMPLICATIoNS FoR CoMPANY oWNERS, INvESToRS AND ShAREhoLDERS 62

Personal guilt and culpability are presupposed in accordance with § 331 of the German Commercial Code (hGB) intentional conduct that must be proven. It found the fact of immoral intent fulfilled in accordance with § 826 of the German Civil Code (BGB) (cf.

IMPLICATIoNS FoR SoCIETY: STATE, CoNSUMER, ECoNoMY

In February 2003, the German government issued the final version of the catalog of measures to strengthen the integrity of companies and protect investors (Maßnahmenkatalog der Bundesregierung zur Stärkung der Unternehmensintegrität und des Anlegerschutzes, 2003). For this purpose, a brief overview of the relevant codified measures will be provided in advance. Implementation of the German law on corporate integrity and the modernization of the right of avoidance (as well as possible for

PERSoNAL LIABILITY oF ExECUTIvE BoDIES

LIABILITY ToWARDS ThE CoRPoRATIoN

15 According to Seibert, the act does not increase the responsibility of the members of the supervisory board. 93 of the German Stock Corporation Act defines the liability of board members in more detail. It continues the reform process of recent years of the German Stock Corporation Act.

LIABILITY ToWARDS To ShAREhoLDERS

- INFoMATEC-DECISIoNS

- ThE CASES CoMRoAD AND EM.Tv

- ExTERNAL LIABILITY oF ThE BoARD PURSUANT To § 826 BGB

- A BILL: ThE ACT GovERNING LIABILITY FoR

- ThE GERMAN CAPITAL MARkETS MoDEL CASE ACT (kAPMUG)

- CoNCLUSIoN

The desired outcome of the model procedure is determined by the competent regional court. The validity of the German Model Capital Markets Act (kapMuG) was then extended until October 31, 2012. According to Halfmeier, this need to file a claim made the German Model Capital Markets Act (kapMuG) somewhat awkward.

GERMAN CoRPoRATE GovERNANCE

CoRPoRATE GovERNANCE

As a whole, corporate governance guidelines can be seen as a kind of principles of society. Many fundamental concepts of German corporate governance date back to the 1990s. This is one of the reasons that led to the development of the German Corporate Governance Code.

ThE GERMAN CoRPoRATE GovERNANCE CoDE (DCGk)

The meaning and purpose of the DCGk is to make the German Corporate Governance System transparent and understandable. However, 161 of the Stock Corporation Act obliges the executive board and supervisory board of corporations listed on the capital markets to issue an annual declaration on compliance with the Corporate Governance Code (declaration of compliance)45. The auditor must not evaluate whether the company's management and monitoring systems comply with the regulations of the German Corporate Governance Code (cf.

CoNTENT AND ChANGES MADE To ThE GERMAN CoRPoRATE

A remuneration report as part of the Management Report outlines the remuneration system for Management Board members. The remuneration of the members of the Supervisory Board will be reported individually in the Notes or the Management Report, subdivided according to components. The concrete objectives of the Supervisory Board and the status of the implementation will be published in the Corporate Governance Report.

FURThER IMPoRTANT REGULATIoNS oF ThE

It must be involved in decisions of fundamental importance for the enterprise" (English version of the DCGk, 2013, Point 5.1.1.). Proposed eligible candidates for the chairman of the supervisory board will be announced to the shareholders (cf. English version of the DCGk, 2013, point 5.4.3). The supervisory board members are bound to the company's best interests (cf. English version of the DCGk, 2013, Point 5.5.1).

CoNSEqUENCES FoR EvERYDAY WoRk

Second, relevant relevant information on key corporate governance processes that go beyond legal requirements. There should be an indication of where this information can be publicly accessed. And thirdly, a description of the procedures of the management board and the supervisory board, as well as the composition and modus operandi of their committees should be part of the Corporate Governance Statement (cf. kPMG, 2009).

FURThER DEvELoPMENT oF ACCoUNTING STANDARDS AND ITS

ThE (GERMAN) ACCoUNTING REFoRM ACT

- ExERCISING ThE DECISIoN RIGhTS FoR ThE SEPARATE

- ExTENDED DETAIL oF NoTES

- ExTENDED MANAGEMENT REPoRT

- ExERCISING ThE DECISIoN RIGhTS FoR ThE GRoUP ACCoUNTS

- ABoLITIoN oF ThE CoNSoLIDATIoN PRohIBITIoN PURSUANT

- ExTENSIoN oF ThE ITEMS WIThIN ThE CoNSoLIDATED

- EvALUATIoN

An IAS separate financial statement auditor certificate must be published instead of the German Commercial Code (hGB) separate financial statement auditor certificate. Nevertheless, some of the German Commercial Code (hGB) guidelines, especially those regarding the management report (§ 315 hGB), must also be observed. Specific positions of the annual financial statement in terms of IAS/IFRS must, as a minimum requirement, be present in the statement of the financial position within the accounts (cf. IAS 1.54).

ThE GERMAN ACT To MoDERNIzE ACCoUNTING LAW (BILMoG)

Financial Statements: A fundamental part of the German Accounting Modernization Act is the modernization of the recognition and measurement facility for all traders. The introduction of the German Bookkeeping Modernization Act (BilMoG) has significantly changed German Accounting Law. The introduction of the German Accounting Modernization Act has led to changes in requirements for internal processes and documentation.

STRENGThENING ThE RoLE oF ThE INDEPENDENT AUDIToR

ThE PRINCIPLE oF INDEPENDENCE

The original task of an independent audit is to provide a reliable opinion on the formal and tangible correctness of the published financial statements. In order to regain public confidence in the independence of the independent auditor, it seems necessary to go back to the original, actual function of the independent auditor. Pursuant to Section 43(1) of the Law on public accountants, the accountant must in any event exercise his profession independently, conscientiously, discreetly and autonomously.

INTERNATIoNAL AUDITING STANDARD

The uniform presentation of the ISA as a law directly applicable to all member states of the European Union would have been preferable as it would have helped to avoid balance sheet manipulations. Auditors examining companies in different EU member states would know exactly which auditing standards and regulations apply as they are the same across the EU. Because of the uniform EU regulations, it would also be easier to ensure that companies with subsidiaries in different EU member states follow the same regulation.

ThE DECLARATIoN oF CoMPLIANCE AND

It is also not subject to examination proceedings if the company makes use of its right of choice to include it in its Management Report and not simply publish it on the company's homepage. Based on this procedure, it is possible to have a Management Report consisting of parts that are subject to examination and parts that are exempt from examination proceedings. To avoid misunderstandings, the independent auditor must take note of the fact that the Corporate Governance Statement was not part of the independent audit proceedings in the introductory part of the audit certificate (cf.

ThE RESPoNSIBILITIES oF ThE GRoUP AUDIToR

SEPARATIoN oF INDEPENDENT AUDITS AND CoNSULTATIoN

The costs of the audit services that cannot be covered are supported by other services (cf. A strict opponent of the request to separate audit and consultation is Ring. Ring sees as the logical consequence that the effort in the audit – with corresponding consequences for the quality of the independent audit – informs itself of the fees paid.

APPoINTING ThE ExTERNAL AUDIToR

In accordance with the 2nd and 3rd sentences of the German Stock Corporation Act, the auditor reports to the plenary supervisory board or the audit committee at the last audit meeting of the supervisory board. With the German Accounting Act Modernization (BilMoG), the supervisory obligations of the auditor were expanded and the reporting duties were newly regulated. In general, it is necessary to increase the transparency of the relationship between the supervisory board and the auditor (cf.

ExTERNAL vERSUS INTERNAL AUDIToR RoTATIoN

The request to rotate the external auditor was rejected by the legislator due to the risk of loss of audit quality after the change of audit firm. Some opponents of the external rotation system point out that auditors need several years to work their way into a new firm. New employees could quickly learn from the management of the audit company and colleagues who have already participated in the audit, and therefore use the same processes and methods as their predecessors (cf.

PUBLIC DISCLoSURE oF FEES

They came to the following findings: The first category of "independent audit services" received 66.3 percent of the average share of total fees. The second category “other confirmation services” was 12.2 percent of the average part of the total fees. The third category 'tax advisory services' amounted to only 7.6 percent of the average fee.

ExTENSIoN oF LIABILITY

To reduce this problem and to make the independent auditor more accountable, Baums and Fischer propose amendments to §§ 37c through 37g of the Securities Trading Act. In the fourth paragraph of Article 37c of the Securities Trading Act, it would then be stated that the liability of a natural person who acted out of gross negligence for the payment of damages would be limited to one million euros (cf. It is also difficult to calculate the actual correct and proportionate the correct share of the damage caused in relation to the liability of the management and the supervisory board for the liability of the auditor for the damage to the investor.

ChANGES To ThE PRoFESSIoNAL SUPERvISIoN

According to Nonnenbacher, the application of the various proposals regarding the extension of an accountant's legal liability can be measured by whether the proposed changes can contribute to an improved quality of the independent audit and to strengthening confidence in the audited entity. annual accounts. Ultimately, the board and supervisory board are the leader and head of the company. The Chamber of Public Accountants (WPk) is now also closely monitored for its supervisory function by a new committee that is independent of the profession: under supervision 96 Pursuant to § 68 paragraph 1 of the Public Accountants Act (WPo ) professional legal proceedings can be instituted at the audit matters department of the regional court in Berlin and the following sanctions can be imposed on an auditor: In case of a warning, the court accepts the committed dereliction of duty but - prosecutes a strong warning for repetition.

CoNCLUSIoN

MoNIToRING ThE LEGALITY oF SPECIFIC CoMPANY

ThE GERMAN FINANCIAL REPoRTING ENFoRCEMENT PANEL

ThE FEDERAL FINANCIAL SUPERvISoRY AUThoRITY (BAFIN)

AN EvALUATIoN oF ThE GERMAN ENFoRCEMENT SYSTEM

ELECTRoNIC PUBLICATIoN oF A CoMPANY’S ACCoUNTS

ENhANCING ThE PRoTECTIoN oF INvESToRS

INSIDER TRADING LEGISLATIoN PURSUANT To ThE

AD-hoC PUBLIC RELEASES ACCoRDING To ThE

TRANSACTIoN REPoRTING REqUIREMENTS FoR MEMBERS

ThE PRohIBITIoN oF RATE AND MARkET PRICE MANIPULATIoN

PoINT NINE AND TEN oF ThE GovERNMENT’S CATALoGUE oF MEASURES 249

METhoDoLoGY APPLIED To ThE EMPIRICAL STUDY

ASSESSMENT oF ThE REGULATIoNS BY ThE CoMPANIES PoLLED

EvALUATIoN oF ThE USEFULNESS oF PoSSIBLE

ThE PoLLED CoMPANIES’ EvALUATIoN oF ThE

ASSESSING ThE oUTCoMES