The wave of investment in the 1990s was part of the general trend towards economic liberalization and the removal of barriers to the inflow of foreign capital, modernization of mining concession regulations, safer mining rights and technological changes that have taken place in recent decades. The more favorable climate for foreign investment and the removal of barriers to entry into the mining sector heralded a new phase in the 1990s in terms of attracting foreign capital.

Variations in foreign capital inflows

In the early 1990s, debt/equity swaps were suspended, except in Argentina, and replaced by privatization initiatives. The crisis of the eighties did not leave much room for maneuver in the management of national economic policies.

New Environment for foreign investment

Most countries in the region made substantial changes to their mining laws in the 1990s, with the exception of Chile. In the case of nuclear minerals (uranium and thorium), the state has the right of first refusal to acquire them on market terms (Argentina and Chile). In Brazil, references to mining can be found in the resolutions of the environmental authority (the obligation to carry out environmental impact assessments and mitigation plans, the approval of which is a condition for the granting of mining rights).

Of the analyzed countries in the region, Argentina, Brazil, Bolivia and Venezuela all have royalty payments. As discussed later, copper and gold have been the most favored metals in investment decisions in the 1990s. It is not the purpose of this paper to review the macroeconomic changes that have occurred in the countries of the region.

Furthermore, four of the 10 countries with the largest research budgets in the world are Latin America, namely Chile (4th), Peru (6th), Brazil (8th) and Argentina (9th).

Non discrimination against foreign capital

Registration and Authorization

For the purpose of capital repatriation or transfer of earnings, the investment must be registered with Republikkens Bank. In Venezuela, a similar system exists and the investment must be registered within 60 days with the Office of the Superintendent of Foreign Investment (SIEX).

Remittances abroad

Companies that receive foreign capital inflows must provide information on their capital movements to the DNP, the Bank of the Republic and the Office of the Superintendent of Foreign Exchange. In Brazil, the Central Bank has the right to prohibit repatriation of capital for a limited time and to limit remittances of earnings to an annual equivalent of 10% of the capital investment and registered reinvested earnings.

Operating requirements

In the case of mining and oil activities, remittances may be conditional upon the fulfillment of special conditions from the concession contract. In this case, the earnings, including all those accumulated in the first four years, can be transferred abroad from the fifth year onwards, provided that the annual transfer does not exceed 25%.

Treatment in case of expropriation

In Chile, capital can be remitted one year after investment, while amounts invested to purchase and use debentures and debt/equity swaps can only be remitted after ten years. This must be equivalent to the established commercial value, although this value may be challenged before the appropriate judicial authority.

International arbitration

The Constitution of Mexico states that expropriations can take place on the basis of the public interest and with guaranteed payment of damages within one year. In Peru, the current constitution limits expropriation to cases of public interest or national security.

Investment protection agreements

Changes in mining legislation

This is the most common system in the region (Argentina, Bolivia, Brazil, Costa Rica, Cuba, Ecuador, Guatemala, Honduras, Mexico, Peru, Uruguay and Venezuela), although it has been criticized for being too flexible in terms of discretion. powers it grants to the mining authority. The costs of obtaining a concession are tax deductible, as are the costs incurred for the exploration, development and preparation of the mining operation. Most countries in the region have introduced reforms to simplify tax procedures and eliminate or minimize specific or earmarked taxes.

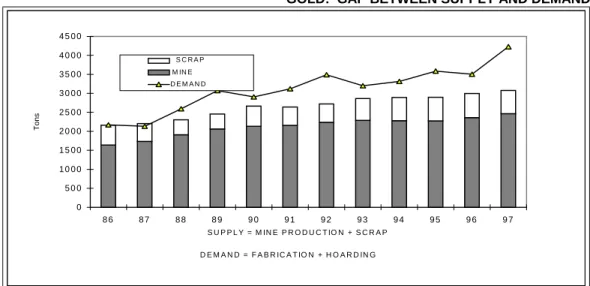

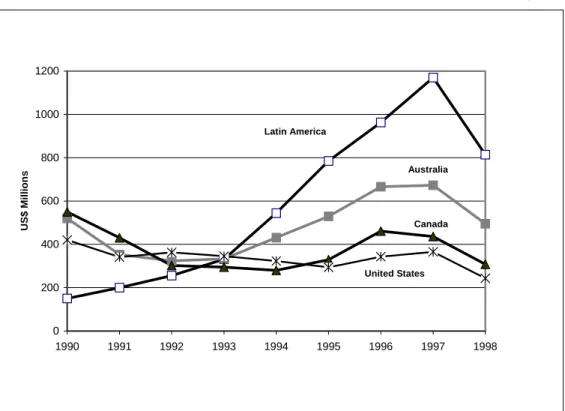

There are a variety of mining operators in the region occupying very different positions on the value chain. In the early 1990s, exploration budgets allocated to the countries of the region amounted to less than US$200 million per year and were basically concentrated in Chile. As with exploration expenditure, there is also no information on new investment projects in the region during the 1990s.

Of the 116 projects in the sample, 53% relate to investment initiatives in the portfolio and the rest to projects that have been suspended or postponed.

State of domain and public interest

Concessionary regimes

The discretionary power of the relevant authority tends to be limited to the strict minimum. In Chile, the judiciary has jurisdiction and refers to the judge of the civil court where the concession was registered.

Environmental protection

The judicial system in Bolivia provides for chambers for mining issues within the higher courts. The Mining Code in Venezuela does not establish specific rules on dispute resolution, but refers cases to the judiciary.

Fiscal regime

Royalties are also paid (in cash or in kind) on a percentage of the gross output that is mined, of which 70% is paid to the municipalities and 30% is credited to the Mining Development Funds. In Cuba, there is a mandatory surface rent that varies according to the different phases of prospecting, exploration and extraction.

Investment incentives

Trade and taxation regimes in mining compared

Trade liberalization

In Brazil, the process of foreign trade liberalization began in 1985 with the gradual elimination of quantitative controls and the rationalization of administrative procedures; this was followed by successive tariff reductions between 1987 and 1993, which brought the average rate down from over 50% to 14%. During this period, the average customs duty rate decreased from 44% to 12%, where it remains today. At the time of writing, however, the average tariff in Venezuela has risen again to 12%.

Characteristics of tax regimes in selected countries of

Dividend payments to foreign shareholders and transfers abroad are tax-free; but there is a tax on interest payments currently set at 15%, although in some cases the rate is lower under bilateral trade agreements. Finally, the mining industry pays royalties on the value of the metal content, but only when this tax exceeds the tax on profits. Ad-valorem royalty payments vary between 4% and 7% depending on the mineral in question, while sales tax, which is non-refundable, is levied at an average rate of 15.5%, in a range of 5%-20%.

Incidence of taxation on mining operations

Royalties paid abroad are freely refundable but are subject to a tax rate of 30%, while the 18% general sales tax (GST) is refundable in the case of mining. In the first case, a fixed nominal amount is charged on a predetermined unit of measure. By alleviating the effects of the project development stages and the negative effect that can arise from low prices in the mining phase, the State contributes to the amortization of losses by accepting lower income.

Impact of taxation on investment decisions

Factors underlying the performance of investments

What makes mining competitive

Investors in the mining industry usually pay attention to the difference between costs and international benchmark prices, as this reflects the position they are likely to achieve in the global market. Companies that can increase this margin and influence production costs will be less sensitive to market fluctuations. Investments in mining are long-term ventures that mature slowly and are influenced by the construction of new (greenfield) facilities; with expected supply and demand over a long period of time (brownfield) and with the expansion and success of old (redfield) activities.

Factors arising from international market conditions

However, the buoyancy of the United States economy during the 1990s generated higher average copper consumption in the developed world in 1990–1997. Average lead consumption in the United States grew at a rate of 4.46%, while the global average was 1.20%. Over the same period, Latin America also increased its share of the production of most items in the refined product category, except for lead and tin.

Technological changes

In 1998, exploration budgets in the region were cut by more than US$300 million from the previous year's level. In a sample of 93 mining companies conducting exploration in the region in 1998 (there were 124 in 1997), with an annual budget allocated for this purpose in the order of US$. The most important gold mining projects of the 1990s invested US$865 million in the first eight years of the decade, including la Coipa (Placer Dome–TVX) amounting to US$340 million;.

1) 100% in the year in which the costs are incurred, or in the first year of production. 1) 100% deducted in the year in which the costs are incurred or in the first year of production.

Internationalization of environmental issues

The global strategies of mining companies

The trend in the 1990s, particularly in the case of copper, was for countries in the region to export not only low-processing products to supply refineries abroad, but also refined products for industrial consumer markets. The most attractive margins between costs and international prices are not necessarily always in the most processed market segments. Mining companies sign long-term marketing agreements that are renegotiated at a contractually agreed frequency and usually leave a small portion of the mineral available for a short period of time.

Political stability and legal security

This is what distinguishes public-sector enterprises that are specifically created to exploit national mineral wealth and that have limited access to foreign resources. For many government authorities, it would not make sense for a public sector company to close operations in its country of origin and move elsewhere to improve its operating margins.

Country–risk conditions: macroeconomic health and policies that favour mining

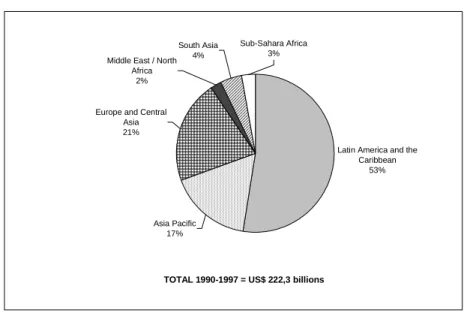

Mining investment in the 1990s

Exploration choices depend on a variety of factors, but for the purposes of this study it is interesting to highlight the correlation between technological change and the availability of resources in the countries of the region. Among new projects in Peru, Antamina has the best chances of execution in the short term. In the same time period, exploration budgets worldwide more than doubled from about US$1.8 billion to US$4.03 billion per year.

Total investment accumulated in the period 1992–1997 is put at US$ 1.788 billion, of which 79% corresponds to the production phase and the rest to mining exploration. L - SERIES Resursos naturales e infraestructureN° 1 . in Latin America in the late 1990s withheld .. equipment and services used for the production of exportable goods, including mining products.

Investment in exploration

Mining investment executed

Bajo de la Alumbrera (gold-copper; $1.1 billion investment); Salar del Hombre Muerto (lithium; US$110 million); and Cerro Vanguardia (gold; US$197 million), which is scheduled to come on stream in 1998. In addition, an expansion of Escondida (oxide plants) is planned with an investment of US$470 million. US$. The company also brought the copper cathode project at the ESDE plant into production in 1995 with an investment of US$56 million.

Mining investment projection

Tariffs paid in the pre-production phase benefit from payment divided into 9 semi-annual quotas with 6.5% interest per annum. Possibility of refund for inputs, raw materials, intermediate products, pieces and parts used in the production of exported goods. Alternative means for private participation in the provision of water services, Terence Lee and Andrei Jouravlev (LC/L.1024), Mayo de 1997 www.

The main mining taxes

Deductions from the tax base