PRODUCTION NETWORKS AND EU ENLARGEMENT:

IS THERE ROOM FOR EVERYONE IN THE AUTOMOTIVE INDUSTRY?

LETICIA BLÁZQUEZ CARMEN DÍAZ-MORA

ROSARIO GANDOY

FUNDACIÓN DE LAS CAJAS DE AHORROS DOCUMENTO DE TRABAJO

Nº 612/2011

De conformidad con la base quinta de la convocatoria del Programa de Estímulo a la Investigación, este trabajo ha sido sometido a eva- luación externa anónima de especialistas cualificados a fin de con- trastar su nivel técnico.

ISSN: 1988-8767

La serie DOCUMENTOS DE TRABAJO incluye avances y resultados de investigaciones dentro de los pro- gramas de la Fundación de las Cajas de Ahorros.

Las opiniones son responsabilidad de los autores.

PRODUCTION NETWORKS AND EU ENLARGEMENT: IS THERE ROOM FOR EVERYONE IN THE AUTOMOTIVE INDUSTRY?

Leticia Blázquez*

Carmen Díaz-Mora*

Rosario Gandoy*

Abstract:

The aim of this paper is to analyse the changes that have taken place in European production networks since the mid-nineties, when, simultaneously, a new impetus to the EU process and its enlargement occurred. Due to its characteristics, the automotive industry is particularly suitable for our analysis. Descriptive analysis suggests that advances in the European integration process have led to a spatial extension of the networks to the East rather than to a replacement of traditional locations. This finding is supported by our econometric analysis that, estimating an extended gravity panel data model, shows that, besides EU membership and comparative advantages, variables such as good quality infrastructure, a minimum threshold of development, a headquarter effect as well as other unobserved country characteristics are key determining factors to be integrated in cross-border production networks. Moreover, these results open the door to the implementation of regional and industrial policies in order to strengthen these European production networks.

JEL Classification: F10, F14, F15, L62

Key words: International production networks, Trade in parts and components,

Enlarged European Union, Automotive Industry, Panel data gravity model.

Corresponding author: Carmen Díaz Mora, Dept. International and Spanish Economics, Econometrics and Economic History, Faculty of Juridical and Social Sciences, University of Castilla-La Mancha, 45071 Toledo, Spain. E-mail: [email protected]

* Dept. International and Spanish Economics, Econometrics and Economic History, Faculty of Juridical and Social Sciences, University of Castilla-La Mancha.

Acknowledgements: Financial support from the Castilla-La Mancha Regional Ministry of Education and Science under the project PPII10-0154-9251 (co-financed by FEDER funds) is gratefully acknowledged.

2

1. INTRODUCTION.

In recent decades, trade liberalization, advances in information technology and the reduction in transport and communication costs have favored an increasing use of strategies of international production fragmentation. This process has encouraged the formation and intensification of international production networks. The establishment and strengthening of regional trade agreements has reinforced this trend. Particularly, lower trade barriers between Members have had a marked impact on the configuration of global networks, promoting their current regional configuration. Additionally, in accordance with the classical theory of international trade, comparative advantages play a noteworthy role in their structure. Consequently, within the European Union scope, the deepening of the integration process and the accession of twelve new Member States, with cost advantages over the senior members and close proximity to major European markets, would have given an additional impetus to the geographical reorganization of production in the region.

However, there exist certain factors that favour the stability of the existing networks. The international production fragmentation decision depends largely on the costs of managing cross- border production blocks. Among them, transportation, communication and coordination costs of the fragmented production chain, i.e., the named “service link” costs (Jones and Kierzkowski, 1990), are particularly important. In general, transaction costs (Williamson, 1975) such as the costs of searching out for new business partners in new markets, bargaining and decision costs, costs of controlling and guarantying the quality and delivery timing, costs derived from incomplete contracts or the risky transfer of know-how to other firms, must be taken into account. These costs will be, at least partially, irrecoverable, leading to the stability of current networks.

Therefore, although competitive conditions have changed, radical alterations in the networks configurations would not be expected, at least in the short-medium term. The scarcity of papers analysing production networks stability support this idea. This is the case of Obashi (2010), who shows that the parts and components trade in Asian machinery networks tends to be more stable than trade in final goods.

In this context, the main objective of this paper is to analyse the changes in European automotive networks that have taken place since the mid-nineties. Specifically, we intend to determine whether the advances in the European integration process have led to the crowding out of senior countries participating in production sharing systems in favour of new Member States, in particular of those with costs advantages in the assembly stages (e.g., Spain); or whether they have just caused an expansion of production and trade capacity of those networks.

In the latter case, an extension rather than a replacement of networks would have taken place. In order to evaluate these expected changes, we estimate a gravity panel data model to study what are the determining factors of trade linked to cross-border production networks. Parts and components (P&C from henceforth) trade appears to be especially suitable for the analysis of

3

international production networks because, due to its intermediate nature, its foreign exchanges must inevitably be headed towards assembly or to its incorporation into a further stage of production in another economy. The period studied is between 1995 and 2007; that is, before the international financial crisis broke out.

We focus our analysis on the automotive industry for several reasons; firstly because it is one of the most fragmented industries. Specifically, several studies have pointed to the strong regional structure of the auto networks (Dhiel, 2001; Sturgeon et al., 2009). Secondly, the European automotive industry plays a prominent role in the world economy. In addition, it is a highly important sector for certain EU countries or even regions, where the threat of relocation often raises considerable public alarm. Lastly, previous analyses for NAFTA have revealed that advances in regional integration constitute a stimulus for international fragmentation in the automotive industry (Türkan and Ates, 2011). Therefore, it can be expected that the deepening of European integration will translate into changes in networks in this field. Nevertheless, the geography of networks could be particularly stable in the case of auto industry, where quality, technology and security standards are particularly high, driving up the transaction costs.

The reorganization of the automotive industry along with the propulsion of this sector in Eastern European countries since their EU accession has been the topic of numerous analyses.

However, this paper contributes to literature in two ways. On the one hand, although the use of P&C trade as a proxy for participation in international production networks is commonplace, it has seldom been used in studies concerning the automotive sector. This approach constitutes, then, a novelty for the sector analysis, allowing for a finer estimate of the determining factors of its fragmentation strategies. On the other hand, the study provides a regional focus, taking into consideration the 25 EU countries as a study scope. This view enables the gathering of changes taking place in the whole European network, both in new and old Member States.

The article is organized as follows. In section 2, we briefly describe the data and present descriptive evidence on the position of the European automotive industry in a global context and the main European players, through the analysis of their shares in world trade. In this section we also deal with the study of the geographical dimension of the EU automotive trade. The extended gravity model to be estimated is detailed in Section 3 and the econometric results are presented in section 4. Some conclusions are provided in Section 5.

2. DATA AND DESCRIPTIVE ANALYSIS.

As we mentioned above, trade in auto P&C is used as a proxy for cross border production networks1. Our main data source is the United Nations Commodity Trade Statistics Database (UN

1 It is important to note that this is a good proxy when P&C are mainly destined for further processing or assembly abroad, and not for replacement purposes. In this sense, the higher demand for replacement parts in auto industry could be considered a shortcoming for P&C trade as indicator of trade linked to cross-border production networks.

4

COMTRADE), which offers detailed information on international trade flows for practically every country in the world. More specifically, we use the information classified and recorded using the Standard International Trade Classification Revision 3 (SITC Rev.3), which makes a distinction between trade in parts and components (auxiliary industry) and final goods. Following SITC Rev.2 categories for automotive P&C and final products identified by Kaminski and Ng (2001), we provide a new code list corresponding to SITC Rev.3. (table A.1 in Statistical Appendix).

Automotive trade flows in the EU-25 have been very dynamic from 1995-2007, growing by 9 per cent annual cumulative in nominal terms. The dynamism of auto trade has been particularly high in P&C (around one percentage point over final goods), increasing its share up to 40 per cent in total auto trade in the EU-25. This fact is the consequence of intense processes of international fragmentation of production in the automotive sector, to the point of being considered at present as one of the most globalized industries. This growth has allowed the EU- 25 to maintain a prominent role in world trade throughout the whole period, with shares around 50 per cent, both in final and P&C markets (Figure 1). That is, in the expansive international context before the financial crisis, when the demand for cars grew steadily, the European automotive industry was able to maintain and expand its trade shares. This happened despite the tough competition from emerging countries such as Brazil, Russia, India, China and Mexico where the largest multinational firms of the sector have increased their investments with the objective of keeping costs down and supplying new markets.

The predominance of the European automotive industry trade has been accompanied in the last decade by profound changes in the organization of production. Specifically, two features are highlighted (Figure 1). First, the diverging evolution experienced by the two main areas in which the EU-25 can be divided – the EU-15 (countries that joined before the 2004 enlargement) and the EU-10 (countries that joined in 2004). While the EU-15 world shares fell substantially in final goods exports and were steady in P&C trade, the EU-10 has experienced a notable and progressive increase since 1995 in both shares. Therefore, it has been the dynamism of the activity in the Eastern European countries that has allowed the EU-25 to maintain (in final goods) and improve (in P&C) its competitive position in the global market. Specifically, the increasing share of the EU-25 in auto P&C world trade (from 46 to 54 per cent on the export side and from 44 to 50 on the import side) is attributable exclusively to the new enlargement countries. As predicted, the incorporation of the Eastern European countries into the EU has caused a geographic reorganization of the automotive industry in favour of the New Members2. These countries have been particularly active in attracting foreign investment from large companies in the sector and have intensified their trade considerably by means of a growing participation in European production sharing networks. These investment flows have come not only from Members States’ firms, but also from non-Members’ companies (Suzuki and Isuzu Motors of

2 Some firm-level examples of this production reorganization in automotive industry are reported in Dicken (2003).

5

Automotive P&C world import share (%)

0 2 4 6 8 10 12

Germany UK Spain France Belgium Italy Sweden Austria Netherland Poland Hungary Czech Rep. Slovak Rep. Portugal Denmark Finland Slovenia Greece Irland Lithuania Latvia Estonia Cyprus Malta

1995 2007

0 10 20 30 40 50 60

1995 2007

EU-15 EU-15

EU-10

EU-10

Automotive Final Goods world export's share (%)

0 2 4 6 8 10 12 14 16 18 20 22

Germany France Belgium Spain UK Italy Sweden Austria Netherland Czech Rep- Poland Slovak Rep. Hungary Finland Portugal Slovenia Lithuania Denmark Estonia Greece Irland Latvia Cyprus Malta

1995 2007

0 10 20 30 40 50 60

1995 2007

EU-10 EU-10

EU-15

EU-15

Automotive P&C world export share (%)

0 2 4 6 8 10 12 14 16 18

Germany France Italy Spain UK Poland Hungary Belgium Czech Rep. Austria Sweden Netherland Slovak Rep. Portugal Denmark Slovenia Finland Lithuania Estonia Irland Greece Latvia Malta Cyprus

1995 2007

0 10 20 30 40 50 60

1995 2007

EU-15 EU-15

EU-10

EU-10

Japan; Daewo, Hyundai and Kia of Korea) with the aim of supplying the European market from inside (Kaminsky and Ng, 2001).

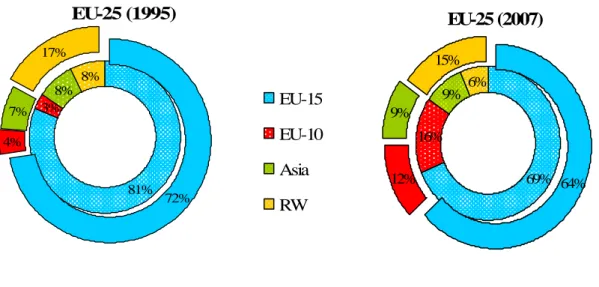

Figure 1. EU-25 automotive world trade shares

6

A second feature to be highlighted is the dissimilar evolution of certain Member States.

According to P&C export and import shares shown in Figure 1, it is clear that the key countries in the auto industry are the larger economies of the EU-15: first of all, Germany, and considerably behind, France, Italy, the United Kingdom and Spain. These five countries combined account for 37 per cent of world automotive exports and 70 per cent of EU exports in 2007 (with similar percentages when final goods and P&C are distinguished). Curiously enough, Spain is the only of these economies without its own car brand in her territory. After her accession to the EU, she attracted high FDI inflows, mainly from multinational companies which set up production plants in the country. Her emergence as a relevant supplier of both finished automobiles and auto P&C has been emphasized in several studies (e.g., Spatz and Nunnemkamp, 2002).

It is more interesting to observe how, while most advanced economies have reduced their influence in world automotive trade, Germany has strengthened her position, especially in P&C markets. Considering this, it may be affirmed that the German automotive industry has been especially active in the internationalization and fragmentation of production, leading this transformation within the EU-25. Amongst the EU-15 countries with a higher world trade share in automotive industry, only Spain and Belgium, both of them with a solid auto auxiliary industry, have been able to face new competitors and to maintain their relative participation in the P&C world market from 1995 to 2007, although Belgium has lost part of her import share.

Together with the German economy, the main competitive improvements are found in Poland, Hungary, the Czech Republic and Slovakia. Once again, their improvements are higher in P&C markets, showing their increasing participation in the European and world automotive market. In this context of competitive pressure from Eastern Europe, Spain´s ability to maintain her position and to even increase her export share in P&C markets can be seen as a real success for this country. A priori, this evolution would indicate that the unquestionable extension of the European automotive networks towards the East is compatible with the active participation of other peripheral nucleus, whose main actor is Spain.

It is important to note that integration into auto networks for these Central-Eastern European Member States, as well as previously for Spain, has been foreign-led (Radosevic and Rozeik, 2005; Jakubiak et al., 2008). Since the beginning of the 90s, a large amount of foreign investment has flourished because of country specific factors such as lower wage costs, proximity to core EU markets, socialist heritage in the automotive industry, skilled labour and privatisation policies. Additionally, accession into the EU has induced European multinationals to rapidly enter Eastern markets (VW) or deepen their presence therein (Fiat, Renault), in order to extend their regional networks.

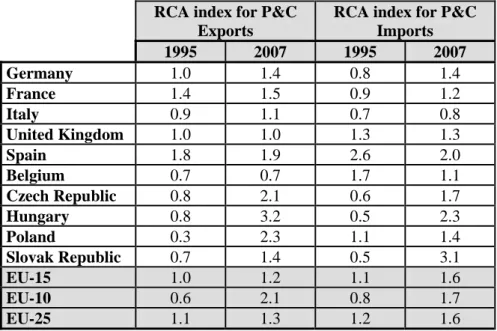

The calculation of the Balassa index of revealed comparative advantage (RCA) on P&C exports and imports shows that these four countries plus Germany, France and Spain have double RCA (above unity) which would indicate, following Kaminski and Ng (2001), an active

7

EU-25 (1995)81%

3%

8%

8%

72%

4%

7%

17%

EU-25 (2007)

69%

16%

9% 6%

12% 64%

9%

15%

EU-15 EU-10 Asia RW

involvement in production sharing activity3. RCA indexes exceeding unity for exports and imports mean more specialization in exports of P&C (revealing the existence of advantages in the production and exportation of P&C) and more specialization in imports of P&C (revealing the existence of comparative advantage in assembly operations).

The increasing integration of Central and East European countries into automotive production networks is also exhibited when we analyse the changes in the direction of auto P&C trade in the EU-25. Even though its main trading partners are the EU-15 economies, a movement towards the 2004 accession countries can be observed throughout the period (Figure 2). So, the restructuring of European automotive networks that EU enlargement has caused can be appreciated. Since the clear preponderance of intra-EU flows, the dominant trend is still towards a strong regional structure of automotive networks. But today this is a much larger regional-scale, as some East Europe Member States are incorporated.

Figure 2: Direction of trade in automotive P&C in EU-25

3. ESTIMATING A GRAVITY MODEL FOR AUTOMOTIVE PARTS AND COMPONENTS TRADE

In order to establish the effects of the explanatory factors on European trade linked to international production networks in the automotive industry, we propose to estimate a gravity model. These models, initially developed by Tinbergen (1962) and Anderson (1979), explain the volume of bilateral trade flows according to the size of the trading economies (a positive influence because it is associated with a wider available market) and the bilateral trade costs (which depend on variables such as the physical distance between trading partners, sharing a border or a colonial past, or belonging to the same regional integration agreement). We are particularly interested in the last variable, since intra-EU trade is prevalent in the auto industry. We expect that the country’s EU membership will be a determining factor in explaining its participation in

3 See Table A.2. in Statistical Appendix.

8

European production networks. The reason is that trade between Member States will be less subject to both trade barriers and economic, legal and political uncertainties or exchange risks (Zeddies, 2007). Moreover, since P&C may cross borders more than once, the trade stimulating effect of EU membership will be particularly high for these intermediate goods.

We augment the standard gravity model with several explanatory variables pointed out by the theoretical literature on international production fragmentation. The first group of specific variables links this strategy to the exploitation of comparative advantages (Arndt, 1997; Deardorff, 2001; Jones and Kierzkowski, 1990 and 2001). That is, some stages of the production process can be carried out more efficiently in specific locations, taking their comparative advantages into account.

Although labour content is relatively low in the car industry (between 5 and 10 per cent), labour cost may remain as a relevant factor, mainly in a framework where competition is tightening and the wage differential is still substantial between Eastern and Western Europe (Sachwald, 2005). Hence, in order to capture comparative advantages from differences in wages, we introduce the relative wage differences among trading countries in the model. If we assume that production of P&C is a less labour-intensive activity than assembly, countries with higher relative wages in the auto industry will enjoy a comparative advantage in production and exportation of P&C, while those countries with lower relative wages will enjoy a comparative advantage in the importation of P&C and assembly stages. So, we expect the relative wages variable to have a positive impact on P&C exports.

Moreover, although we assume that P&C trade, or specifically, international production networks, are driven by the existence of comparative advantages between countries, we can argue that certain minimum conditions concerning technological or institutional capacity at the country level must be guaranteed to be incorporated into these networks. In this respect, an excessive gap in the economic development of trading countries could act as an obstacle to networking. According to available empirical evidence, production sharing networks are integrated by countries with a medium level of development. In them, the minimum requirements that make the internationalisation of the value chain feasible in the best efficiency conditions are assured. The need for minimum factor endowment requirements is even higher in the automotive industry, where suppliers and automakers maintain a close collaboration at the level of design and quality. In this paper we introduce the absolute value of the difference in GDP per capita to capture the impact of the basic requirements for establishing networks.

Nevertheless, efficiency gains derived from the exploitation of the comparative advantages at each stage of production can be reduced and even disappear if transport, coordination and supervision costs are excessively high. That is, if “service link costs”, referring to the costs of connecting production blocks in different locations, are excessive. The more complex the production fragmentation procedure and the wider the international production networks, the

9

greater the exploitation of comparative advantages, but the costs of these services will also be greater. The balance between service link costs and benefits derived from maximum exploitation of the advantages of the international division of labour and from intra-product specialisation will determine the optimal degree of international fragmentation of production. Although a general decrease of service link costs has been observed, these continue to differ greatly between countries, thus affecting an individual country’s possibility of taking part in production sharing networks. For that reason, the standard gravity model is extended to include a second group of variables which introduces the service link costs, proxied by the quality of transport and telecommunications infrastructure. These factors are especially important to an auto industry where quality control and delivery timing are essential to business. A positive sign in their coefficients is expected: the greater the infrastructure quality, the lower the service link costs and the higher the trade linked to production sharing networks.

Additionally, the home country may benefit from a “headquarters effect”, that is, an unusually high concentration of production and exports. As Sturgeon et al. (2009) indicate, multinational automakers strongly influence on the location decisions in the auxiliary automotive industry. Parts and subsystems have tended to concentrate into a few geographic clusters, typically near the automaker companies. Physical proximity facilitates the increasing demand of product differentiation, the transport cost reduction, mainly in modules with higher size and weight, and the advantages of production systems as lean manufacturing. Economic globalization and changes in production strategies have opened the door to new possibilities of geographical organization of production; however, reasons to maintain some traditional location guidelines still exit. Among them, besides the technical reasons mentioned above, it is important to highlight political pressures to maintain “in house” industries with elevated employment levels, high unionization rates and a strong influence on the local economy. To capture this headquarters effect, we include a dummy variable in the regressions, equal to 1 if the parent company is from country i and zero otherwise.

Finally, time dummy variables (Dt) are included to control for the impact of time-varying factors that affect all the countries, such as technological improvements or the multilateral reduction of trade barriers that result in lower costs for connecting segmented stages of production process.

Therefore, the gravity model specification that we propose is the following:

[Specification 1]

ln Xijt = β0 + β1 ln GDPit + β2 ln GDPjt + β3 ln Bilateral distanceij + β4 Shared borderij + β5 Colonial pastij + β6 EUijt + β7 Headquarteri +β8 ln Relative-wagesijt + β9 ln ADif-GDPpcijt + β10 ln Infrastructureijt + Dt + εit

10

The dependant variable reflects a country’s participation in cross-border production networks. It is proxied by country i exports (imports) of auto P&C to (of) country j, that is, bilateral trade in auto P&C expressed in nominal terms4,5. The model is estimated for bilateral trade of EU- 25 countries with their major partners in auto P&C for the period 1995-2007. Specifically, forty-six countries, mainly from Europe but also from America, Asia or Africa, are included as partners in the model (Table A.3 in the Statistical Appendix). There are hardly any zeros in our dataset (less than eight per cent of observations), since it involves only main trading partners. The subscripts i and j respectively refer to the countries of origin and destination of the exports, and t to the year.

Regarding the expected signs of the explanatory variables, the GDPit and GDPjt variables measure the size of the trading economies (country i and country j) and then a positive value for both coefficients is expected. Trade associated with international fragmentation of production will increase if the distance between the trading countries decreases (Bilateral distanceij), if the countries share a border (Shared borderij) or a colonial past (Colonial pastij) or belong to the European Union (EUijt) or if there is a headquarter effect in the exporting country (Headquarteri).

As regards the more specific hypotheses of the international fragmentation models, we would expect a negative impact of the ADif-GDPpcijt variable if the gap in the economic development of the trading countries is too wide for an adequate functioning of production sharing processes; and a positive impact of the Relative-wagesijt variable if a comparative advantage in terms of a lower wages favours the importation of P&C and, therefore, the assembly activities in the motor vehicle industry. Finally, we would expect a positive coefficient for the Infrastructureijt variable if a greater quality of transport and communications infrastructure enhances participation in cross-border automotive production networks6.

4. ECONOMETRIC RESULTS.

The results of the estimates are presented in the first column of Table 1. It can be observed that all the coefficients are significant and display the expected sign. Concerning the standard variables in the gravity models, the economic size of the trading countries has a positive impact on the P&C trade with coefficients close to the unit as predicted by the theory, while the bilateral trade costs have a negative impact. In particular, the distance between countries

4 A common error in papers that estimate gravity models is the deflation of exports. Baldwin et al. (2008, pg. 15) qualify this as the “bronze medal” in the race of errors in gravity models in international trade. According to these authors, deflation in this case is an error because “all the prices in the gravity equation are measured in terms of a common numeraire, so there is no price illusion”.

5 In theory, country j exports of P&C to country i should be identically equal to country i imports of P&C from country j, but in practice they are not for different reasons. Most authors estimate the gravity model using import data because they are regarded to be more reliable than export data since imports are carefully collected for custom duties in each country. Although in our dataset this appreciation would be only important for extra-EU trade, we use import data.

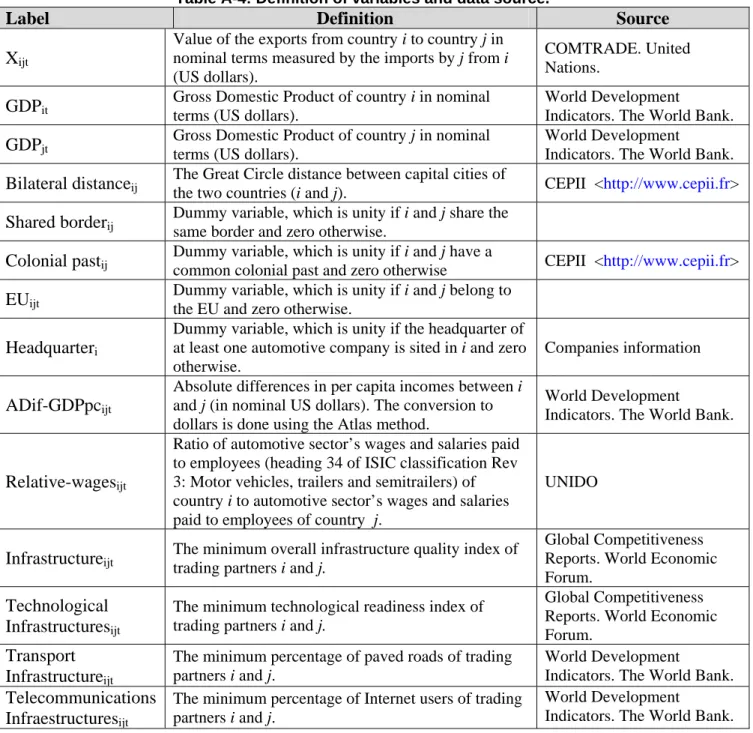

6 See Table A4. in the Statistical Appendix for an explanation of the measurement of the model’s variables and the statistics used.

11

discourages trade associated with production sharing networks (because it increases bilateral trade resistance), while sharing a border or a colonial past increases the trade value (given that it reduces the bilateral resistance). The coefficient of the EU dummy variable shows the expected positive sign and it is statistically different from zero. So, there is (omit “a”) clear evidence to support the hypothesis that regional trade agreements such as the EU promote cross-border networking. Moreover, the reductions of trade barriers derived from the advances in the EU integration process would have generated new incentives for fragmentation of production in the European context. The dummy variable to capture the headquarter effect is also positive and statistically significant. This result would indicate that hosting the companies’ headquarters is a powerful reason for several senior Member States to still show strong participation in the production networks.

Regarding the specific variables for models of international fragmentation of production, the negative and significant coefficient of the absolute differences in GDP per capita allows us to defend our hypothesis that a large gap in the economic development between countries implies a restriction for auto P&C trade and discourages from establishing cross-border production networks. The idea that comparative advantage would only hold for countries that have reached a certain level of factor endowment (a minimum threshold of development) is also suggested by other papers such as Türkan and Ates (2011). These authors also obtain a negative effect of dissimilarities in GDP per capita on US vertical intra-industry trade in auto-parts industry, suggesting that these capture the differences in public infrastructures, favorable policy environment, skilled labour and industrial agglomeration, which would hamper the creation of cross-border production networks.

The proxy variable of comparative advantages or disadvantages (the relative wages) yields a positive and significant coefficient. The greater the EU country’s wages compared to a trading partner, the greater its P&C exports to that partner (or greater P&C imports to that partner from the EU country).

The positive sign obtained for variables that approximate the quality of infrastructure supports the hypothesis that participation in automotive production networks increases with the quality of these infrastructures in the countries involved. This will guarantee that the service link costs associated with the fragmentation and dispersion of the production will not be as high, as they cancel the profits derived from exploiting the comparative advantages of different locations.

Specifically, we used two indicators to approximate the quality of the infrastructures: an overall infrastructure index and a technological readiness index, both of them offered in the Global Competitiveness Reports elaborated by the World Economic Forum7. As expected, the

7 The first index makes reference jointly to the quality of roads, railroad, port, air transport infrastructures, along with the available seat kilometres, quality of electricity supply and the number of telephones lines; whereas the second one refers to the availability of latest technologies, the firm-level technology absorption, the laws relating

12

correlation between both indexes is very high (0.78); hence we analysed the impact of these variables on the P&C trade in two different specifications (Column 1 and 2 in Table 1). No matter the index used, the coefficients were positive and significant. These indexes are available only from the year 2000 onward, reducing the number of observations appreciably. When they are omitted from the model and the whole sample is used, the other variables remain practically unchanged (Column 3 in Table 2).

Table 1: Results of the extended gravity model estimates for the EU trade in auto P&C Coefficients Column (1) Column (2) Column (3) Column (4) Column (5)

GDPi 1.187*** 1.069*** 1.090***

(0.022) (0.023) (0.018)

GDPj 0.962*** 0.925*** 0.946***

(0.016) (0.017) (0.013) Bilateral distance ‐0.883*** ‐0.794*** ‐1.041***

(0.030) (0.031) (0.025)

Common border 1.011*** 1.082*** 0.884***

(0.103) (0.101) (0.090)

Colonial past 0.714*** 0.703*** 0.577***

(0.118) (0.121) (0.101)

EU 0.657*** 0.794*** 0.546*** 0.749*** 0.781***

(0.065) (0.065) (0.052) (0.068) (0.069)

Headquarter 0.583*** 0.661*** 0.971*** 1.027***

(0.065) (0.065) (0.053) (0.049)

ADif-GDPpc ‐0.036* ‐0.036* ‐0.128*** ‐0.042* ‐0.054**

(0.021) (0.021) (0.017) (0.024) (0.024) Relative-wages 0.139*** 0.154*** 0.141*** 0.180*** 0.204***

(0.015) (0.015) (0.013) (0.008) (0.009)

Infrastructure 0.225***

(0.024)

Technological Infrastructures 0.267***

(0.031)

Time dummies Yes Yes No No

Country-pair specific fixed effects (Dij) No No Yes Yes Time varying exporter and importer

fixed effects (Dit, Djt) No No Yes Yes

Number of observations 6723 6356 10267 10272 10272

Adjusted R2 0.672 0.649 0.638 0.857 0.851

Note: Standard errors in brackets. ***, ** and * indicate significance levels of 1, 5 and 10 percent respectively.

Robustness analysis.

to ICT, the transfer of technology and foreign direct investments, the mobile telephone subscriptions, the number of Internet users, personal computers and broadband Internet subscribers.

13

To check the robustness of the obtained results, we have conducted some sensitivity analyses. Specifically, we estimate the model incorporating different types of fixed effects. First of all, we estimated the model introducing country-pair-specific dummy variables (Dij). Gravity models tend to include variables for establishing the impact of natural trade barriers (distance, shared border), cultural barriers (shared colonial past) or barriers imposed by the trade policy (member of the same regional integration agreement). But, these variables may not represent the total potential trade bilateral costs. It is very likely that other factors (specific to each country-pair) have an impact on bilateral trade; so that the estimation results will be biased when they are omitted from the model. To control for the impact of any time-invariant bilateral variables, gravity equation is estimated replacing time-invariant bilateral variables such as bilateral distance, common language or common borders with fixed country-pair effects.

Secondly, we estimate the model including time-varying exporter and importer fixed effects (Dit y Djt). As Anderson and van Wincoop (2003, 2004) point out, the volume of trade between any two countries does not only depend on the cost of bilateral trade (or bilateral trade resistance). It also depends on bilateral trade costs relative to the cost of trade with other economies (what they term multilateral trade resistance). Ceteris paribus, the greater the multilateral trade resistance, the greater the bilateral trade. So, when these multilateral trade costs are omitted from the gravity equation, biased estimates will be obtained8. A simple method to control for this effect of multilateral trade resistance is to use time-varying exporter and importer dummy variables (Dit y Djt). To ensure the unitary elasticity for income restriction (coefficients close to unity for GDPit and GDPjt variables) derived from the theoretical foundations of gravity equation, Anderson and van Wincoop (2003) divide the dependent variable by the product of exporter and importer GDP’s. Taking these considerations into account, the specification to be estimated is the following9:

[Specification 2]

ln [Xijt / GDPit GDPjt)]= β0 + β1EUijt + β2 Headquarteri + β3ln Relative-wagesijt + β4ln ADif-GSPpcijt+ β5ln Infrastructureijt + Dij + Dt + Dit + Djt +εit

The introduction of exporter-time and importer-time dummies as well as time-invariant country-pair fixed effects does not alter the sign and significance of the coefficients as it is showed in the fourth column of Table 2 (dummy coefficients are omitted for brevity). So, our results are robust to the introduction of different fixed-effects. Since the infrastructure indicators used are index numbers (values from 0 to 7) and they hardly vary over time, when bilateral time-

8 “Gold medal” error of gravity models (Baldwin et al., 2008).

9 Although Anderson (1979) proposes a theoretical model with non unitary income elasticities once non tradable goods are taking into account, moving exporter and importer GDPs to the left hand side allows us to control for potential endogeneity between GDP and bilateral trade flows, since exports and imports are part of GDP. This potential endogeneity is pointed out by Baier and Begstrand (2007) but they also defend that it could be ignored without affecting the results.

14

invariant dummies are included, these specific indicators need to be removed. Additionally, considering that Headquarteri is a country-specific dummy variable and that there may be multicollinearity problems, we estimate the model omitting this variable. Also in this case, the results remain robust (last column of table 2).

Taking into account that adding fixed effects improves the overall fit of the model, particularly in the case of time varying nation dummies, we can interpret that auto P&C trade is also explained by country-specific fixed effects. Among these country specific characteristics that could affect P&C trade, we may consider the domestic industrial policy for the automotive sector, anticipated liberalizing effects of the European integration process, a long tradition in car production industry or a different use of strategies of fragmentation and internationalization of production by firms10.

5. CONCLUSIONS AND POLICY IMPLICATIONS.

In this paper we present evidence regarding the changes in European production networks in the auto industry since the mid-nineties, when a new impetus to EU deepening and enlargement was given. The new Eastern European Members have significantly increased their participation in both auto P&C and final automotive trade. Amongst the Fifteen, only Germany, the unquestionable European automotive leader, has been able to appreciably increase her trade shares. The case of Spain is also remarkable since it has managed to maintain her position and even to increase her export share in P&C markets. These features show that the EU enlargement has led to a spatial extension of European automotive networks towards the East, which is compatible with the active participation of other peripheral nucleus, mainly Spain.

Using an extended gravity panel data model, we have estimated the determining factors of P&C trade for the EU-25 as a proxy for participation in international production networks. The descriptive analysis suggests and our econometric results corroborate that EU membership and comparative advantages are key determining factors to be integrated into cross-border production sharing systems, but others factors also seem to matter: not only are some Central-Eastern new Member States really engaged in networking, but also other senior Member States such as Spain, whose labour cost advantages have disappeared in the Enlarged EU context, yet manage to preserve its involvement11. That would mean that the availability of cheap labour is not a sufficient factor to enter competitively in the process of international fragmentation of production,

10 We have estimated the model adding variables which try to capture some of these factors (e.g. FDI inflows into auto industry), but their coefficients are not significant and the overall fit of the model is not improved. This occurs because they are determining factors only for certain countries.

11 Some authors (Bilbao and Camino, 2008; Aláez and Barneto, 2008) have stressed that automotive firms operating in Spain show a low risk of business relocation when factors influencing vulnerability to corporate restructuring processes (such as the importance of price as a significant factor for competitiveness in the industry, the sunk costs associated with plant relocation and the distance of the plant from the corporative headquarter) are taken into account.

15

especially in relatively skill intensive industries, as suggested by Barba-Navaretti, Haaland and Venables (2002).

Automotive companies have made use of opportunities created by the EU enlargement to reshape production networks for a better exploitation of comparative advantages within the region. With this strategy, they have been able to maintain competitiveness despite the intense competition from less developed areas. As the European Commission (2007) argues, in the changing playing field of global commerce, competitive advantage lies in optimising the global value chain. So, the EU should continue removing trade barriers to encourage production fragmentation strategies in the global economy. It seems necessary to step up efforts to expand the single market in the area of goods and services, removing regulations that restrict their free movements and consequently facilitating the reorganization of networks.

Besides EU membership and comparative advantages, other variables such as good quality infrastructure, a minimum threshold of development and a headquarter effect emerge as important determinants of networking in automotive industry. The relevance of the first two variables points out how EU regional policy could contribute to strengthening European networks.

It seems clear that development disparities between regions can be reduced by encouraging investment in transport and telecommunications infrastructure. This implies that an adequate regional policy could diminish largely the service link costs and promote the insertion of less developed Members into European networks. In doing so, it would facilitate a more efficient configuration of the European production networks, boosting European competitiveness and accelerating growth in lagging Members. In words, it would improve economic and social cohesion in the EU.

Finally, the estimates also confirm that unobserved country-specific variables, which have been controlled by including time-varying nation fixed effects, play a key role in production sharing networks. Some of these country-specific variables could help to explain the geographical configuration of automotive production networks in the enlarged EU, particularly why some countries can preserve their position in the network even though they have lost their comparative advantages after the enlargement (the case of Spain). It may, therefore, be assumed that changes in the comparative advantages lead to an alteration in the network configuration and the creation of new locations, but it does not necessary involve the replacement of traditional ones.

A possible explanation can be found in the existence of sunk costs in the participation in production sharing networks, first and foremost when this is associated with the presence of foreign capital firms in the sector. Due to high investment in long-lived capital equipment and skills, and the close linkages between automakers and suppliers, the geography of automotive networks tends to be stable (Sturgeon et al., 2009). Although the early choice of a country by multinational firms as a location for assembly activities can be the result of economic history, multinational firm affiliates become increasingly embedded in host countries, making relocation

16

more difficult. The importance of country-specific factors recommends the implementation of active domestic economic policies, such as encouraging investments to guarantee enough technological capacity and skilled labour, in short, enough level of productivity, to attract and retain leading firms in the industry; and when these are foreign capital firms, strengthening the linkages with the local economy in order to facilitate the integration of domestic firms into the network.

17

References:

Aláez, R. and Barneto. M., 2008. Evaluating the Risk of Plant Closure in the Automotive Industry in Spain. European Planning Studies, 16, 1, 61-80.

Anderson, J.E., 1979. A Theoretical Foundation for the Gravity Equation. American Economic Review, 69, 1, 106-116.

Anderson, J.E. and van Winccop, E., 2003. Gravity with Gravitas: A Solution to the Border Puzzle. American Economic Review, 93, 170-192.

Anderson, J.E. and van Wincoop, E., 2004. Trade Costs. Journal of Economic Literature, 45, 691- 741.

Athukorala, P. and Yamashita, N., 2006. Production Fragmentation and Trade Integration: East Asia in a Global Context. The North American Journal of Economics and Finance, 17, 3, 233-256.

Arndt, S. W., 1997. Globalization and the Open Economy. The North American Journal of Economics and Finance, 8, 1, 71-79.

Baier, S.L. and Bergstrand, J., 2007. Do Free Trade Agreements Actually Increase Members.

Journal of International Economics, 71, 1, 72-95.

Baldwin, R.E., Di Nino, V., Fontagne, L., De Santis, R.A., and Taglioni, D., 2008. Study on the Impact of the Euro on Trade and Foreign Direct Investment. European Economy, Economic Papers, 321.

Barba Navaretti, G., Haaland, J.I. and Venables, A., 2002. Multinational Corporations and Global Production Networks: The Implications for Trade Policy. Centre For Economic Policy Research, London.

Bilbao, J. and Carmino, V., 2008. Proximity Matters? European Union Enlargement and Relocation of Activities. The case of the Spanish Automotive Industry. Economic Development Quarterly, 22, 2, 149-166.

European Commission, 2007. Mid-term Review of Industrial Policy. A Contribution to the EU’s Growth and Job Strategy. COM 2007 374 final.

Deardorff, A., 2001. Fragmentation in Simple Trade Models. North American Journal of Economics and Finance 12, 2, 121-137.

Dhiel, M., 2001. International Trade in Intermediate Inputs: The case of the Automobile Industry.

Kiel Working paper, 1027.

Dicken, P., 2003. Global Production Networks in Europe and East Asia: The Automobile Components Industries. GPN Working Paper 7, University of Manchester.

Jakubiak, M., Kolesar, P., Izvorski, I., and Kurekova, L., 2008. The Automotive Industry in the Slovak Republic: Recent Developments and Impact on Growth. Commission on Growth and Development Working Paper 29, Washington, DC.

Jones, R.W. and Kierzkowski, H., 1990. The Role of Services in Production and Internacional Trade: A Theoretical Framework, in: Jones, R. and Krueger. A. Eds., The Political Economy of International Trade. Basil Blackwell, Oxford.

Jones, R.W. and Kierzkowski, H., 2001. A Framework for Fragmentation, in: Arndt, S.W. and Hierzkowski, H. Eds., Fragmentation. New Production Patterns in the World Economy.

Oxford University Press, Oxford.

Kaminski, B. and Ng, F., 2001. Trade and Production Fragmentation: Central European Economies in EU Networks of Production and Marketing. Policy Research Working Paper, 2611, The World Bank.

Obashi, A., 2010. Stability of Production Network in East Asia: Duration and Survival Trade.

Japan and the World Economy 22, 1, 21-30.

Radosevic, S. and Rozeik, A., 2005. Foreign Direct Investment and Restructuring in the Automotive Industry in Central and East Europe. Centre for the Study of Economic &

Social Change in Europe, Working Paper, 53, University College London.

Sachwald, F., 2005. The impact of EU Enlargement on the Location of Production in Europe. Les Etudes de 1'IFRI, 4.

Spatz, J. and Nunnenkamp, P., 2002. Globalization of the Automobile Industry: Traditional Locations under Pressure?. Kiel Working Papers, 1093, Institute for World Economics.

18

Sturgeon T.J., Memedovic, O., Van Bieserbroeck, J. and Gereffi, G., 2009. Globalisation of the Automotive Industry: Mean Features and Trends. International Journal of Technological Learning, Innovation and Development, 2, 1/2, 7-24.

Tinbergen, J., 1962. Shaping the World Economy: Suggestions for an International Economic Policy. The Twentieth Century Fund, New York.

Türkan, K. and Ates, A., 2011. Vertical Intra-industry Trade and Fragmentation: An Empirical Examination of the U.S. Auto-Parts Industry. The World Economy, 34, 1, 154-172.

Williamsom, O.E., 1975. Markets and Hierarchies: Analysis and Antitrust Implications. Free Press: New York.

Zeddies, G., 2007. Determinants of International Fragmentation of Production in the European Union. IWH Discussion Papers, 15/07, Halle Institute for Economic Research.

19

Statistical Appendix.

Table A.1: Automotive Parts and Components and Final Products (SITC Rev. 3 headings included).

PARTS AND COMPONENTS:

713.2,Internal combustion piston engines for propelling vehicles

713.82, Other compression-ignition internal combustion engines (diesel or semi-diesel) 713.9,Parts, n.e.s, for the internal combustion piston engines

744.19,Parts of the trucks and tractors

778.3, Electrical equipment, n.e.s., for internal combustion engines and vehicles; parts thereof

778.31,Electrical ignition or starting equipment of a kind used for spark-ignition or compression-ignition internal combustion engines

778.33,Parts of the equipment of heading 778.31 778.34, Electrical lighting or signalling equipment 778.35, Parts of the equipment of heading 778.34 784,Parts and accessories of motor vehicles

784.1,Chassis fitted with engines, for motor vehicles 784.2,Bodies (including cabs), for motor vehicles 784.3,Other parts and accessories of motor vehicles

784.31, Bumpers, and parts thereof

784.32, Other parts and accessories of bodies (including cabs) 784.33, Brakes and servo-brakes and parts thereof

784.34, Gearboxes

784.35, Drive-axles with differential, whether or not provided with other transmission components

784.36, Non-driving axles, and parts thereof 784.39, Other parts and accessories

FINAL GOODS

781, Motor cars and other motor vehicles principally designed for the transport of persons 782, Motor vehicles for the transport of goods and special-purpose motor vehicles 783, Other road motor vehicles

722, Tractors

744.11, Self-propelled trucks powered by an electric motor, fitted with lifting or handling equipment

20

Table A-2. Balassa RCA indexes for P&C imports and exports in the EU-25 RCA index for P&C

Exports

RCA index for P&C Imports

1995 2007 1995 2007

Germany 1.0 1.4 0.8 1.4

France 1.4 1.5 0.9 1.2

Italy 0.9 1.1 0.7 0.8

United Kingdom 1.0 1.0 1.3 1.3

Spain 1.8 1.9 2.6 2.0

Belgium 0.7 0.7 1.7 1.1

Czech Republic 0.8 2.1 0.6 1.7

Hungary 0.8 3.2 0.5 2.3

Poland 0.3 2.3 1.1 1.4

Slovak Republic 0.7 1.4 0.5 3.1

EU-15 1.0 1.2 1.1 1.6

EU-10 0.6 2.1 0.8 1.7

EU-25 1.1 1.3 1.2 1.6

Note: RCAij=(Xij/Xj)/(Xiw/Xw) with Xij as the exports of product i from country j; Xj total exports of manufactures from country j; Xiw the world exports of product i; and Xw the world total exports of manufactures.

Similarly, the RCA index is calculated for import of P&C and export of final goods.

Table A-3. Countries included in the model (EU’s main partners in auto P&C trade).

Regions Countries

EU

Austria, Belgium-Luxembourg, Bulgaria, Cyprus, Czech Rep., Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Malta, Netherlands, Poland, Portugal, Romania, Slovak Rep., Slovenia, Spain, Sweden, UK.

Rest of Europe

Norway, Russia, Switzerland and Turkey.

America

Argentina, Brazil, Canada, Mexico and USA.

Africa

Morocco and South Africa.

Asia

China, India, Japan, Rep. of Korea and Thailand

21

Table A-4: Definition of variables and data source.

Label Definition Source

X

ijtValue of the exports from country i to country j in nominal terms measured by the imports by j from i (US dollars).

COMTRADE. United Nations.

GDP

it Gross Domestic Product of country i in nominal terms (US dollars).World Development

Indicators. The World Bank.

GDP

jt Gross Domestic Product of country j in nominal terms (US dollars).World Development

Indicators. The World Bank.

Bilateral distance

ij The Great Circle distance between capital cities ofthe two countries (i and j). CEPII <http://www.cepii.fr>

Shared border

ij Dummy variable, which is unity if i and j share the same border and zero otherwise.Colonial past

ij Dummy variable, which is unity if i and j have acommon colonial past and zero otherwise CEPII <http://www.cepii.fr>

EU

ijt Dummy variable, which is unity if i and j belong to the EU and zero otherwise.Headquarter

iDummy variable, which is unity if the headquarter of at least one automotive company is sited in i and zero otherwise.

Companies information

ADif-GDPpc

ijtAbsolute differences in per capita incomes between i and j (in nominal US dollars). The conversion to dollars is done using the Atlas method.

World Development

Indicators. The World Bank.

Relative-wages

ijtRatio of automotive sector’s wages and salaries paid to employees (heading 34 of ISIC classification Rev 3: Motor vehicles, trailers and semitrailers) of country i to automotive sector’s wages and salaries paid to employees of country j.

UNIDO

Infrastructure

ijt The minimum overall infrastructure quality index of trading partners i and j.Global Competitiveness Reports. World Economic Forum.

Technological Infrastructures

ijtThe minimum technological readiness index of trading partners i and j.

Global Competitiveness Reports. World Economic Forum.

Transport Infrastructure

ijtThe minimum percentage of paved roads of trading partners i and j.

World Development

Indicators. The World Bank.

Telecommunications Infraestructures

ijtThe minimum percentage of Internet users of trading partners i and j.

World Development

Indicators. The World Bank.

F

UNDACIÓN DE LASC

AJAS DEA

HORROSDOCUMENTOS DE TRABAJO

Últimos números publicados

159/2000 Participación privada en la construcción y explotación de carreteras de peaje Ginés de Rus, Manuel Romero y Lourdes Trujillo

160/2000 Errores y posibles soluciones en la aplicación del Value at Risk Mariano González Sánchez

161/2000 Tax neutrality on saving assets. The spahish case before and after the tax reform Cristina Ruza y de Paz-Curbera

162/2000 Private rates of return to human capital in Spain: new evidence F. Barceinas, J. Oliver-Alonso, J.L. Raymond y J.L. Roig-Sabaté 163/2000 El control interno del riesgo. Una propuesta de sistema de límites

riesgo neutral

Mariano González Sánchez

164/2001 La evolución de las políticas de gasto de las Administraciones Públicas en los años 90 Alfonso Utrilla de la Hoz y Carmen Pérez Esparrells

165/2001 Bank cost efficiency and output specification Emili Tortosa-Ausina

166/2001 Recent trends in Spanish income distribution: A robust picture of falling income inequality Josep Oliver-Alonso, Xavier Ramos y José Luis Raymond-Bara

167/2001 Efectos redistributivos y sobre el bienestar social del tratamiento de las cargas familiares en el nuevo IRPF

Nuria Badenes Plá, Julio López Laborda, Jorge Onrubia Fernández

168/2001 The Effects of Bank Debt on Financial Structure of Small and Medium Firms in some Euro- pean Countries

Mónica Melle-Hernández

169/2001 La política de cohesión de la UE ampliada: la perspectiva de España Ismael Sanz Labrador

170/2002 Riesgo de liquidez de Mercado Mariano González Sánchez

171/2002 Los costes de administración para el afiliado en los sistemas de pensiones basados en cuentas de capitalización individual: medida y comparación internacional.

José Enrique Devesa Carpio, Rosa Rodríguez Barrera, Carlos Vidal Meliá

172/2002 La encuesta continua de presupuestos familiares (1985-1996): descripción, representatividad y propuestas de metodología para la explotación de la información de los ingresos y el gasto.

Llorenc Pou, Joaquín Alegre

173/2002 Modelos paramétricos y no paramétricos en problemas de concesión de tarjetas de credito.

Rosa Puertas, María Bonilla, Ignacio Olmeda

174/2002 Mercado único, comercio intra-industrial y costes de ajuste en las manufacturas españolas.

José Vicente Blanes Cristóbal

175/2003 La Administración tributaria en España. Un análisis de la gestión a través de los ingresos y de los gastos.

Juan de Dios Jiménez Aguilera, Pedro Enrique Barrilao González 176/2003 The Falling Share of Cash Payments in Spain.

Santiago Carbó Valverde, Rafael López del Paso, David B. Humphrey Publicado en “Moneda y Crédito” nº 217, pags. 167-189.

177/2003 Effects of ATMs and Electronic Payments on Banking Costs: The Spanish Case.

Santiago Carbó Valverde, Rafael López del Paso, David B. Humphrey

178/2003 Factors explaining the interest margin in the banking sectors of the European Union.

Joaquín Maudos y Juan Fernández Guevara

179/2003 Los planes de stock options para directivos y consejeros y su valoración por el mercado de valores en España.

Mónica Melle Hernández

180/2003 Ownership and Performance in Europe and US Banking – A comparison of Commercial, Co- operative & Savings Banks.

Yener Altunbas, Santiago Carbó y Phil Molyneux

181/2003 The Euro effect on the integration of the European stock markets.

Mónica Melle Hernández

182/2004 In search of complementarity in the innovation strategy: international R&D and external knowledge acquisition.

Bruno Cassiman, Reinhilde Veugelers

183/2004 Fijación de precios en el sector público: una aplicación para el servicio municipal de sumi- nistro de agua.

Mª Ángeles García Valiñas

184/2004 Estimación de la economía sumergida es España: un modelo estructural de variables latentes.

Ángel Alañón Pardo, Miguel Gómez de Antonio

185/2004 Causas políticas y consecuencias sociales de la corrupción.

Joan Oriol Prats Cabrera

186/2004 Loan bankers’ decisions and sensitivity to the audit report using the belief revision model.

Andrés Guiral Contreras and José A. Gonzalo Angulo

187/2004 El modelo de Black, Derman y Toy en la práctica. Aplicación al mercado español.

Marta Tolentino García-Abadillo y Antonio Díaz Pérez 188/2004 Does market competition make banks perform well?.

Mónica Melle

189/2004 Efficiency differences among banks: external, technical, internal, and managerial Santiago Carbó Valverde, David B. Humphrey y Rafael López del Paso

190/2004 Una aproximación al análisis de los costes de la esquizofrenia en españa: los modelos jerár- quicos bayesianos

F. J. Vázquez-Polo, M. A. Negrín, J. M. Cavasés, E. Sánchez y grupo RIRAG 191/2004 Environmental proactivity and business performance: an empirical analysis

Javier González-Benito y Óscar González-Benito

192/2004 Economic risk to beneficiaries in notional defined contribution accounts (NDCs) Carlos Vidal-Meliá, Inmaculada Domínguez-Fabian y José Enrique Devesa-Carpio

193/2004 Sources of efficiency gains in port reform: non parametric malmquist decomposition tfp in- dex for Mexico

Antonio Estache, Beatriz Tovar de la Fé y Lourdes Trujillo 194/2004 Persistencia de resultados en los fondos de inversión españoles

Alfredo Ciriaco Fernández y Rafael Santamaría Aquilué

195/2005 El modelo de revisión de creencias como aproximación psicológica a la formación del juicio del auditor sobre la gestión continuada

Andrés Guiral Contreras y Francisco Esteso Sánchez

196/2005 La nueva financiación sanitaria en España: descentralización y prospectiva David Cantarero Prieto

197/2005 A cointegration analysis of the Long-Run supply response of Spanish agriculture to the common agricultural policy

José A. Mendez, Ricardo Mora y Carlos San Juan

198/2005 ¿Refleja la estructura temporal de los tipos de interés del mercado español preferencia por la li- quidez?

Magdalena Massot Perelló y Juan M. Nave

199/2005 Análisis de impacto de los Fondos Estructurales Europeos recibidos por una economía regional:

Un enfoque a través de Matrices de Contabilidad Social M. Carmen Lima y M. Alejandro Cardenete

200/2005 Does the development of non-cash payments affect monetary policy transmission?

Santiago Carbó Valverde y Rafael López del Paso

201/2005 Firm and time varying technical and allocative efficiency: an application for port cargo han- dling firms

Ana Rodríguez-Álvarez, Beatriz Tovar de la Fe y Lourdes Trujillo 202/2005 Contractual complexity in strategic alliances

Jeffrey J. Reuer y Africa Ariño

203/2005 Factores determinantes de la evolución del empleo en las empresas adquiridas por opa Nuria Alcalde Fradejas y Inés Pérez-Soba Aguilar

204/2005 Nonlinear Forecasting in Economics: a comparison between Comprehension Approach versus Learning Approach. An Application to Spanish Time Series

Elena Olmedo, Juan M. Valderas, Ricardo Gimeno and Lorenzo Escot