The Metro 2040 policy reviews are all being undertaken as part of the regular work plan in the Council-approved Regional Planning Budget. Efficient administration is a key to the successful, efficient and consistent implementation of the regional growth strategy.

EXECUTIVE SUMMARY

For planning purposes, the overall materiality for the consolidated financial statements for the year ended 31 December 2020 is set at. Please see the attached engagement letter in Appendix C for specific details regarding the scope of our work.

YOUR DEDICATED BDO AUDIT TEAM

AUDIT TIMELINE

SIGNIFICANT AUDIT RISKS AND PLANNED RESPONSES

We will inquire with management about any significant changes to the remaining life and associated costs of the landfill. We will inquire with management about ongoing litigation, and potential claims impacting the Districts.

MATERIALITY

For our audit procedures regarding property, plant and equipment (“TCA”) and other assets and liabilities related to TCA, we identified a higher materiality based on the net book value of TCA. We will communicate to the Performance and Audit Committee all corrected and uncorrected misstatements identified during our audit, except for those misstatements that we determine are “obviously trivial.”

USING THE WORK OF OTHERS

Experts

APPENDICES

APPENDIX A: BDO AUDIT STRATEGY

APPENDIX B: DRAFT INDEPENDENT AUDITOR’S REPORT

Independent Auditor’s Report

However, future events or conditions may cause the consolidated entity to cease to function as a going concern. Obtain sufficient and appropriate audit evidence regarding the financial information of entities or business activities within the Group to express an opinion on the consolidated financial statements.

APPENDIX C: ENGAGEMENT LETTER

APPENDIX D: RESPONSIBILITIES

AUDITOR’S ENGAGEMENT OBJECTIVES

AUDITOR’S RESPONSIBILITIES FOR DETECTING FRAUD

RESPONSIBILITIES OF THOSE CHARGED WITH GOVERNANCE

MANAGEMENT RESPONSIBILITIES

Peformance and Audit

BDOManagement

APPENDIX E: BDO RESOURCES

APPENDIX F: CHANGES IN ACCOUNTING STANDARDS WITH POTENTIAL TO AFFECT YOUR ORGANIZATION

Subsequent measurement of the liability may result in either a change in the carrying amount of the related tangible capital asset (or a component thereof), or an expense, depending on the nature of the remeasurement and whether the asset remains in productive use. As a result of the issuance of Article PS 3280:. editorial changes have been made to other standards; and. This is one of the most significant new standards in years and will require significant staff time in most entities to prepare for compliance.

Because the Conceptual Framework is used to develop generally accepted accounting principles (GAAP), but is not itself considered GAAP, the introduction of the Conceptual Framework is not expected to have an immediate impact. When government nonprofits were included in the PSA Manual, they were given the option to adopt PSAS standards or PSAS standards in combination with the “4200 Series” of standards that reflect Part III of the CPA Manual. This is a difficult area due to the fact that many GNFPOs operate very differently from governments and therefore do not fit well into the government's financial reporting model.

The existing Employee Benefits standards in PS 3250, Retirement Benefits and PS 3255, Post-Employment Benefits are among the older standards that currently exist in the PSA handbook. To provide an update on the work of the Project Delivery Department in relation to the development and deployment of Best Practice for Project Delivery in the area of project costing. Cost estimating is the forecasting of the cost of the project, from inception to project completion.

ATTACHMENT

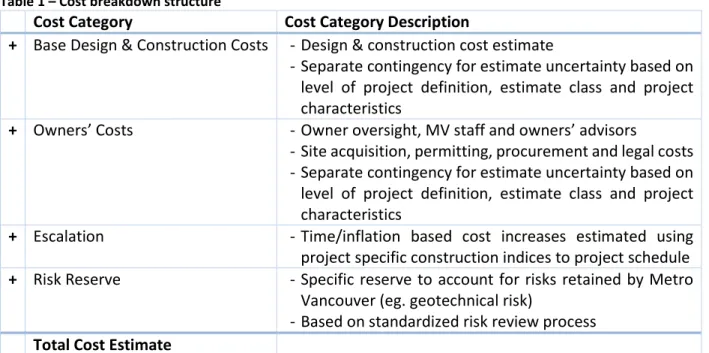

Standardized Cost Categorization

A separate contingency for estimate uncertainty based on project definition level, estimate class, and project characteristics. Site acquisition, permitting, procurement and legal costs - separate assessment uncertainty contingencies based on project definition level, assessment class and project characteristics. Escalation – Time/inflation based cost increases estimated using project specific construction indices in the project schedule + Risk Reserve – A special reserve to account for risks retained by Metro.

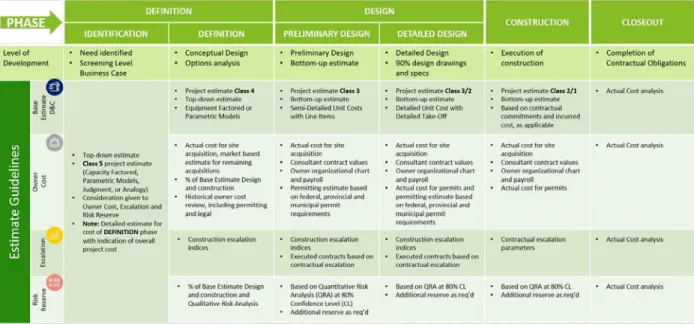

Project Implementation Best Practice Response - Project Assessment Framework Date of Finance and Intergovernmental Committee Regular Meeting: 18 November 2020 Page 3 of 4 The baseline design and construction cost estimate includes a separate uncertainty assessment line item to allow for design refinement and assumption assessment, when the scope is further defined throughout the life cycle. This allows the level of scope definition, the complexity of the project and the novelty of the scope of work or implementation model to be taken into account;.

The proprietary cost estimate also includes a separate line item for uncertainty estimation, which allows assumptions to be evaluated as the site and control model are further defined throughout the life cycle. A separate risk reserve covers risks owned by Metro Vancouver that are identified, managed and quantified in accordance with a standardized risk review process. Having a separate risk reserve encourages a thorough consideration of systemic and project-specific risks and can be used in evaluating the procurement and risk allocation model.

Consistent Guidelines Throughout the Project Lifecycle

Response to Project Delivery Best Practices – Project Estimating Framework Regular Meeting of the Financial and Intergovernmental Commission Date: November 18, 2020 Page 4 of 4. The guidelines described above have been developed using the Association for the Advancement of Cost Engineering International's estimating classification system ( AACEi). The classification system includes five estimation classes, from class 5, which corresponds to the lowest project definition, to class 1, which corresponds to the highest project definition.

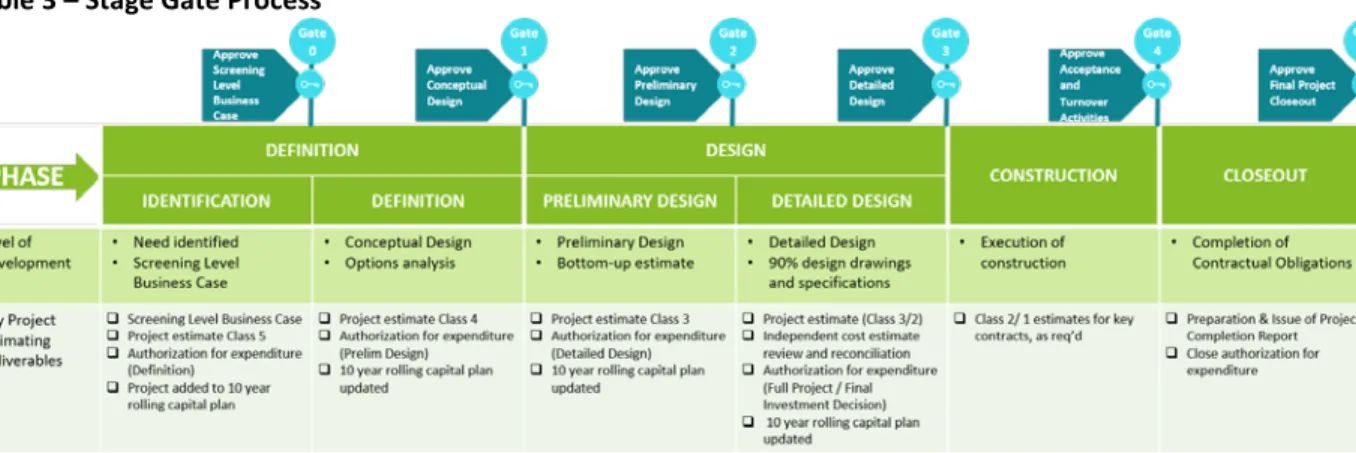

Formalized Cost and Scope Stage Gate Process

That the Performance and Audit Committee receives for its information the report dated January 4, 2021 entitled "Tender/Contract Award Information - September 2020 to November 2020". In addition, there were seven (7) existing contracts that required contract amendments, necessitating additional reporting to the Performance and Audit Committee. 500,000 will be reported to the Performance and Audit Committee to align with the thresholds outlined in the policy.

The following contracts were awarded during the months of September 2020 to November 2020 (details attached as ANNEX A):. Tender/Contract Award Information – September 2020 to November 2020 Regular Performance and Audit Committee Meeting: January 14, 2021 Page 2 of 5. WSP Canada Group Limited, Associated Engineering. Tender/contract award information – September 2020 to November 2020 Date of regular meeting of the Performance and Audit Committee: January 14, 2021 Page 3 of 5.

Information on Tender/Contract Award – September 2020 to November 2020 Performance and Audit Committee Ordinary Meeting Date: January 14, 2021 Page 4 of 5 Information on Tender/Contract Award – September 2020 to November 2020 Performance and Audit Committee Ordinary Meeting Date: January 14, 2021 Page 5 of 5. APPENDIX B: Contract modified to a value of more than $500,000 but not previously reported to the Performance and Audit Committee.

Appendix A

Bidders invited by Metro Vancouver and BC Bid websites and private invitation on April 20, 2020. Bidders invited by Metro Vancouver and BC Bid websites and private invitation on May 8, 2020. Bidders invited by Metro Vancouver and BC Bid websites and private invitation on 5/27 .2020.

Proposers were invited from the Metro Vancouver and BC Bid websites and private invitations on December 17, 2019. Proponents were invited from the Metro Vancouver and BC Bid websites and private invitations on August 28, 2020. Proponents were invited from the websites of Metro BC and Metro Vancouver private invite on May 28, 2020.

Supporters were invited by the Metro Vancouver and BC Bid websites and a private invitation on June 23, 2020. Supporters were invited by the Metro Vancouver and BC Bid websites and a private invitation on September 28, 2020. Supporters were invited by the websites of Metro Vancouver and BC Pray and private invitations. invitation on September 24, 2020.

Appendix B

Appendix C

Consulting Engineering Services for Iona Island Wastewater Treatment Plant Project Definition for the Greater Vancouver Sewerage and Drainage District. 01 is the result of a technical investigation of aerobic granular sludge (AGS) technology, additional modeling to characterize the site and assist with the geotechnical design, condition assessments of the existing facility to determine suitability and cost of asset reuse, development of additional design concepts to integrate existing and new facilities, and an analysis of solids treatment options and operational impacts. Consulting Engineering Services - Detailed design and construction for the Fleetwood Reservoir for the Greater Vancouver Water District.

This contract is funded within the Greater Vancouver Water District capital program capital budget. The latest change order totaling $207,743 is the result of putting the project on hold for over two (2) years at the request of the City. As part of the approval process, the city required subdivision of the landfill to create three separate properties: the transfer station site, the EagleQuest golf course and "Lot 3," which is slated for future development.

As a result, the three properties had to be made independent by the separation of utilities and the United Boulevard frontage improvements completed. The final design of the portable building structure ("pre-engineered metal building") is completed by the supplier in cooperation with the structural designer who is responsible for the design of the concrete foundations. Also, additional services to support engineering in climate change adaptation and mitigation, support community engagement for public and stakeholder workshops, explore value-added partnership opportunities for environmental and community improvement, lead feasibility analysis of community improvement opportunities and sustainability performance, and develop additional architectural and landscape concepts to facilitate the integration of existing and new plant design.

Appendix D

Supply, manufacture, testing and commissioning of a pilot plant for digestion optimization at Lulu Island's wastewater treatment plant. Annacis Island Wastewater Treatment Plant gates and hydraulic system for the inlet control chamber channel. Pre-Selection of Liquid Train Odor Control Equipment for Northwest Langley Wastewater Treatment Plant Upgrade.

Theme: Átl'ka7tsem/Howe Sound Biosphere Nomination approved by the Canadian Commission for UNESCO. The Howe Sound Biosphere Region Initiative Society is pleased to confirm the submission of Átl'ka7tsem/Howe Sound to become Canada's 19th UNESCO Biosphere Region. On behalf of the Canadian Commission for UNESCO, I am pleased to confirm the submission of the nomination file for the proposal.

The nomination package has now been sent to UNESCO in Paris for review by the International Advisory Board. Click here for the latest news on Howe Sound Biosphere Region Initiative programs and initiatives. The Howe Sound Biosphere Region Initiative is the result of a partnership with the Squamish Nation and works locally with the goal of a global example of finding balance between.